Conceptually transparent interpretation of probablity.

Uncertainty quantification.

Allows to explicitly include prior knowledge in the model.

Felxible and suited for many applications in academia and industry.

Scalable*

Why PyMC?

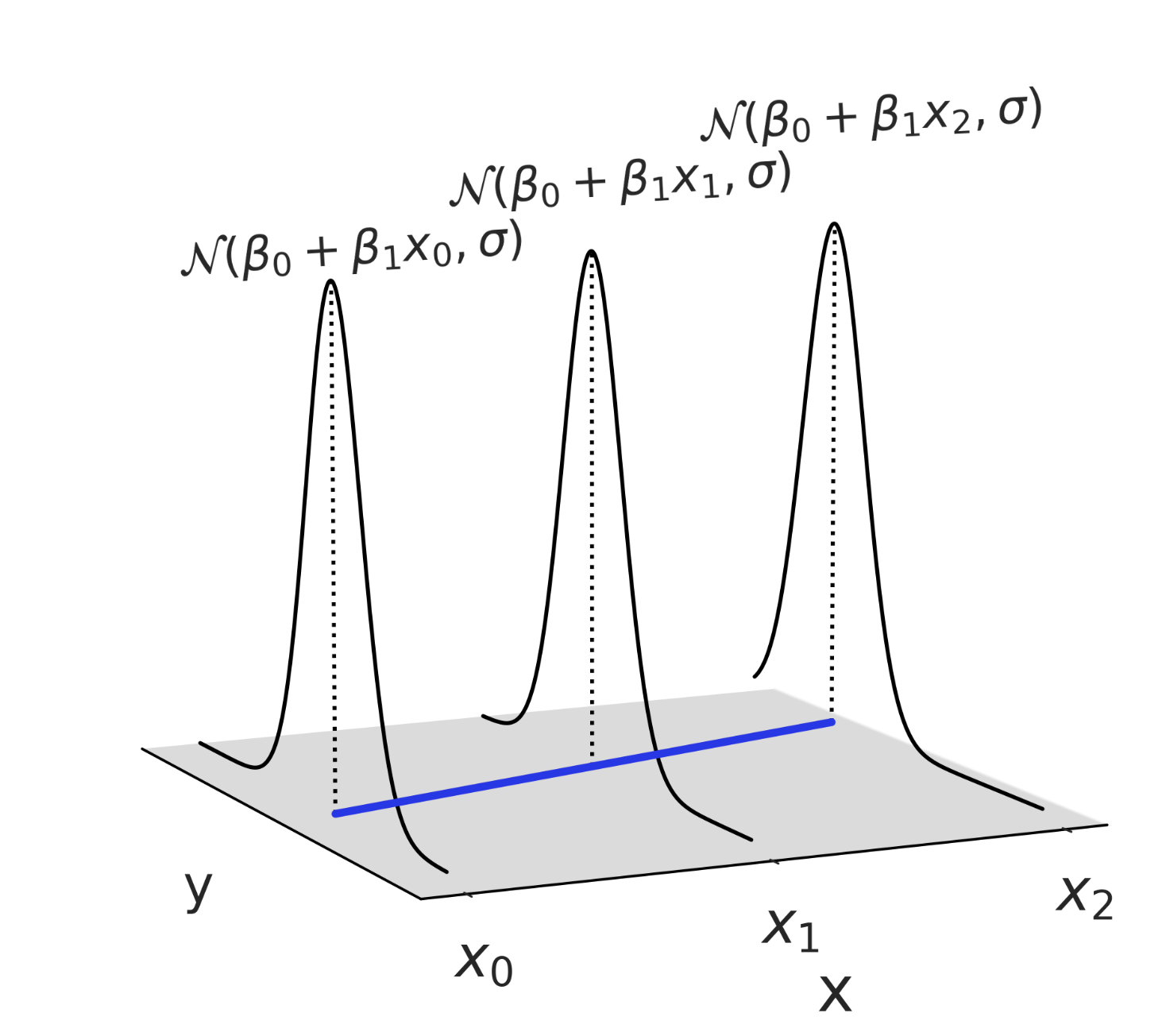

Bayesian Inference : An Example

Suppose you see a person with long hair. You want to estimate the probablity that this person is a woman. That is, for \(A = \text{woman}\) and \(B = \text{long hair}\), we want to estimate \(P(A|B)\)

Prior-Information

You belive \(P(A) = 0.5\), \(P(B)=0.4\) and \(P(B|A) = 0.7\).

Two ML Models: Linear Regression (\(L^1\)) with second order interactions and XGBoost

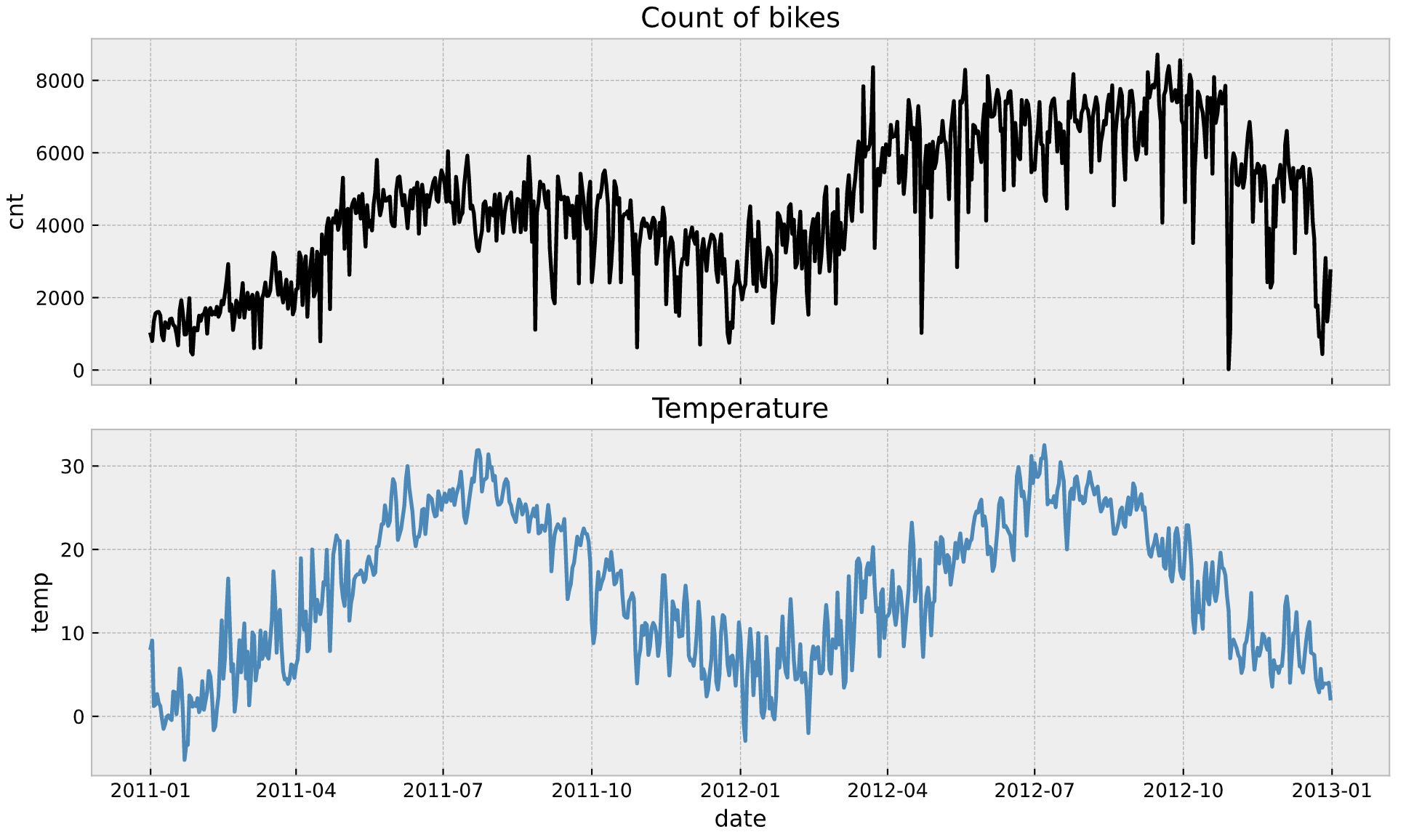

Example: Bike Rental Model

Two ML Models: Both see a negative effect of temperature in bke rentals ini the month of July.

Example: Bike Rental Model

Time-Varying Coefficients

\[

b(t) \sim N(b(t - 1), \sigma^2)

\]

Example: Bike Rental Model

Time-Varying Coefficients

Example: Bike Rental Model

Time-Varying Coefficients

Example: Bike Rental Model

Time-Varying Coefficients

Effect of temperature on bike rentals as a function of tmie for a time varying coeffiicient model (via Gaussian random walk).

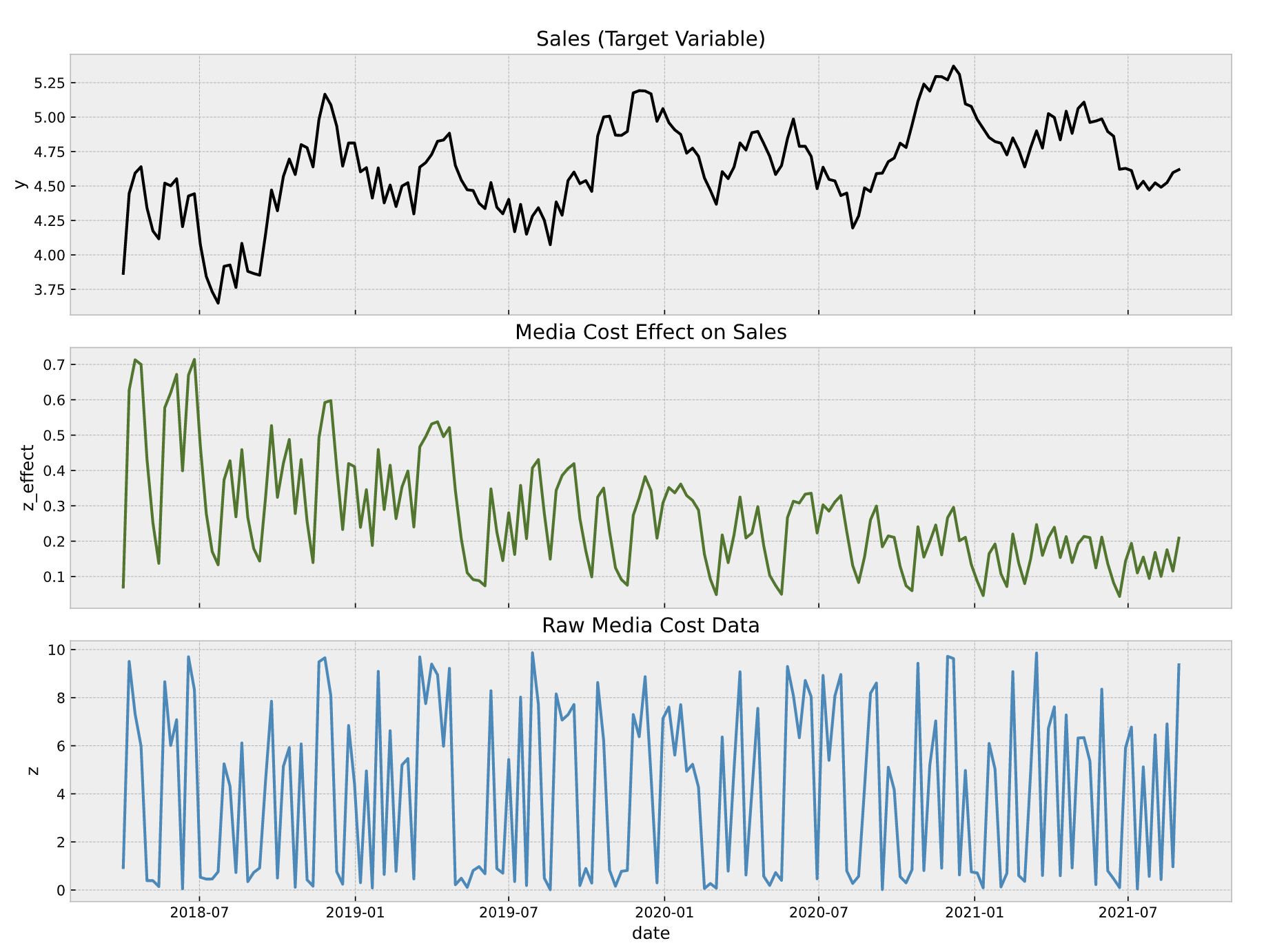

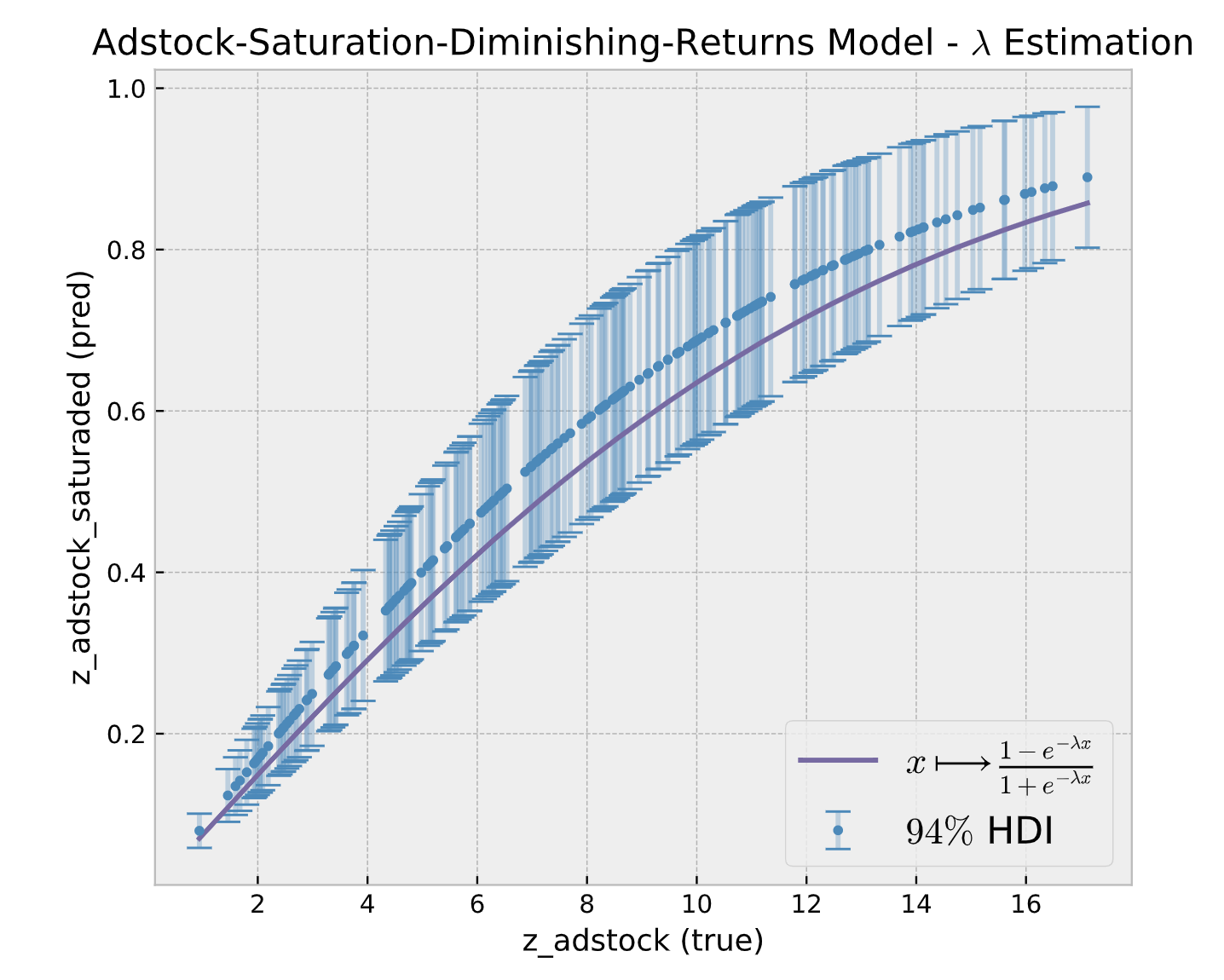

Application: Media Mix Model (MMM)

Application: Media Mix Model (MMM)

MMM structure: Media data (cost, impressions or clicks) is modeled using carryover effects (adstock) and saturation effects. In addition, one can control for seasonality and external regressors. In this example, we allow time-varying coefficients to capture the effect development over time.

Application: Media Mix Model (MMM)

Fitted saturation effect. This can be used for media mix budget optimization.