%%{init: {"theme": "white", "themeVariables": {"fontSize": "54px"}, "flowchart":{"htmlLabels": false}}}%%

flowchart TD

kernel["kernel"] --> spectral_sensity["Spectral Density"]

spectral_sensity --> polynomial["Polynomial Expansion"]

laplacian["Laplacian"] --> fourier["Fourier Transform"]

laplacian --> dirichlet["Dirichlet's BC"]

dirichlet --> spectral_decomposition["Spectral Decomposition"]

spectral_decomposition["Spectral Decomposition"] --> functional["Functional Calculus"]

polynomial --> identify_coefficients["Identify Coefficients"]

fourier --> identify_coefficients

functional --> identify_coefficients

identify_coefficients --> approximation["Approximation Formula"]

Introduction to Hilbert Spaces Approximations Gaussian Processes

A conceptual and practical viewpoint

Mathematician & Data Scientist

Outline

Reference Notebook 📓

Motivation: Some Applications

Gaussian Processes

Hilbert Space Approximation Deep Dive

Example: Birthdays Dataset

References

Motivation: Some Applications

Some Applications

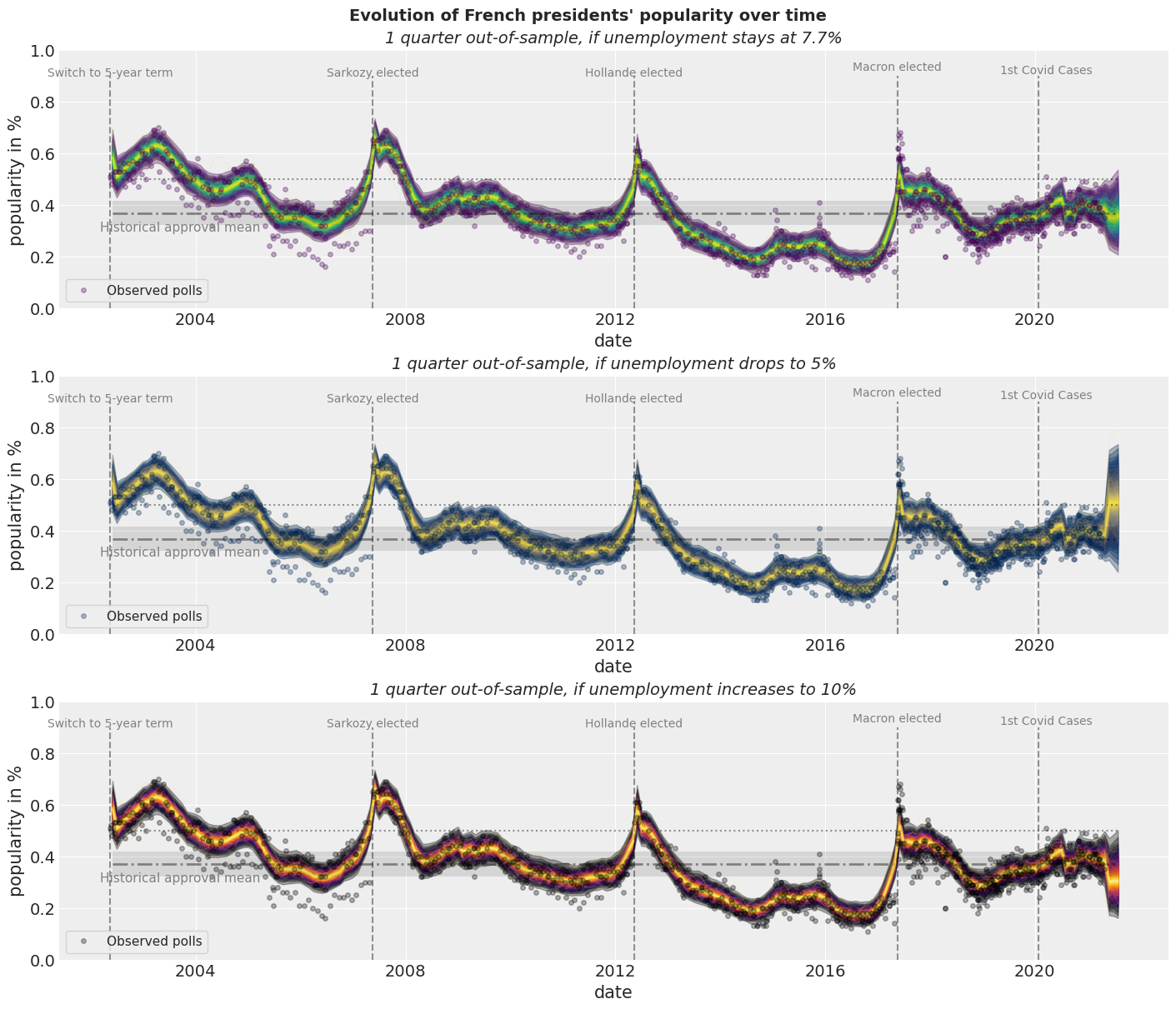

Case Study: How popular is the President?

Some Applications

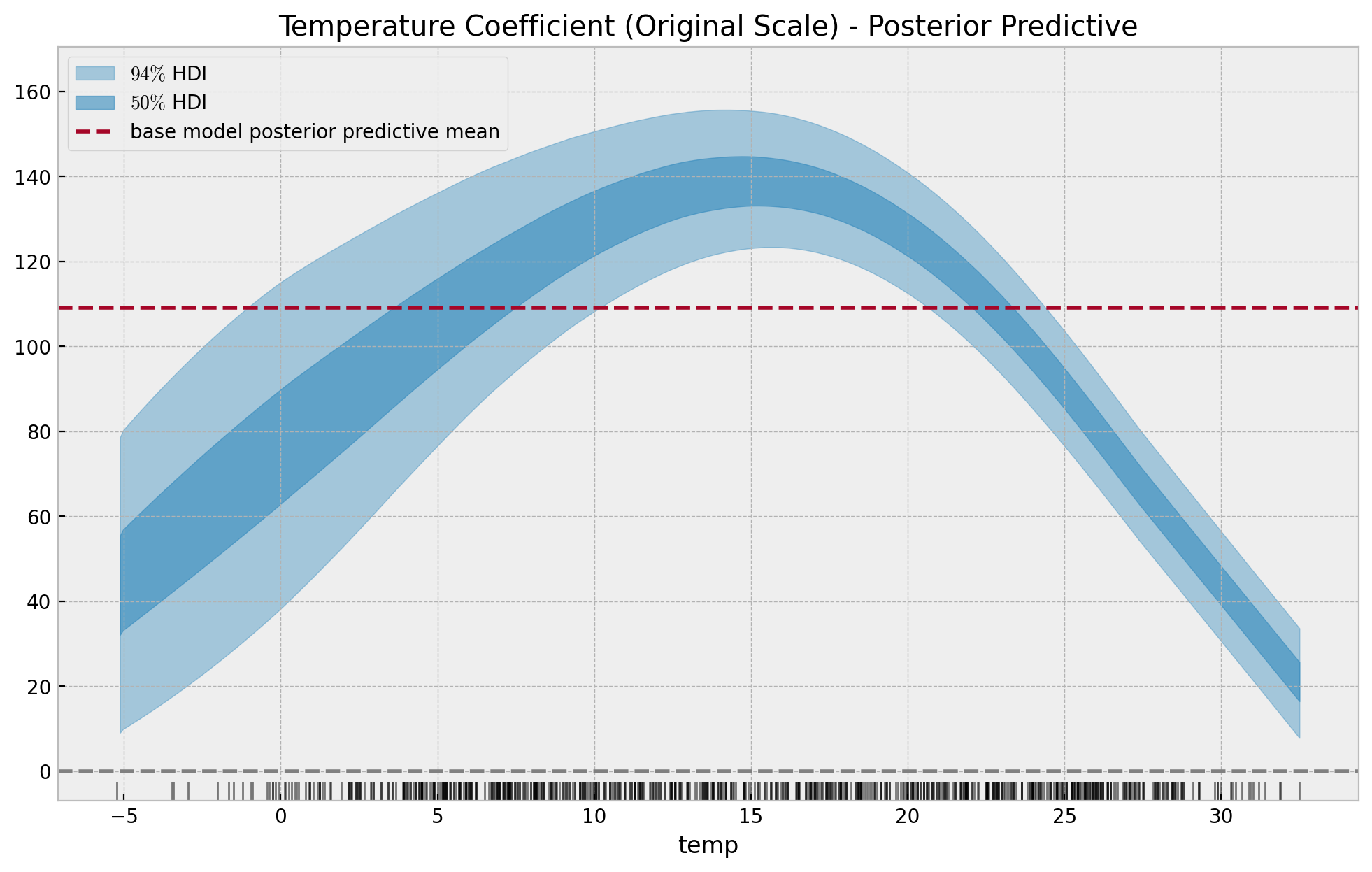

Time-Varying Regression Coefficients

Some Applications

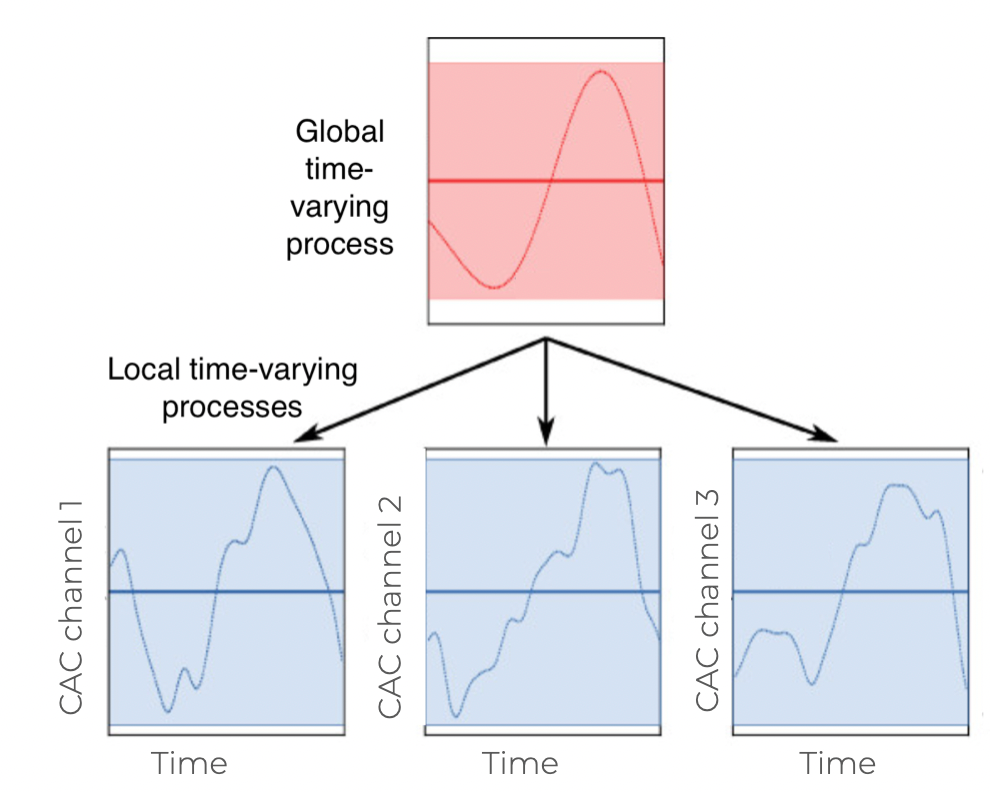

Changes in marketing effectiveness over time

Gaussian Processes

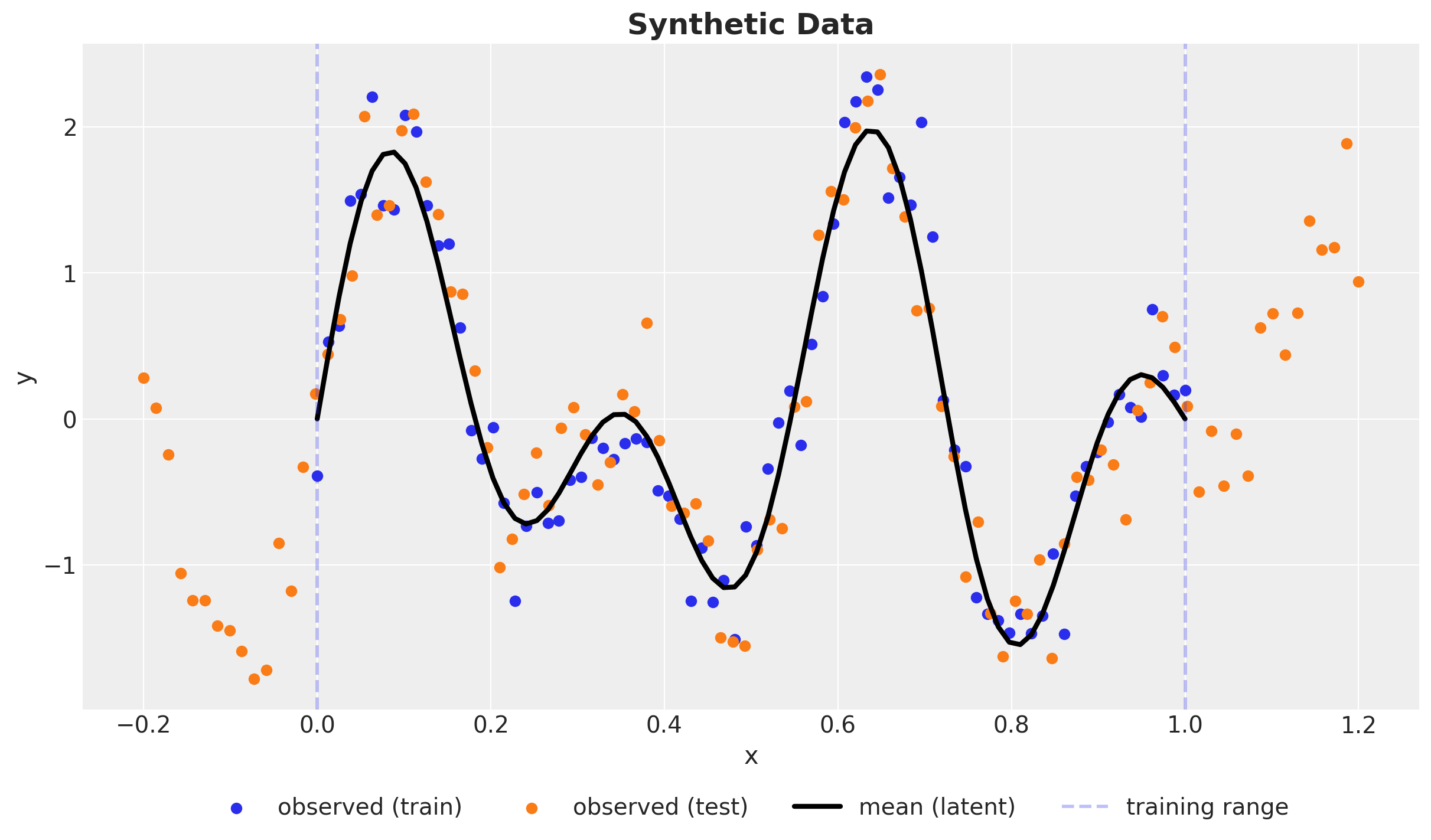

Synthetic Data

\(y \sim \text{Normal}(\sin(4 \pi x) + \sin(7 \pi x), 0.3^2)\)

Kernel

A way to encode similarity between points

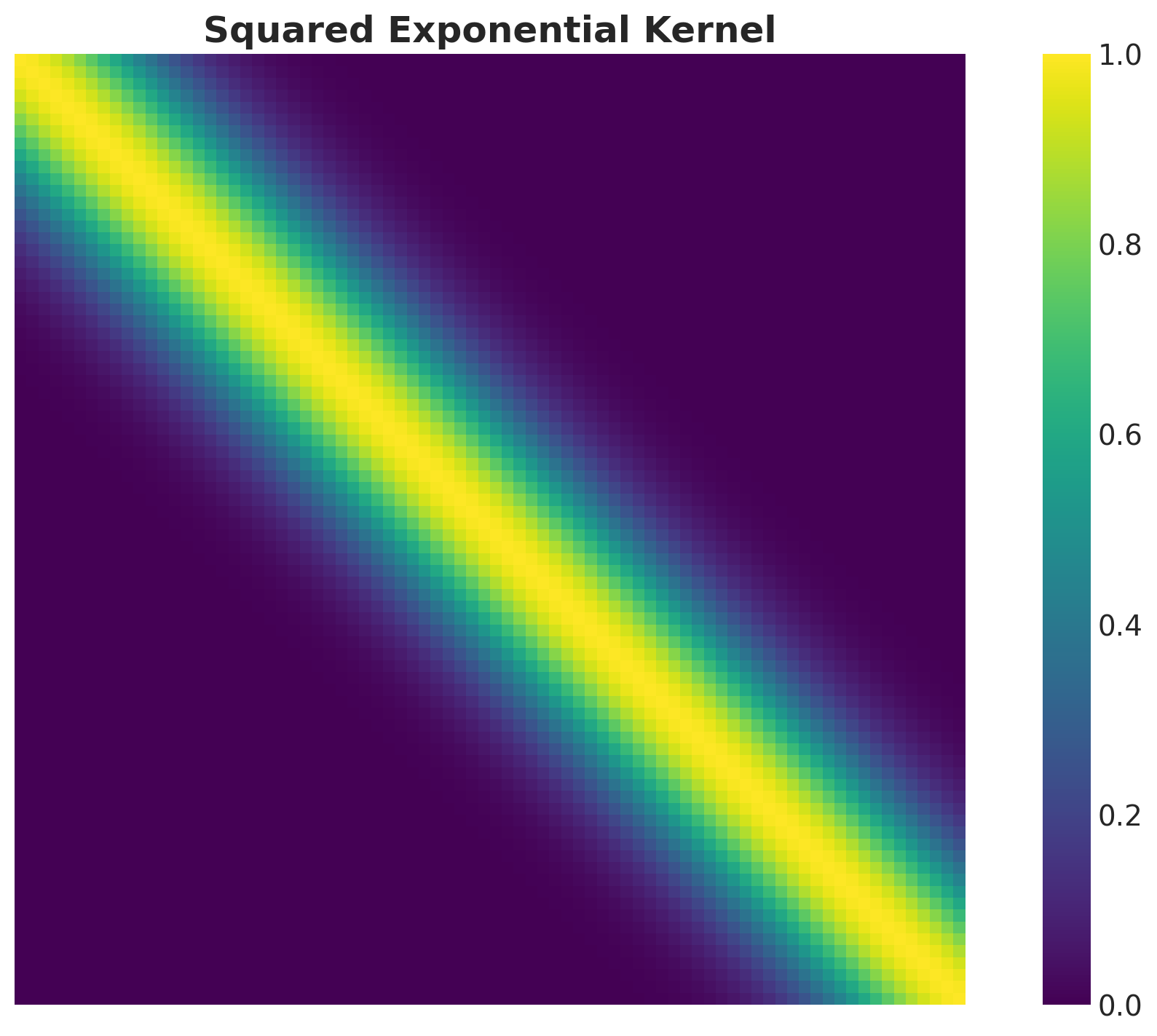

Example: Squared Exponential Kernel

\[ k(x, x') = a^ 2 \exp\left(-\frac{(x - x')^2}{2 \ell^2}\right) \]

Where \(a\) is the amplitude and \(\ell\) is the length-scale.

Note

Observe that the kernel just depends on the distance between points \(r = x - x'\). This is a property of stationary kernels.

Kernel Matrix

GP Model - Prior

Let us denote by \((x, y)\) and the training data and by \(x_{*}\) the test set for which we want to generate predictions. We define by \(f\) and \(f_*\) the latent functions for the training and test sets respectively.

\[ \left( \begin{array}{c} y \\ f_* \end{array} \right) \sim \text{MultivariateNormal}(0, \boldsymbol{K}) \]

where

\[ \boldsymbol{K} = \left( \begin{array}{cc} K(X, X) + \sigma^2_n I & K(X, X_*) \\ K(X_*, X) & K(X_*, X_*) \end{array} \right) \]

GP Model - Conditioning

\[ f_*|X, y, X_* \sim \text{MultivariateNormal}(\bar{f}_*, \text{cov}(f_*)) \]

where

\[ \begin{align*} \bar{f}_* &= K(X_*, X){\color{red}{(K(X, X) + \sigma^2_n I)^{-1}}} \\ \text{cov}(f_*) & = K(X_*, X_*) - K(X_*, X){\color{red}{(K(X, X) + \sigma^2_n I)^{-1}}} K(X, X_*) \end{align*} \]

Important

Taking the inverse of the kernel matrix is the most computationally expensive part of the GP model. It is of order \(\mathcal{O}(n^3)\).

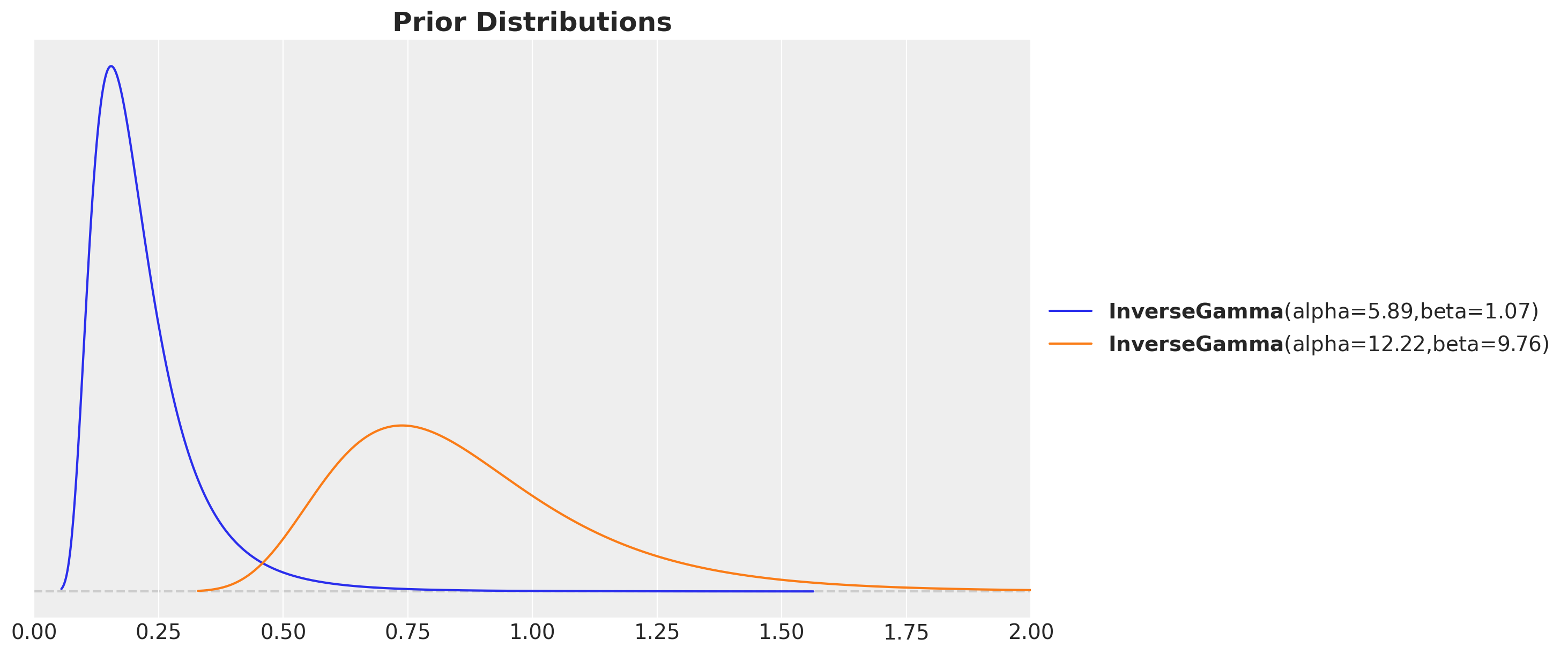

Kernel parameter priors

inverse_gamma_params_1 = pm.find_constrained_prior(

distribution=pm.InverseGamma,

lower=0.01,

upper=0.4,

init_guess={"alpha": 5, "beta": 3},

mass=0.94,

)

inverse_gamma_params_2 = pm.find_constrained_prior(

distribution=pm.InverseGamma,

lower=0.5,

upper=1.5,

init_guess={"alpha": 5, "beta": 6},

mass=0.94,

)

fig, ax = plt.subplots()

pz.InverseGamma(**inverse_gamma_params_1).plot_pdf(color="C0", ax=ax)

pz.InverseGamma(**inverse_gamma_params_2).plot_pdf(color="C1", ax=ax)

ax.set(xlim=(0, 2))

ax.set_title("Prior Distributions", fontsize=18, fontweight="bold");Kernel parameter priors

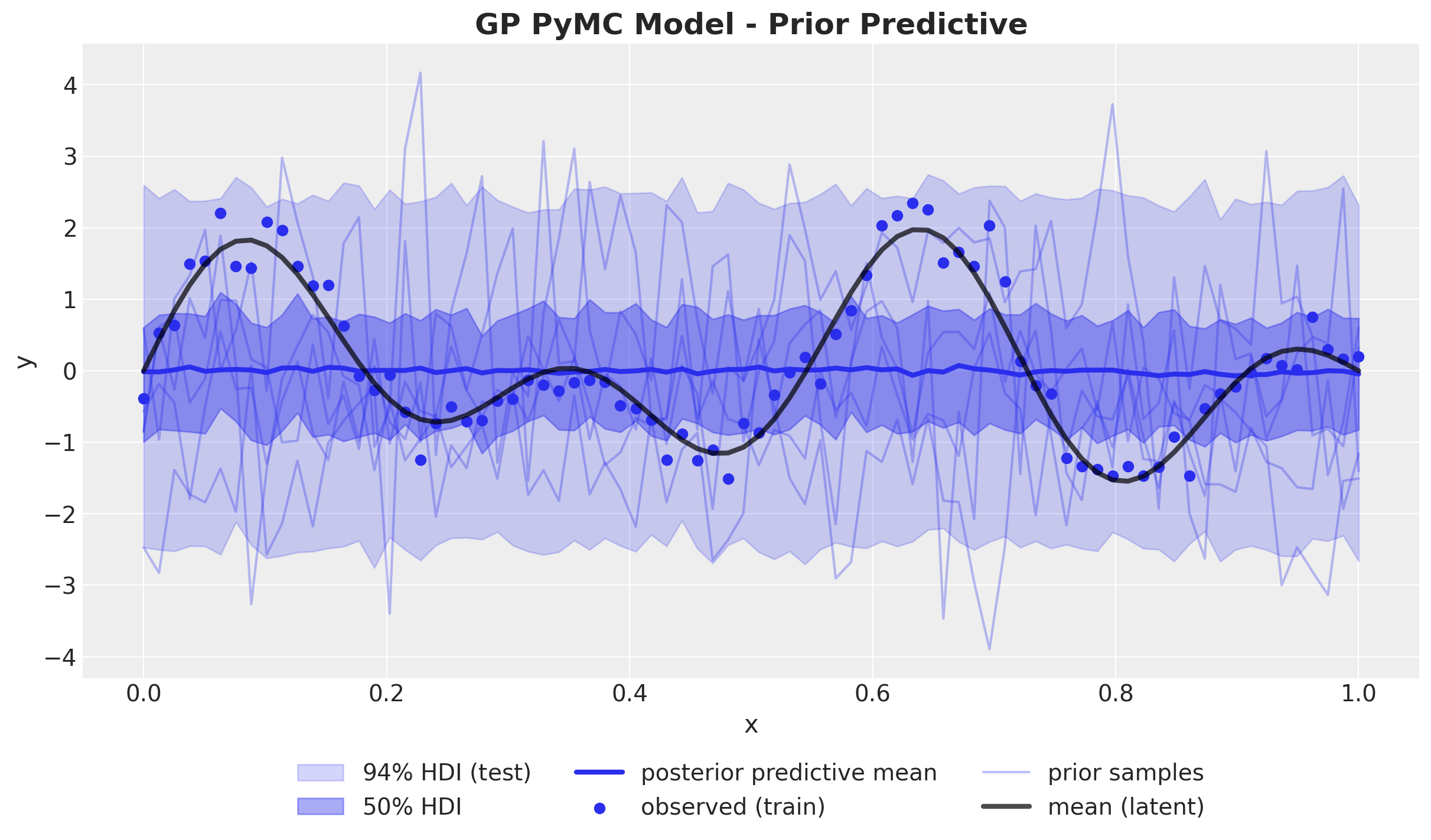

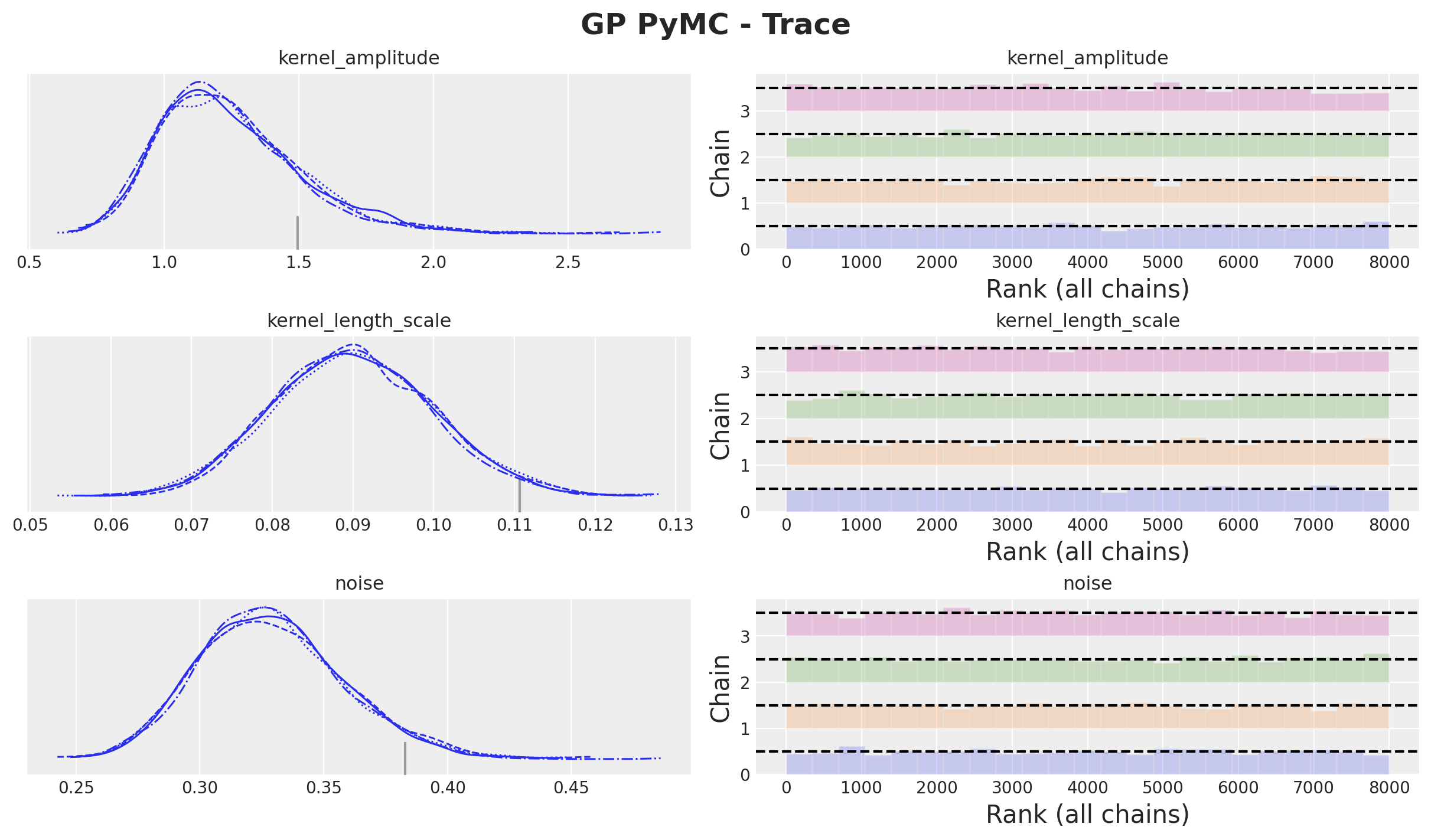

GP Model in PyMC

with pm.Model() as gp_pymc_model:

x_data = pm.MutableData("x_data", value=x_train)

kernel_amplitude = pm.InverseGamma("kernel_amplitude", ...)

kernel_length_scale = pm.InverseGamma("kernel_length_scale", ...)

noise = pm.InverseGamma("noise", ...)

mean = pm.gp.mean.Zero()

cov = kernel_amplitude**2 * pm.gp.cov.ExpQuad(

input_dim=1, ls=kernel_length_scale

)

gp = pm.gp.Latent(mean_func=mean, cov_func=cov)

f = gp.prior("f", X=x_data[:, None])

pm.Normal("likelihood", mu=f, sigma=noise, observed=y_train_obs)GP Model in PyMC

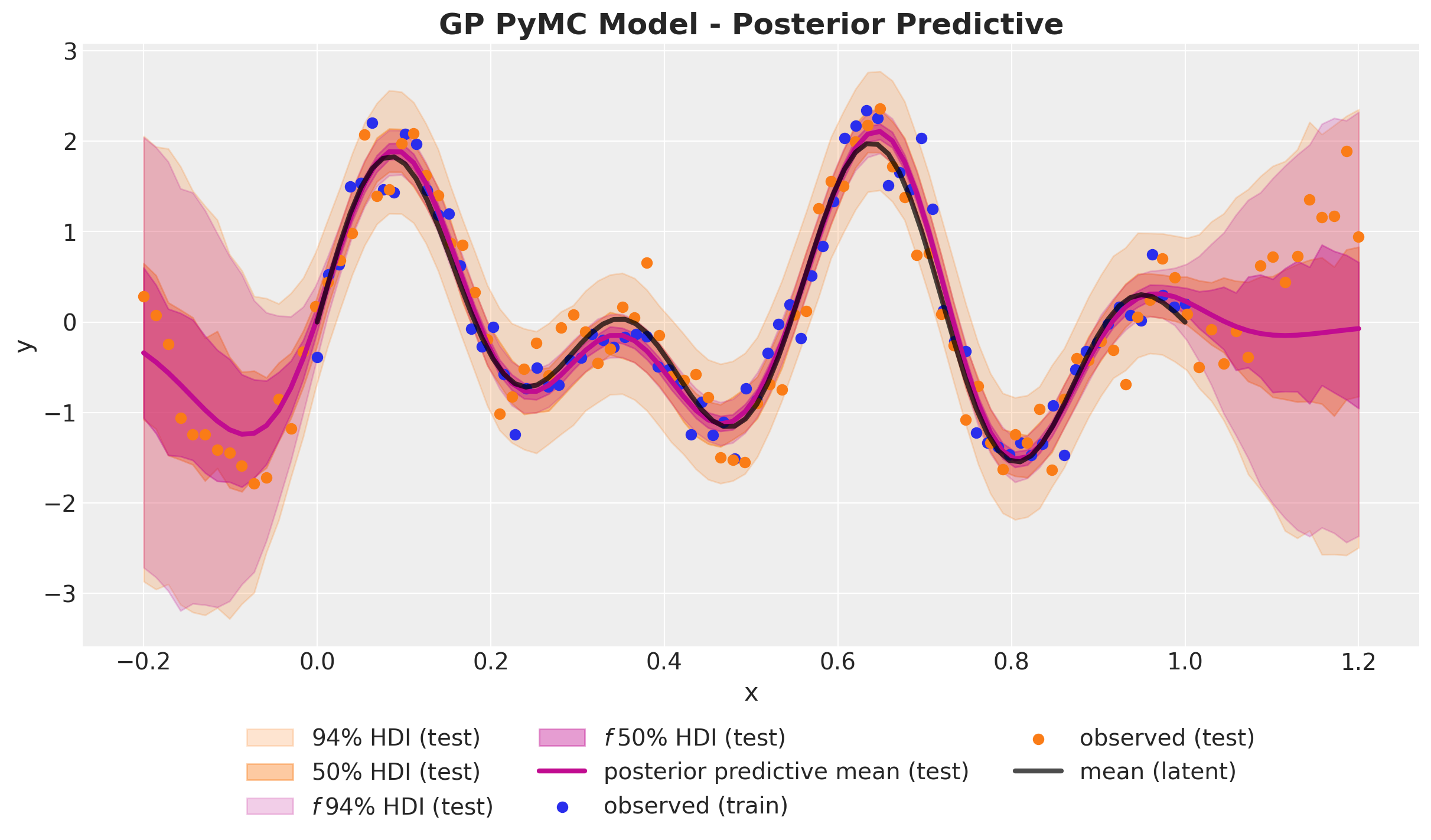

GP Model - Prior Predictions

GP Model - Posterior Distributions

Out-of-Sample Predictions

conditional method

with gp_pymc_model:

x_star_data = pm.MutableData("x_star_data", x_test)

f_star = gp.conditional("f_star", x_star_data[:, None])

pm.Normal("likelihood_test", mu=f_star, sigma=noise)

gp_pymc_idata.extend(

pm.sample_posterior_predictive(

trace=gp_pymc_idata,

var_names=["f_star", "likelihood_test"],

random_seed=rng_subkey[1].item(),

)

)GP Model - Posterior Predictive

Hilbert Space Gaussian Process (HSGP) Approximation

HSGP Deep Dive

Approach Summary 🤓

Strategy: Approximate the Gram matrix \(K\) with a matrix \(\tilde{K}\) with a smaller rank \(m < n\).

Key Idea: Interpret the covariance function as the kernel of a pseudo-differential operator and approximate it using Hilbert space methods.

Result: A reduced-rank approximation for the covariance function, where the basis functions are independent of the covariance functions and their parameters (plus asymptotic convergence).

Hilbert Space Approximation

Hilbert Space Approximation

Approximation Strategy Steps

- D-Tour: Eigenvalues and Eigenvectors

- We recall the spectral density \(S(\omega)\) associated with a stationary kernel function \(k\).

- We approximate the spectral density \(S(\omega)\) as a polynomial series in \(||\omega||^2\).

- We can interpret these polynomial terms as powers of the Laplacian operator. The key observation is that the Fourier transform of the Laplacian operator is \(||\omega||^2\).

- Next, we impose Dirichlet boundary conditions on the Laplacian operator which makes it self-adjoint and with a discrete spectrum.

- We identify the expansion in (2) with the sum of powers of the Laplacian operator in the eigenbasis of (4).

- We arrive at the final approximation formula and explicitly compute the terms for the squared exponential kernel in the one-dimensional case.

Eigenvalues and Eigenvectors

Recall that given a matrix \(A\) (or a linear operator) the eigenvalues and eigenvectors are the solutions to the equation

\[A v = \lambda v\]

where \(v \neq \vec{0}\) is the eigenvector and \(\lambda\) is the eigenvalue.

The spectrum of a matrix is the set of its eigenvalues.

Example - \(2 \times 2\) Matrix

\[ A = \begin{pmatrix} 1 & 2 \\ 2 & 1 \end{pmatrix} \]

The eigenvalues are \(\lambda_1 = 3\) and \(\lambda_2 = -1\) with eigenvectors:

\[ v_1 = \frac{1}{\sqrt{2}} \begin{pmatrix} 1 \\ 1 \end{pmatrix} \quad \text{and} \quad v_2 = \frac{1}{\sqrt{2}} \begin{pmatrix} -1 \\ 1 \end{pmatrix} \]

Properties

\[ v_1^{T} v_2 = 0 \quad \text{and} \quad v_1^{T} v_1 = v_2^{T} v_2 = 1 \]

The Spectral Theorem

The spectral theorem states that we can always find such orthonormal basis of eigenvectors for a symmetric matrix.

Observe that if we consider the change-of-basis matrix

\[ Q = \begin{pmatrix} v_1 & v_2 \end{pmatrix} \]

then we can write the matrix \(A\) in the new basis as

\[ D = Q^{T} A Q = \begin{pmatrix} 3 & 0 \\ 0 & -1 \end{pmatrix} \]

Code Example

import jax.numpy as jnp

A = jnp.array([[1.0, 2.0], [2.0, 1.0]])

# Compute eigenvalues and eigenvectors

eigenvalues, eigenvectors = jnp.linalg.eig(A)

print(f"Eigenvalues: {eigenvalues}\nEigenvectors:\n{eigenvectors}")

>> Eigenvalues: [ 3.+0.j -1.+0.j]

>> Eigenvectors:

>> [[ 0.70710678+0.j -0.70710678+0.j]

>> [ 0.70710678+0.j 0.70710678+0.j]]

# Change of basis matrix

Q = eigenvectors

Q.T @ A @ Q

>> Array([[ 3.00000000e+00+0.j, 4.44089210e-16+0.j],

[ 6.10622664e-16+0.j, -1.00000000e+00+0.j]], dtype=complex128)Spectral Projections

Another important consequence of the spectral theorem is that we can decompose the matrix \(A\) as a sum of projections onto its eigenspaces. That is, we can write re-write \(A\) as

\[ A = \sum_{j=1}^{2} \lambda_i v_j v_j^{T} \]

Projections

Observe that the operator \(P_{j} = v_j v_j ^{T}\) is indeed a projection operator, that is \(P^2 = P\) and \(P^T = P\), since the \(v_j\) constitutes an orthonormal basis.

Code Example

def proj(v, x):

return jnp.dot(v, x) * v

def matrix_proj(x):

return eigenvalues[0] * proj(Q[:, 0], x) + eigenvalues[1] * proj(Q[:, 1], x)

# First eigenvector

matrix_proj(Q[:, 0]) / eigenvalues[0]

>> Array([0.70710678+0.j, 0.70710678+0.j], dtype=complex128)

# Second eigenvector

matrix_proj(Q[:, 1]) / eigenvalues[1]

>> Array([-0.70710678-0.j, 0.70710678-0.j], dtype=complex128)

# Arbitrary vector

v = jnp.array([1.0, 2.0])

jnp.allclose(jnp.dot(A, v), matrix_proj(v))

>> Array(True, dtype=bool)Functional Calculus

The functional calculus is a generalization of the Taylor series for functions to operators. Given a function \(f\) we can define the operator \(f(A)\) as

\[ f(A) = \sum_{j=1}^{2} \color{red}{f(\lambda_j)} \color{blue}{v_j v_j^{T}} \]

Examples

- \(f(z) = z\) we recover the operator \(A\).

- \(f(z) = 1\) we get the identity operator \(I\).

- \(f(z) = z^2\) we get the operator \(A^2\).

- \(f(z) =e^{z}\) we get the operator \(\exp(A)\).

Example: Exponential of a Matrix

Consider the exponential of the matrix \(A\) defined as

\[ \exp(A) = \sum_{j=0}^{\infty} \frac{A^j}{j!} \]

Example: Exponential of a Matrix

On the other hand, we can use the fact that \(A = Q D Q^{T}\) and that \(Q\) is an orthogonal matrix to write

\[ \exp(A) = \sum_{j=0}^{\infty} \frac{(Q D Q^{T})^j}{j!} = Q \left(\sum_{j=0}^{\infty} \frac{D^j}{j!}\right) Q^{T} = Q \exp(D) Q^{T} \]

and observe that \(\exp(D)\) is a diagonal matrix with the exponential of the diagonal elements:

Spectral Densities

In the case a kernel function is stationary, we can use the spectral representation of the kernel function (Bochner’s theorem):

\[ k(r) = \frac{1}{(2 \pi)^{d}}\int_{\mathbb{R}^{d}} e^{i \omega^{T} r} d\mu(\omega) \]

where \(\mu\) is a positive measure. If this measure has a density, it is called the spectral density \(S(\omega)\) corresponding to the covariance function, i.e. \(d\mu(\omega) = S(\omega) d\omega\).

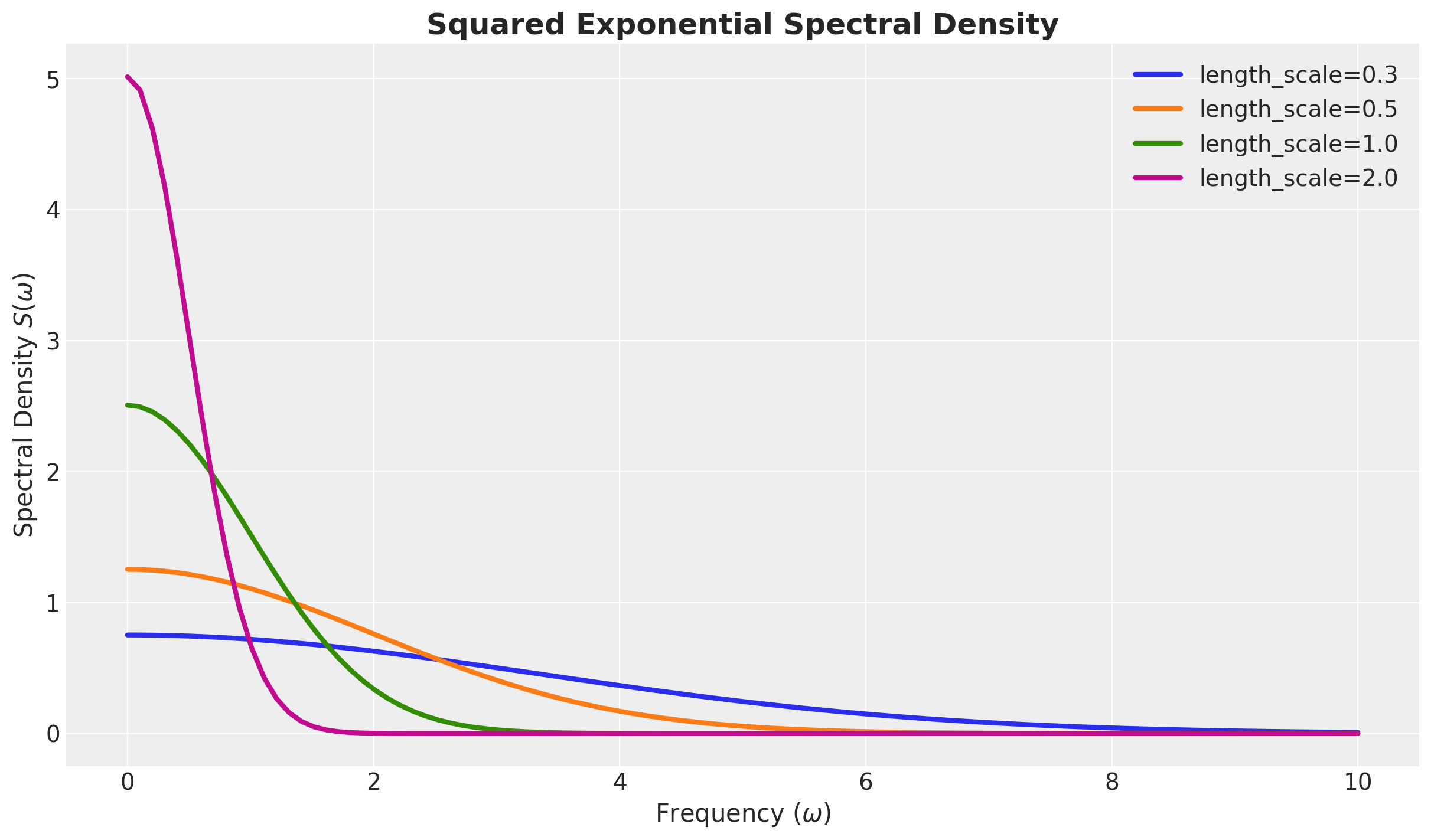

Spectral Density - Example

For the squared exponential kernel, it can be shown that

\[ S(\omega) = a^2(2 \pi \ell^2)^{d/2} \exp\left(-2\pi^2\ell^2\omega^2\right) \]

For the special case \(d=1\) we have

\[ S(\omega) = a^2 \sqrt{2 \pi} \ell \exp\left(-2\pi^2\ell^2\omega^2\right) \]

Tip

Note the similarity between the spectral density and the Fourier transform. For Gaussian-like kernels, like the squared exponential, we expect the associated spectral density to also be Gaussian-like.

\(S(\omega)\) Squared Exponential

Formal Power Expansion of the Spectral Density

Let us assume the kernel function is isotropic, i.e. it just depends on the Euclidean norm \(||r||\).

\(S(\omega)\) is also isotropic.

Write \(S(||\omega||) = \psi(||\omega||^2)\) for a suitable function \(\psi\).

We can expand \(\psi\) (Taylor-like expansion)

\[ \begin{align*} \psi(||\omega||^2) = a_0 + a_1 (||\omega||^2) + a_2 (||\omega||^2)^2 + a_3 (||\omega||^2)^3 + \cdots \end{align*} \]

The Laplace Operator

Recall the Laplace operator is defined as

\[ - \nabla^2 f = \sum_{i=1}^{d} \frac{\partial^2 f}{\partial x_i^2} \]

Tip

The Laplacian has many good properties:

Positive semi-definite

Elliptic

Self-adjoint (appropriate boundary conditions)

Kernel as a function of \(\nabla^2\)

One can verify that the Fourier transform of the Laplacian is

\[ \mathcal{F}[\nabla^2 f](\omega) = - ||\omega||^2 \mathcal{F}[f] \]

We can write the integral operator associated with the kernel

\[ \mathcal{K} := \int_{\mathbb{R}^d} k(\cdot, x')\phi(x') dx' \]

as

\[ \mathcal{K} = a_0 + a_1 (- \nabla^2) + a_2 (-\nabla^2)^2 - a_3 (-\nabla^2)^3 + \cdots \]

Dirichlet’s Laplacian

Boundary Conditions?

The most common boundary conditions are the Dirichlet boundary conditions, which are defined by requiring that the function vanishes on the boundary of the domain.

\[ \begin{align*} -\nabla^2 f &= \lambda f \quad \text{in} \quad \Omega \\ f &= 0 \quad \text{on} \quad \partial \Omega \end{align*} \]

Dirichlet’s Laplacian - Spectrum

It is is a self-adjoint operator defined on the Hilbert space \(L^{2}(\Omega)\) equipped with the Lebesgue measure. That is,

\[ \int_{\Omega} (-\nabla^2 f(x)) g(x) dx = \int_{\Omega} f(x) (-\nabla^2 g(x)) dx \]

It has discrete spectrum with eigenvalues \(\lambda_j \rightarrow \infty\) and eigenfunctions \(\phi_j\) that form an orthonormal basis of \(L^2(\Omega)\), so that \[ \int_{\Omega} \phi_{j}(x) \phi_{k}(x) dx = \delta_{jk} \]

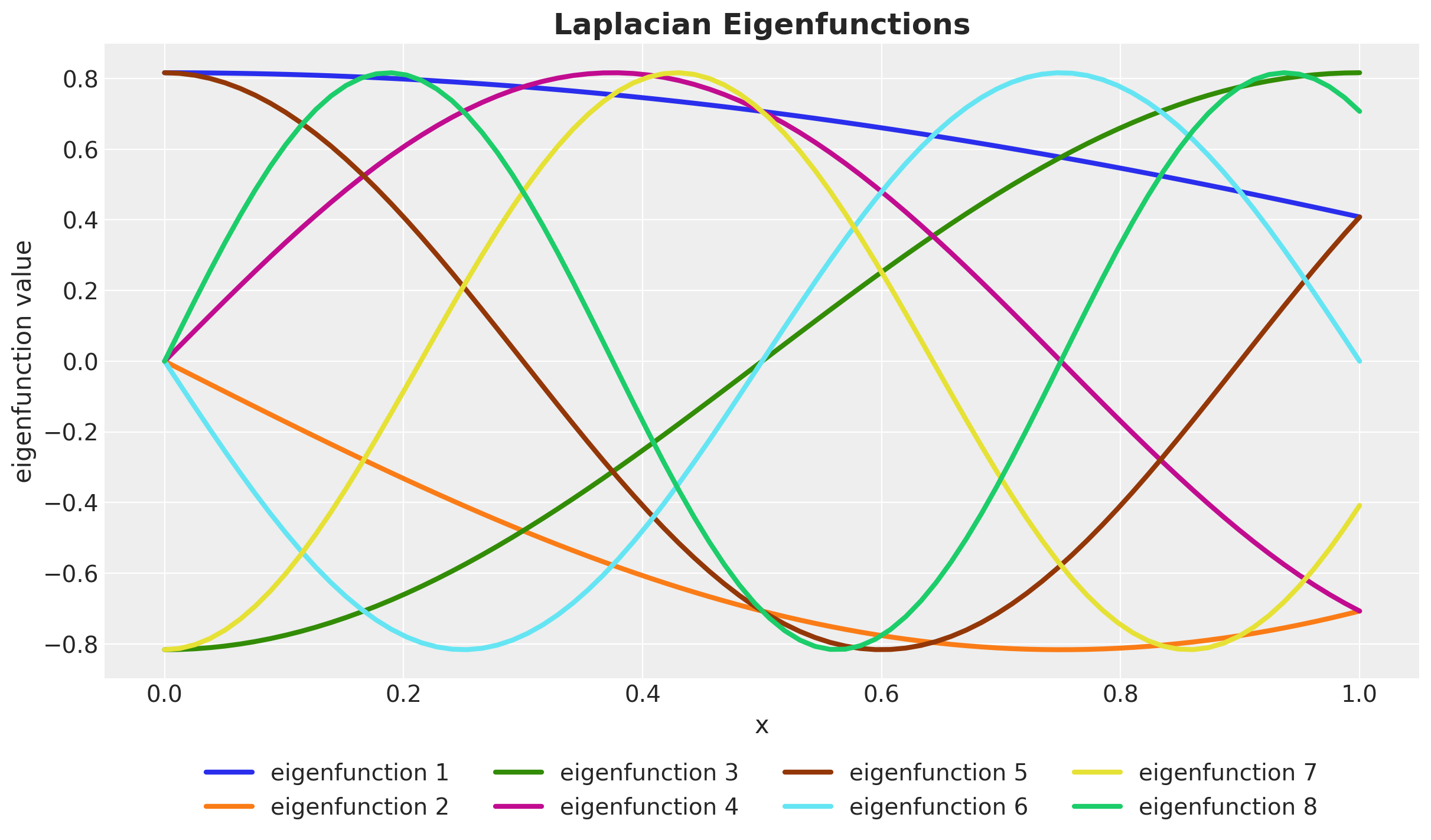

Example - One Dimensional Box

\(\Omega = [-L, L] \subset \mathbb{R}\)

\[ \frac{d^2 \phi}{dx^2} = - \lambda \phi \quad \text{with} \quad \phi(-L) = \phi(L) = 0 \]

Spectrum?

\[ \phi_j(x) = \sqrt{\frac{1}{L}} \sin\left(\frac{\pi j (x + L)}{2L}\right) \quad \text{and} \quad \lambda_j = \left(\frac{j \pi}{2L}\right)^2 \]

for \(j = 1, 2, \ldots\).

HSGP: Functional Calculus

\[ -\nabla^2 f(x) = \int_{\Omega} \overbrace{\left[\sum_{j} \lambda_{j} \phi_{j}(x) \phi_{j}(x')\right]}^{l(x, x')} f(x') dx' \]

We can construct powers of \(-\nabla^2\) as

\[ (- \nabla^2)^{s} f(x) = \int_{\Omega} {\color{red}{\overbrace{\left[\sum_{j} \lambda_{j}^{s} \phi_{j}(x) \phi_{j}(x')\right]}^{l^s(x, x')}}} f(x') dx'. \]

HSGP: Coefficients Identification

Use the formal expansion of \(\mathcal{K}\) in terms of powers of \(\nabla^2\):

\[ \begin{align*} & \left[ a_{0} + a_{1}(-\nabla^2) + a_{2}(-\nabla^2)^2 + \cdots \right]f(x) = \\ &\int_{\Omega} \left[a_{0} + a_{1} l(x, x') + a_{2} l^{2}(x, x') + \cdots \right] f(x') dx' \end{align*} \]

This implies we can approximate the kernel as

\[ \begin{align*} k(x, x') \approx & \: a_{0} + a_{1} l(x, x') + a_{2} l^{2}(x, x') + \cdots \\ \approx & \sum_{j} {\color{red}{\underbrace{\left[ a_{0} + a_{1} \lambda_{j} + a_{2} \lambda_{j}^2 + \cdots \right]}_{S(\sqrt{\lambda_{j}})}}} \phi_{j}(x) \phi_{j}(x') \end{align*} \]

HSGP: Final Formula

In summary, we have the following approximation formula for the kernel function:

\[ \boxed{ k(x, x') \approx \sum_{j}^{m} \color{red}{S(\sqrt{\lambda_j})}\color{blue}{\phi_{j}(x) \phi_{j}(x')} } \]

That is, the model of the Gaussian process \(f\) can be written as

\[ f(x) \sim \text{MultivariateNormal}(\boldsymbol{\mu}, \Phi\mathcal{D}\Phi^{T}) \]

where \(\mathcal{D} = \text{diag}(S(\sqrt{\lambda_1}), S(\sqrt{\lambda_2}), \ldots, S(\sqrt{\lambda_{m}}))\).

HSGP: Linear Model

\[ f(x) \approx \sum_{j = 1}^{m} \overbrace{\color{red}{\left(S(\sqrt{\lambda_j})\right)^{1/2}}}^{\text{all hyperparameters are here!}} \times \underbrace{\color{blue}{\phi_{j}(x)}}_{\text{easy to compute!}} \times \overbrace{\color{green}{\beta_{j}}}^{\sim \: \text{Normal}(0,1)} \]

Note

The only dependence on the hyperparameters is through the spectral density.

Computational Cost

The computational cost of evaluating the log posterior density of univariate HSGPs scales as \(\mathcal{O}(nm + m)\).

Squared Exponential \(1\)-dim

\[ \begin{align*} k(x, x') \approx \sum_{j=1}^{m} & \color{red}{\overbrace{\left(a^2 \sqrt{2 \pi} \ell \exp\left(-2\pi^2\ell^2 \left(\frac{\pi j}{2L}\right)^2 \right)\right)^{1/2}}^{\left(S(\sqrt{\lambda_j})\right)^{1/2}}} \\ & \times \color{blue}{\overbrace{\left(\sqrt{\frac{1}{L}} \sin\left(\frac{\pi j (x + L)}{2L}\right)\right)}^{\phi_{j}(x)}} \\ & \times \color{green}{\overbrace{\beta_{j}}^{\sim \: \text{Normal}(0, 1)}} \end{align*} \]

Hilbert Space Approximation (Recap)

%%{init: {"theme": "white", "themeVariables": {"fontSize": "54px"}, "flowchart":{"htmlLabels":false}}}%%

flowchart TD

kernel["kernel"] --> spectral_sensity["Spectral Density"]

spectral_sensity --> polynomial["Polynomial Expansion"]

laplacian["Laplacian"] --> fourier["Fourier Transform"]

laplacian --> dirichlet["Dirichlet's BC"]

dirichlet --> spectral_decomposition["Spectral Decomposition"]

spectral_decomposition["Spectral Decomposition"] --> functional["Functional Calculus"]

polynomial --> identify_coefficients["Identify Coefficients"]

fourier --> identify_coefficients

functional --> identify_coefficients

identify_coefficients --> approximation["Approximation Formula"]

Laplace Eigenfunctions

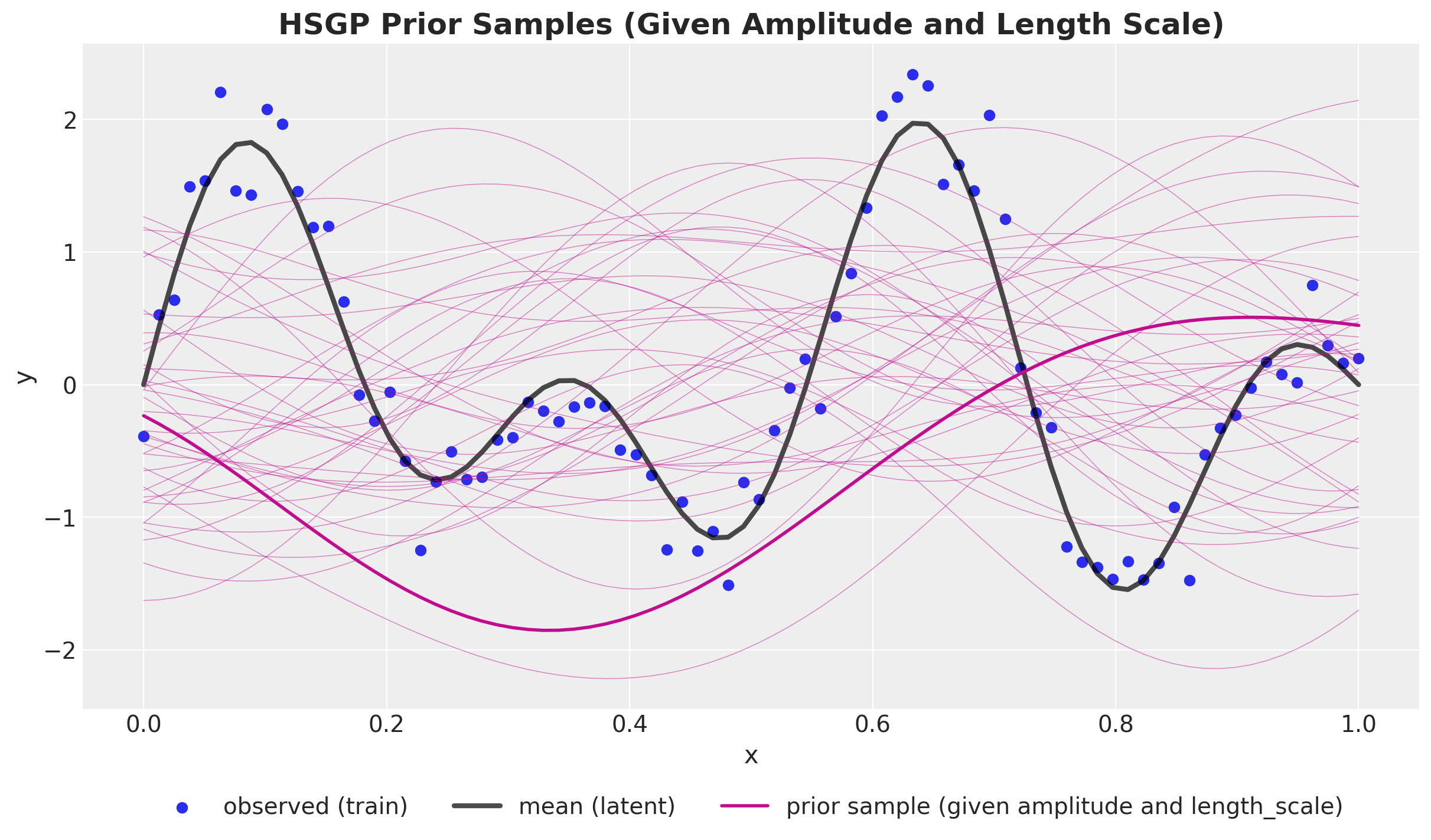

Back to the example …

Prior Predictive

PyMC Implementation

HSGP Class

with pm.Model() as hsgp_pymc_model:

x_data = pm.MutableData("x_data", value=x_train)

y_data = pm.MutableData("y_data", y_train_obs)

kernel_amplitude = pm.InverseGamma("kernel_amplitude", ...)

kernel_length_scale = pm.InverseGamma("kernel_length_scale", ...)

noise = pm.InverseGamma("noise", ...)

mean = pm.gp.mean.Zero()

cov = kernel_amplitude**2 * pm.gp.cov.ExpQuad(

input_dim=1, ls=kernel_length_scale

)

gp = pm.gp.HSGP(m=[20], L=[1.3], mean_func=mean, cov_func=cov)

f = gp.prior("f", X=x_data[:, None])

pm.Normal("likelihood", mu=f, sigma=noise, observed=y_data)Out-of-Sample Predictions

conditional method

with hsgp_pymc_model:

x_star_data = pm.MutableData("x_star_data", x_test)

f_star = gp.conditional("f_star", x_star_data[:, None])

pm.set_data({"x_data": x_test, "y_data": np.ones_like(x_test)})

hsgp_pymc_idata.extend(

pm.sample_posterior_predictive(

trace=hsgp_pymc_idata,

var_names=["f_star", "likelihood"],

random_seed=rng_subkey[1].item(),

)

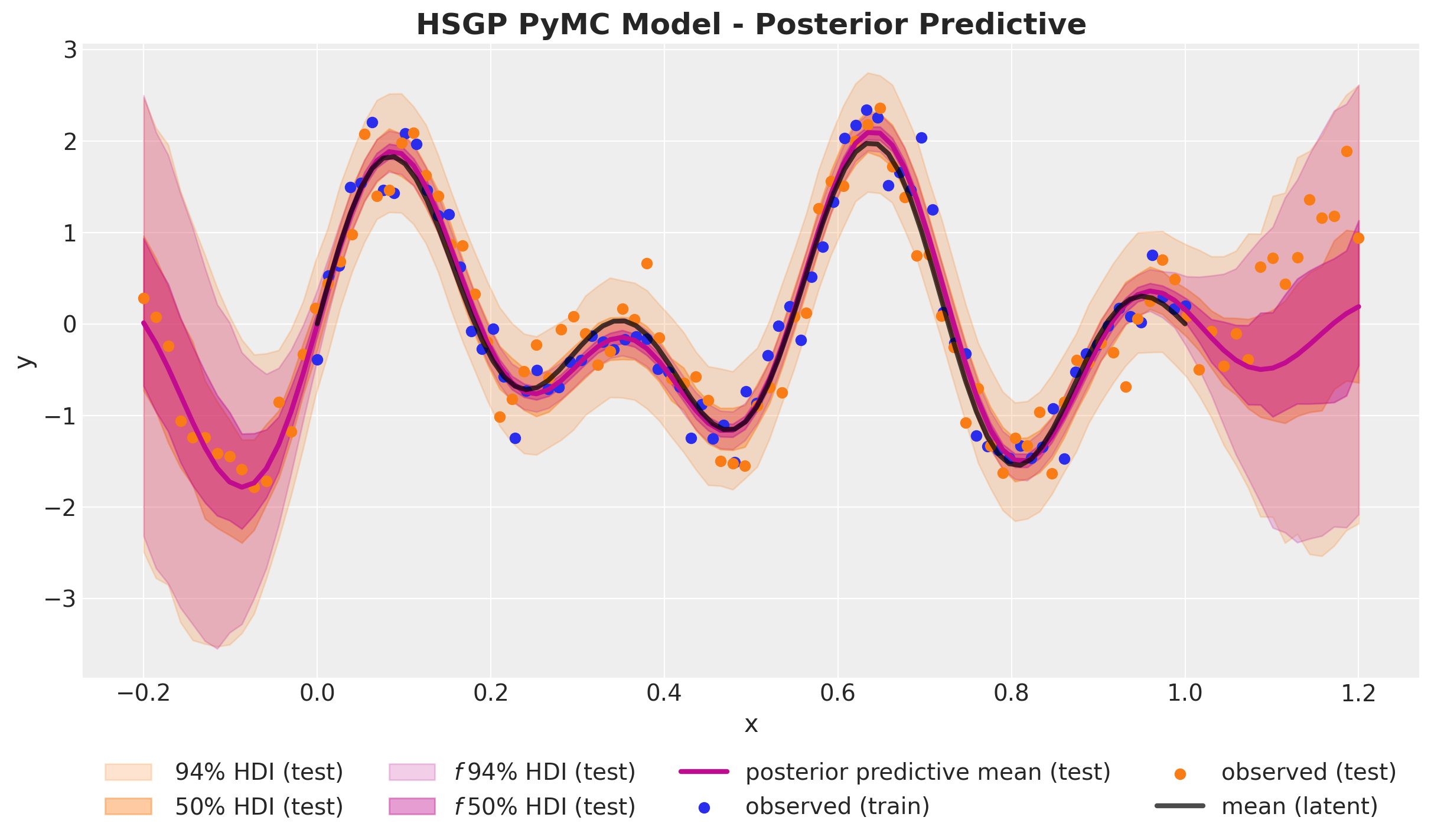

)HSGP Model - Posterior Predictive

PyMC Implementation

HSGP.prior_linearized

with pm.Model() as hsgp_linearized_pymc_model:

x_data = pm.MutableData("x_data", value=x_train)

y_data = pm.MutableData("y_data", y_train_obs)

kernel_amplitude = pm.InverseGamma("kernel_amplitude", ...)

kernel_length_scale = pm.InverseGamma("kernel_length_scale", ...)

noise = pm.InverseGamma("noise", ...)

mean = pm.gp.mean.Zero()

cov = kernel_amplitude**2 * pm.gp.cov.ExpQuad(input_dim=1, ls=kernel_length_scale)

gp = pm.gp.HSGP(m=[20], L=[1.3], mean_func=mean, cov_func=cov)

phi, sqrt_psd = gp.prior_linearized(Xs=x_data_centered[:, None])

beta = pm.Normal("beta", mu=0, sigma=1, size=gp._m_star)

f = pm.Deterministic("f", phi @ (beta * sqrt_psd))

pm.Normal("likelihood", mu=f, sigma=noise, observed=y_data)Out-of-Sample Predictions

pm.set_data method

Example: Birthdays Dataset

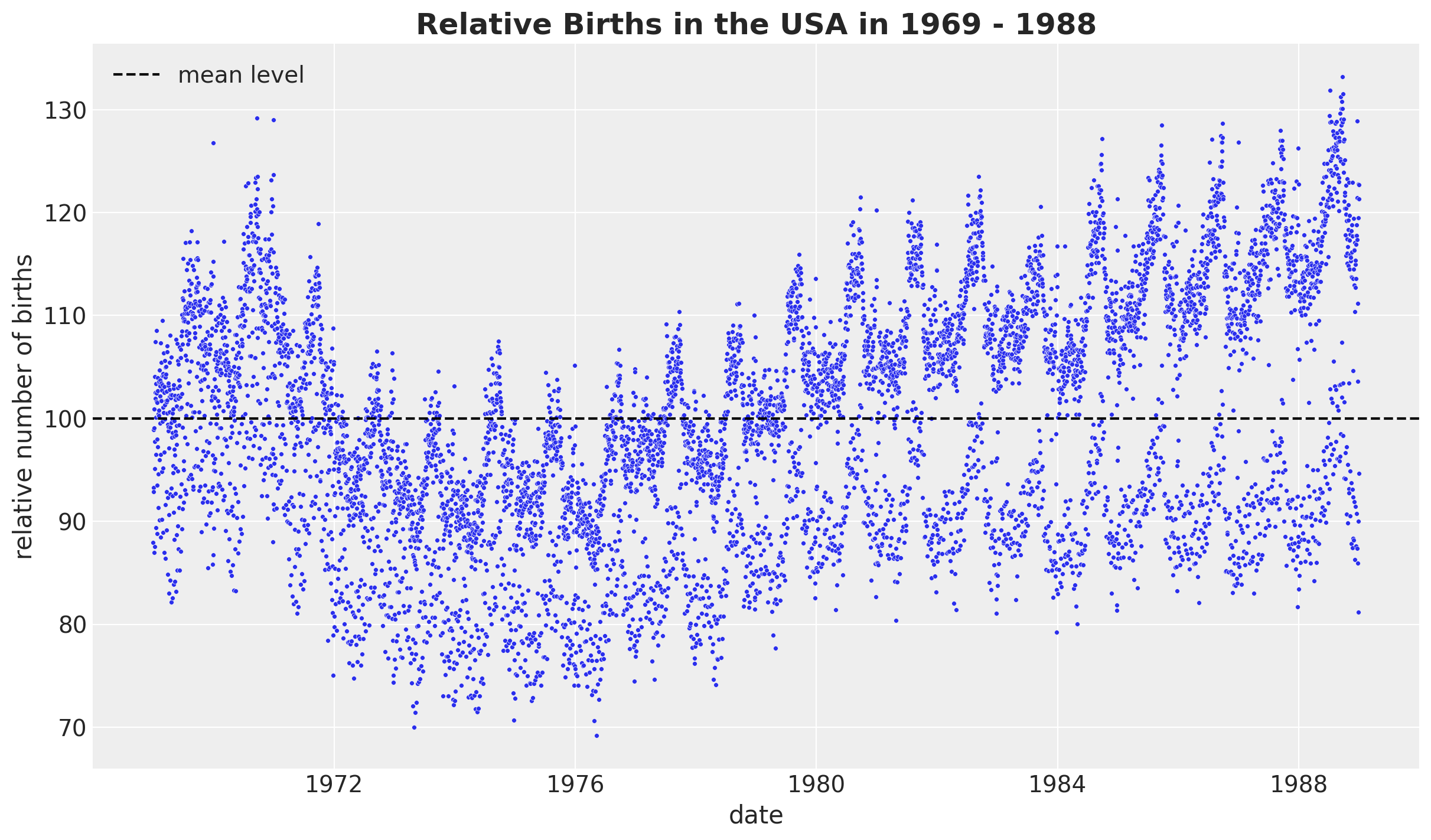

The Birthdays Dataset

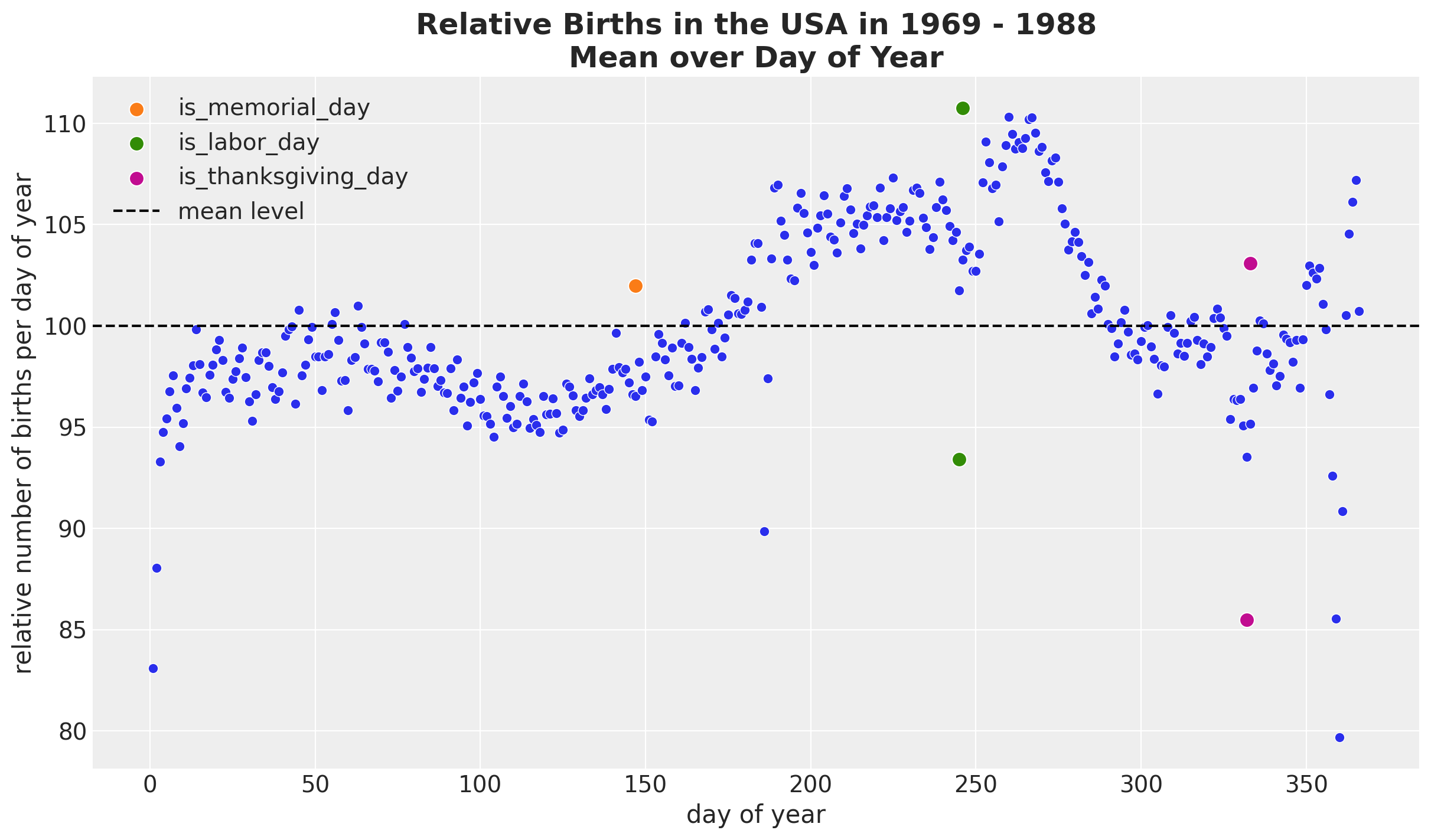

Seasonal Patterns - Day of Year

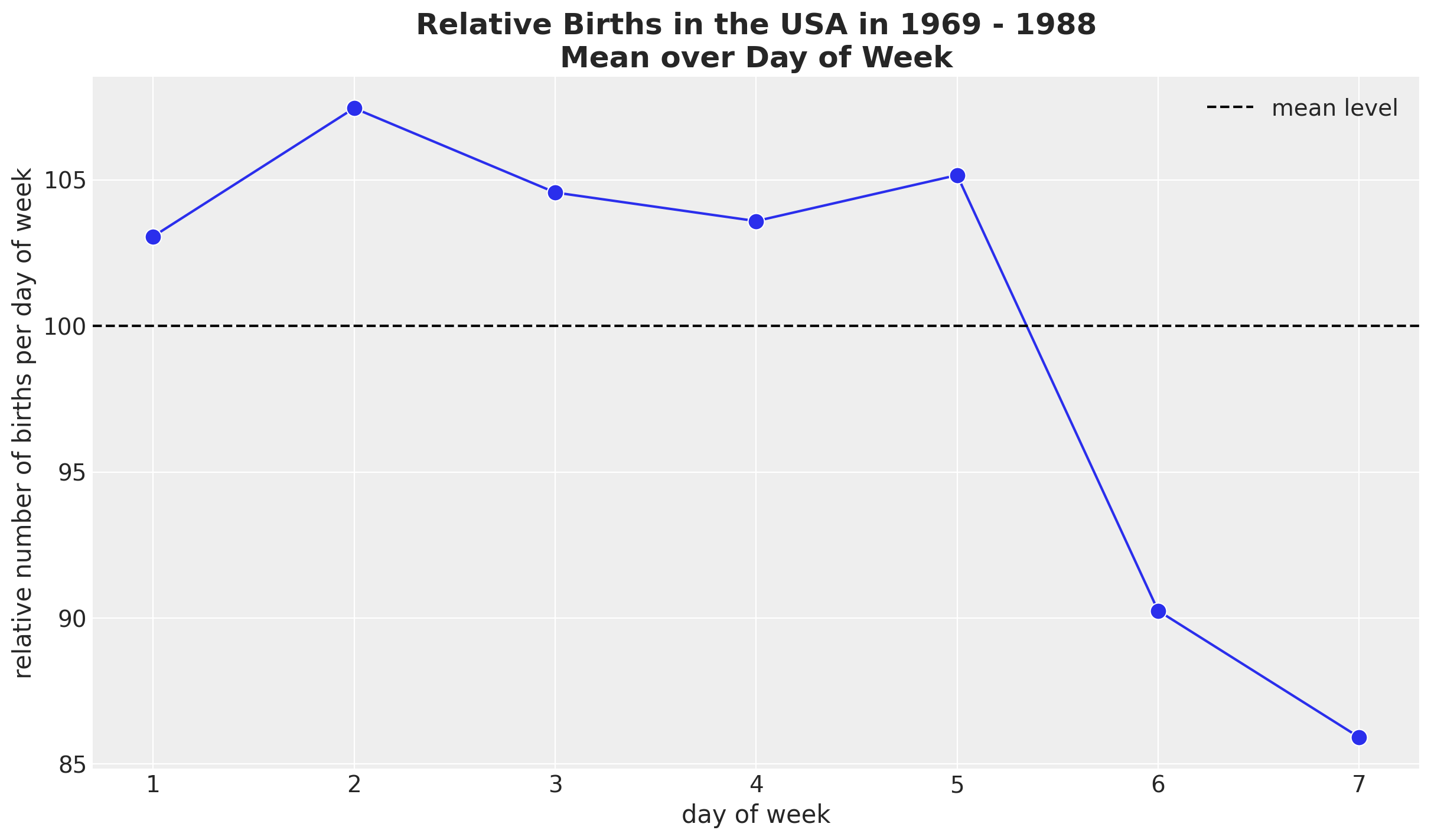

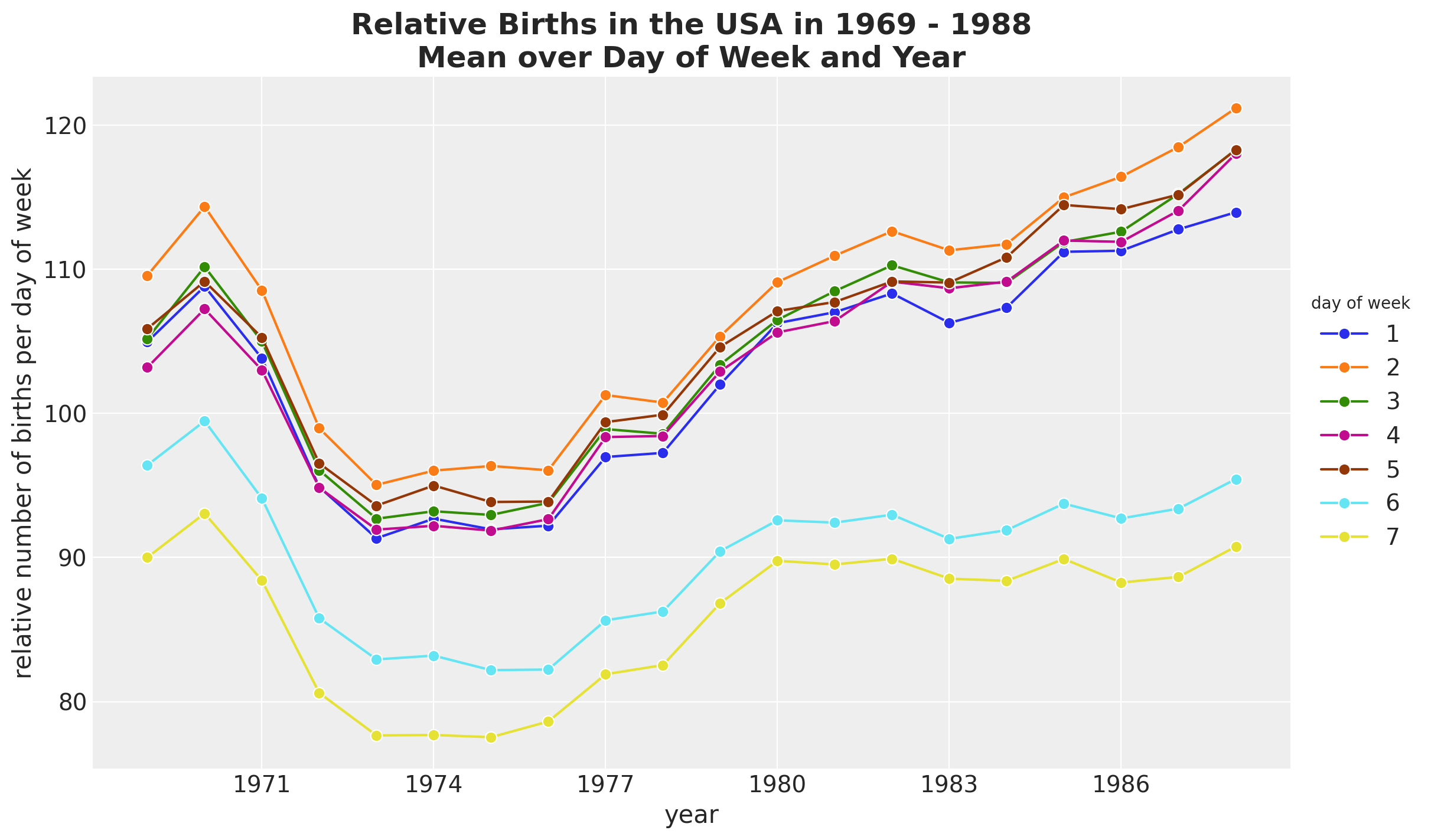

Seasonal Patterns - Day of Week

Seasonal Patterns - Day of Week

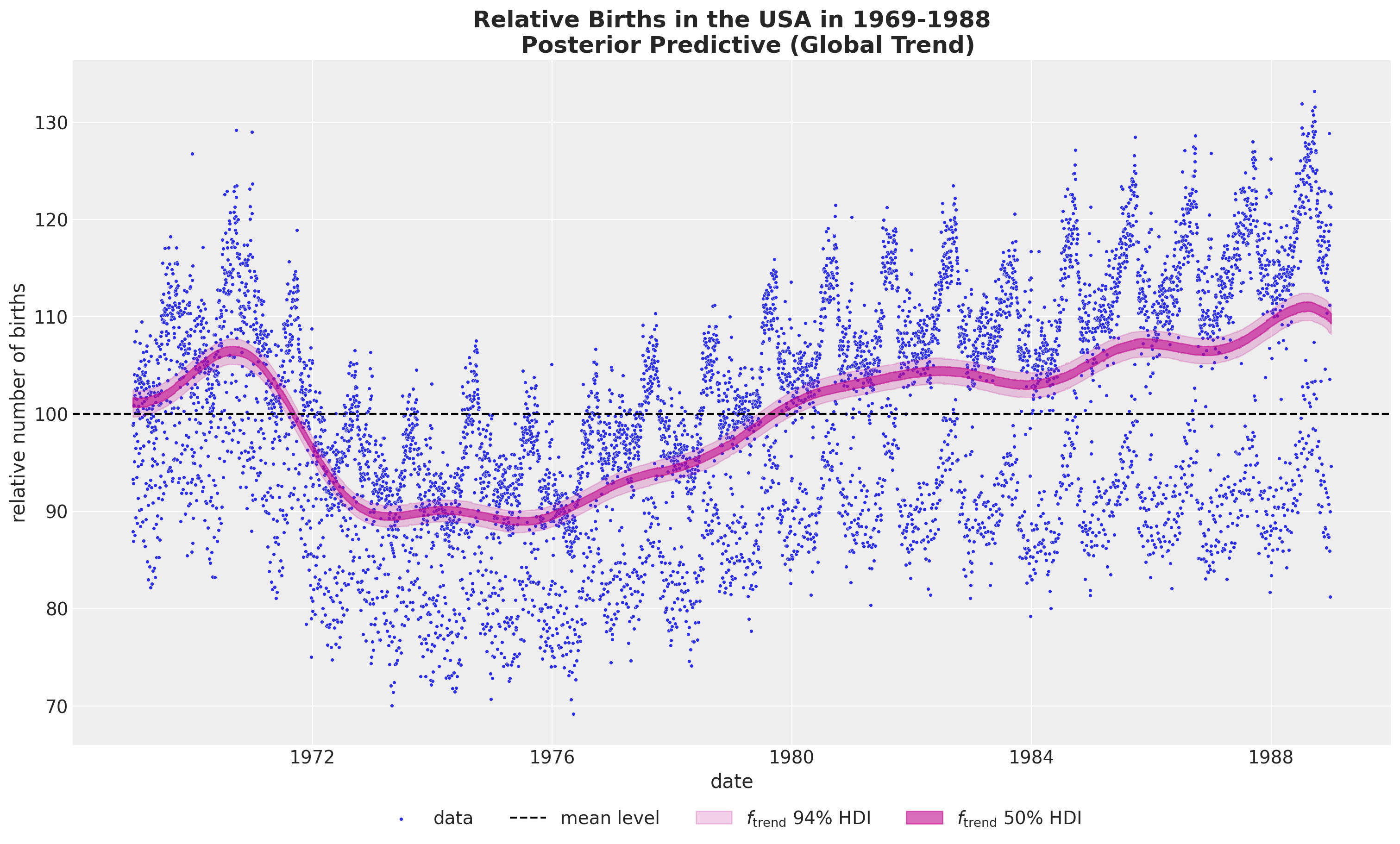

HSGP Model - Trend

We use a Gaussian process with a squared exponential kernel.

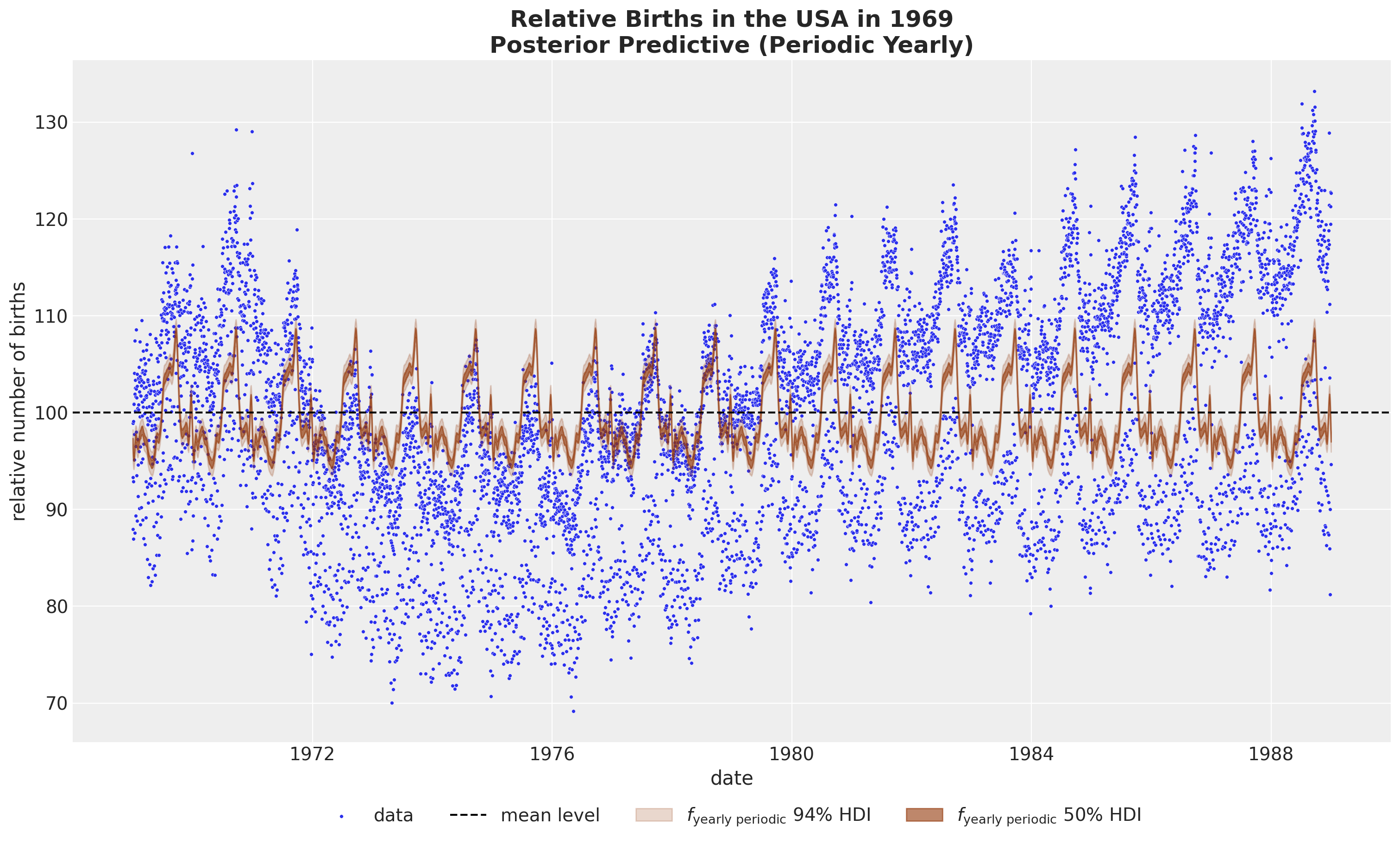

HSGP Model - Yearly Seasonality

We use a Gaussian process with a periodic kernel*.

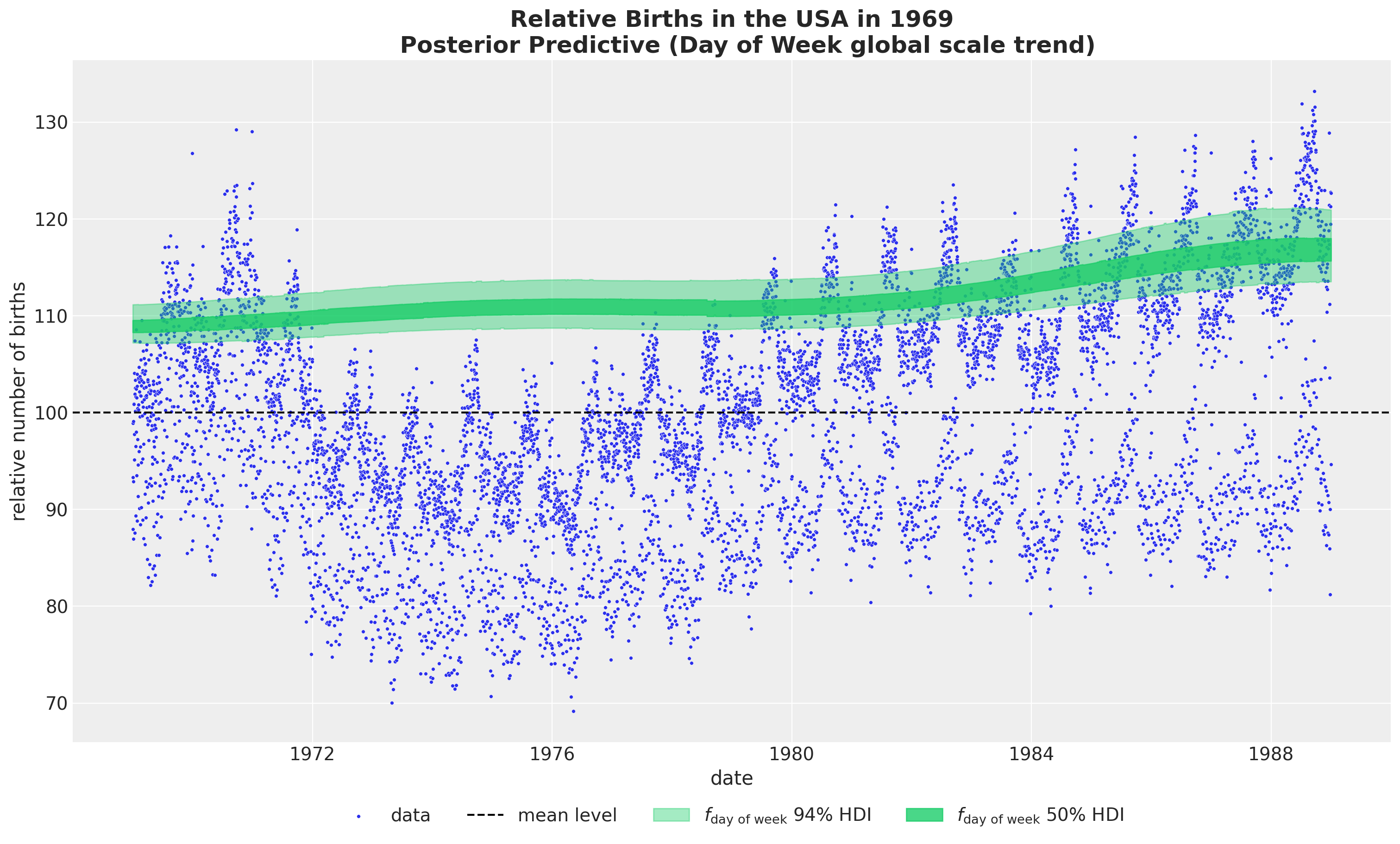

HSGP Model - Weekly Seasonality

We use a ZeroSumNormal distribution to capture the relative difference across weekdays. We couple it with a multiplicative factor parametrized by a Gaussian process.

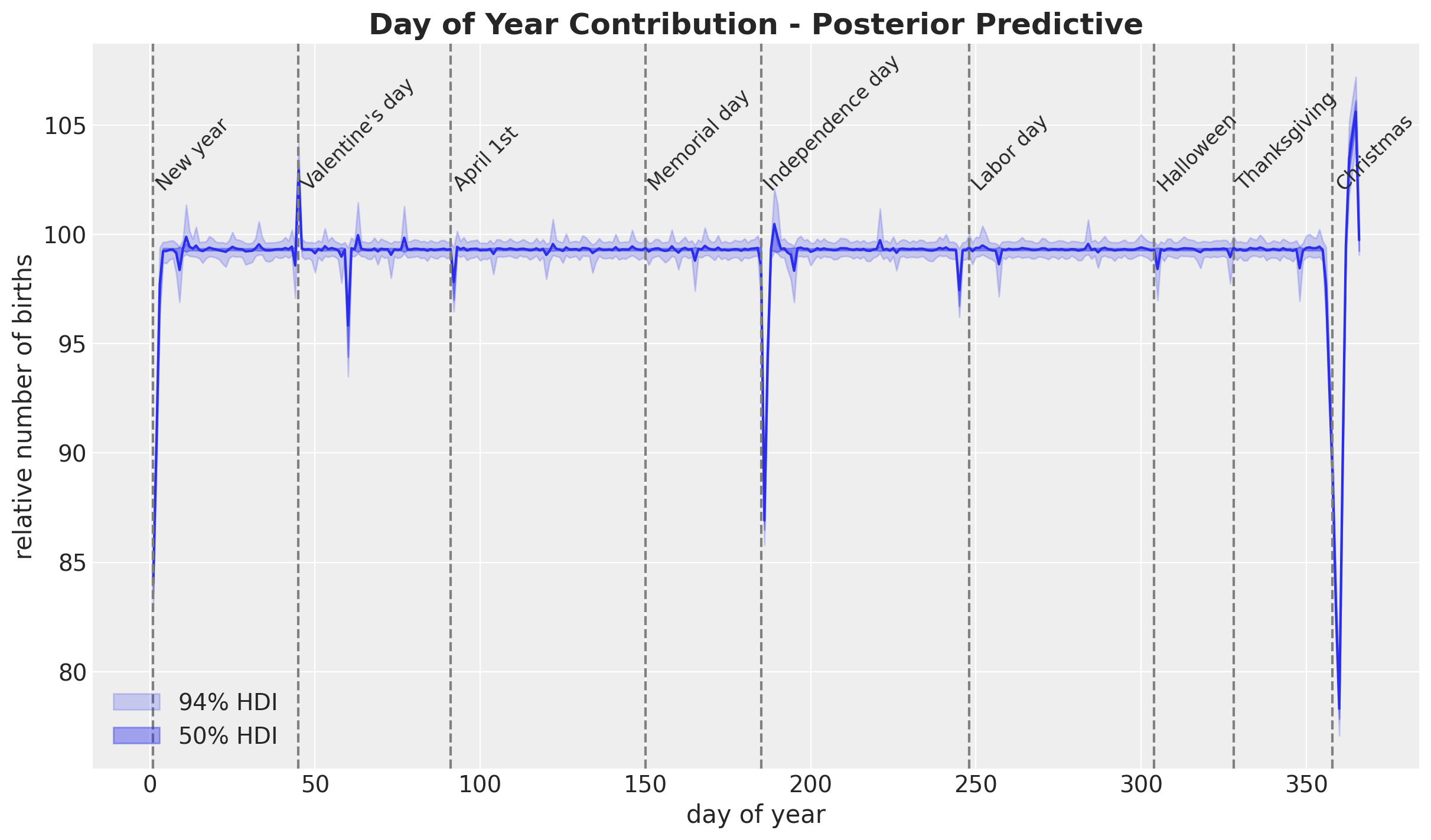

HSGP Model - Special Days

We use a StudentT distribution over the day_of_year2.

References

Gaussian Processes

- Gaussian Processes for Machine Learning, classic book on GPs.

- PyMC Examples: Mean and Covariance Functions

- Bayesian Regression as a Gaussian Process

- An Introduction to Gaussian Process Regression

- Robust Gaussian Process Modeling, very complete introduction to GPs.

- Dan Simpson’s Blog, many posts on GPs and prior selection.

HSGP Approximation

References

Birthdays Dataset

- Bayesian workflow book - Birthdays

- NumPyro Example: Hilbert space approximation for Gaussian processes

- Time Series Modeling with HSGP: Baby Births Example

Spectral Theory

Thank you!

![]()