This example is part of the NumPyro Forecast documentation; see here.

This notebook extends that example by training on the full dataset (\(50K\) time series) on a GPU via Modal. The end-to end notebook runs in approximately \(10\) minutes on GPU 🚀!

The FreshRetailNet-50K dataset (Yang et al., 2025) contains \(50{,}000\) daily store-product demand series from fresh retail operations: \(90\) days per series, with hourly sales, hourly stockout labels, and promotion, discount, and calendar covariates. The native stockout labels make it a great public benchmark for a classic operational problem: observed sales are a censored version of demand, because a store cannot sell what is not on the shelf.

We model this with a multiplicative availability factor: expected sales factor into a demand component and an availability component. A forecasting model describes what demand would be with the product fully in stock, and a multiplicative factor, a function of the day’s recorded availability with parameters learned from the data, scales that demand down when it was not. In this example the two components are:

- Forecasting model: a state space model with a trend, weekly seasonality, and promotion effects.

- Availability factor: a saturating function of the day’s stock availability.

The rationale is simple: when a product is out of stock, recorded sales say little about demand, and without an explicit correction the forecasting model would misread stockout days as low-demand days. The factorization also pays off at prediction time: because the demand component describes what would sell with the product fully in stock, setting availability to one over the forecast horizon turns the sales forecast into a demand forecast, which is the number a planner should order against.

There is a catch, though, and it is the heart of this example: days whose stockout labels say the product was out of stock all day still record positive sales about \(15\%\) of the time. A pure multiplicative factor forces the mean to zero on those days and badly misfits them. The likely reason is that the stockout labels are reconstructed from imperfect inventory snapshots, so they carry noise, a common situation in practice. The model developed in this notebook absorbs the contradiction by learning a floor in the availability factor: even at zero recorded availability, a small share of demand can still be sold.

We proceed in four steps. First, an exploratory analysis of the full \(50{,}000\)-series dataset: we look closely at the stockout and availability labels, quantify the contradiction above, and trace it to label noise concentrated in hours that carry almost no demand, which motivates both a sales-weighted availability feature and the learned floor in the availability factor. Second, we fit a hierarchical state space model to the full \(50{,}000\)-series panel with SVI and a custom optax optimizer on a GPU, wrapping the results in an ArviZ DataTree. Third, we evaluate the forecasts with CRPS and central-interval coverage on a simple train-test split against a seasonal-naive baseline. Fourth, we re-issue the forecast with availability pinned to one over the horizon: a counterfactual estimate of uncensored demand that is deliberately not meant to track the observed (censored) sales, and is exactly what a business should plan against, since nobody knows future availability at prediction time. We close by inspecting what the model learned: the fitted availability factor, the store hierarchy, and the promotion contributions. This notebook is the GPU variant of the fresh retail stockout example: the same model and analysis, run on the whole dataset with the package’s memory-bounding knobs (predictive_batch_size, device="host") sized for an accelerator.

Prepare notebook

The first cell installs numpyro_forecastwith the CUDA extras, and numpyro.set_platform("cuda") below places all computation on the GPU. The memory levers used later in the notebook (chunked posterior and predictive sampling, host offload with device="host") are what make the full \(50{,}000\)-series panel fit on a single accelerator.

uv pip install "numpyro_forecast[all_cuda]We now load the packages we will use.

from collections.abc import Callable

from typing import Any, cast

import arviz as az

import jax

import jax.numpy as jnp

import matplotlib.dates as mdates

import matplotlib.lines as mlines

import matplotlib.pyplot as plt

import numpy as np

import numpyro

import numpyro.distributions as dist

import optax

import polars as pl

import preliz as pz

import xarray as xr

from huggingface_hub import hf_hub_download

from huggingface_hub import logging as hf_logging

from jax import random

from jaxtyping import Float, Int

from matplotlib import ticker as mtick

from numpyro import handlers

from numpyro.infer import Predictive

from numpyro.infer.reparam import LocScaleReparam

from sklearn.preprocessing import LabelEncoder

from numpyro_forecast import (

Forecaster,

ForecastingModel,

eval_coverage,

eval_crps,

predictions_to_datatree,

to_datatree,

)

from numpyro_forecast.features import periodic_repeat

from numpyro_forecast.functional import draw_posterior, fit_svi, forecast, predict_in_sample

from numpyro_forecast.metrics import crps_empirical

from numpyro_forecast.typing import Array

az.style.use("arviz-darkgrid")

plt.rcParams["figure.figsize"] = [12, 7]

plt.rcParams["figure.dpi"] = 100

plt.rcParams["figure.facecolor"] = "white"

# Render polars tables without truncating string cells, and drop the shape and

# dtype headers, which are noise in a rendered document.

pl.Config.set_fmt_str_lengths(100)

pl.Config.set_tbl_hide_dataframe_shape(True)

pl.Config.set_tbl_hide_column_data_types(True)

# The Hub intermittently sends an unauthenticated-request warning header on

# responses, which huggingface_hub logs to stderr; the example needs no token,

# so keep the rendered document clean.

hf_logging.set_verbosity_error()

numpyro.set_platform("cuda")

rng_key = random.PRNGKey(seed=42)

%load_ext autoreload

%autoreload 2

%load_ext jaxtyping

%jaxtyping.typechecker beartype.beartype

%config InlineBackend.figure_format = "retina"Read data

We download the training split (a single parquet file, cached locally by huggingface_hub) and scan it lazily with polars, so the full-dataset aggregations below stream instead of materializing all \(4.5\) million rows.

parquet_path: str = hf_hub_download(

repo_id="Dingdong-Inc/FreshRetailNet-50K",

filename="data/train.parquet",

repo_type="dataset",

)

data_lf: pl.LazyFrame = pl.scan_parquet(parquet_path)

data_lf.collect_schema()data/train.parquet: reconstructing file: 0%| | 0.00B / 106MB

data/train.parquet: downloading bytes: | 0.00B

Schema([('city_id', Int64),

('store_id', Int64),

('management_group_id', Int64),

('first_category_id', Int64),

('second_category_id', Int64),

('third_category_id', Int64),

('product_id', Int64),

('dt', String),

('sale_amount', Float64),

('hours_sale', List(Float64)),

('stock_hour6_22_cnt', Int32),

('hours_stock_status', List(Int64)),

('discount', Float64),

('holiday_flag', Int32),

('activity_flag', Int32),

('precpt', Float64),

('avg_temperature', Float64),

('avg_humidity', Float64),

('avg_wind_level', Float64)])data_lf.select(

pl.len().alias("rows"),

pl.col("city_id").n_unique().alias("cities"),

pl.col("store_id").n_unique().alias("stores"),

pl.col("product_id").n_unique().alias("products"),

pl.struct(["store_id", "product_id"]).n_unique().alias("series"),

pl.col("dt").min().alias("start_date"),

pl.col("dt").max().alias("end_date"),

).collect(engine="streaming")| rows | cities | stores | products | series | start_date | end_date |

|---|---|---|---|---|---|---|

| 4500000 | 18 | 898 | 865 | 50000 | "2024-03-28" | "2024-06-25" |

Every one of the \(50{,}000\) store-product series covers the same \(90\) days. Three columns drive this notebook:

sale_amountis the daily sales target, andhours_saleis its hourly decomposition (it sums tosale_amountup to float rounding).hours_stock_statusis a \(24\)-vector of hourly stockout indicators (\(1\) means out of stock in that hour).stock_hour6_22_cntcounts stockout hours within the \(6{:}00\) to \(22{:}00\) daytime window, so its maximum is \(16\).

The next cell verifies these conventions directly instead of trusting the documentation.

data_lf.select(

(pl.col("hours_sale").list.sum() - pl.col("sale_amount")).abs().max().alias("max_abs_diff"),

pl.col("hours_stock_status").list.len().max().alias("hours_per_day"),

pl.col("stock_hour6_22_cnt").max().alias("max_daytime_stockout_hours"),

).collect(engine="streaming")| max_abs_diff | hours_per_day | max_daytime_stockout_hours |

|---|---|---|

| 1.4211e-14 | 24 | 16 |

Exploratory data analysis

The queries in this section are built from small named polars expression functions, chained with pipe for the frame-level steps, so each query reads top to bottom. The expressions defined along the way (stockout hours, scaled sales, the sales-weighted availability) are reused all the way into the modeling panel.

How prevalent are stockouts?

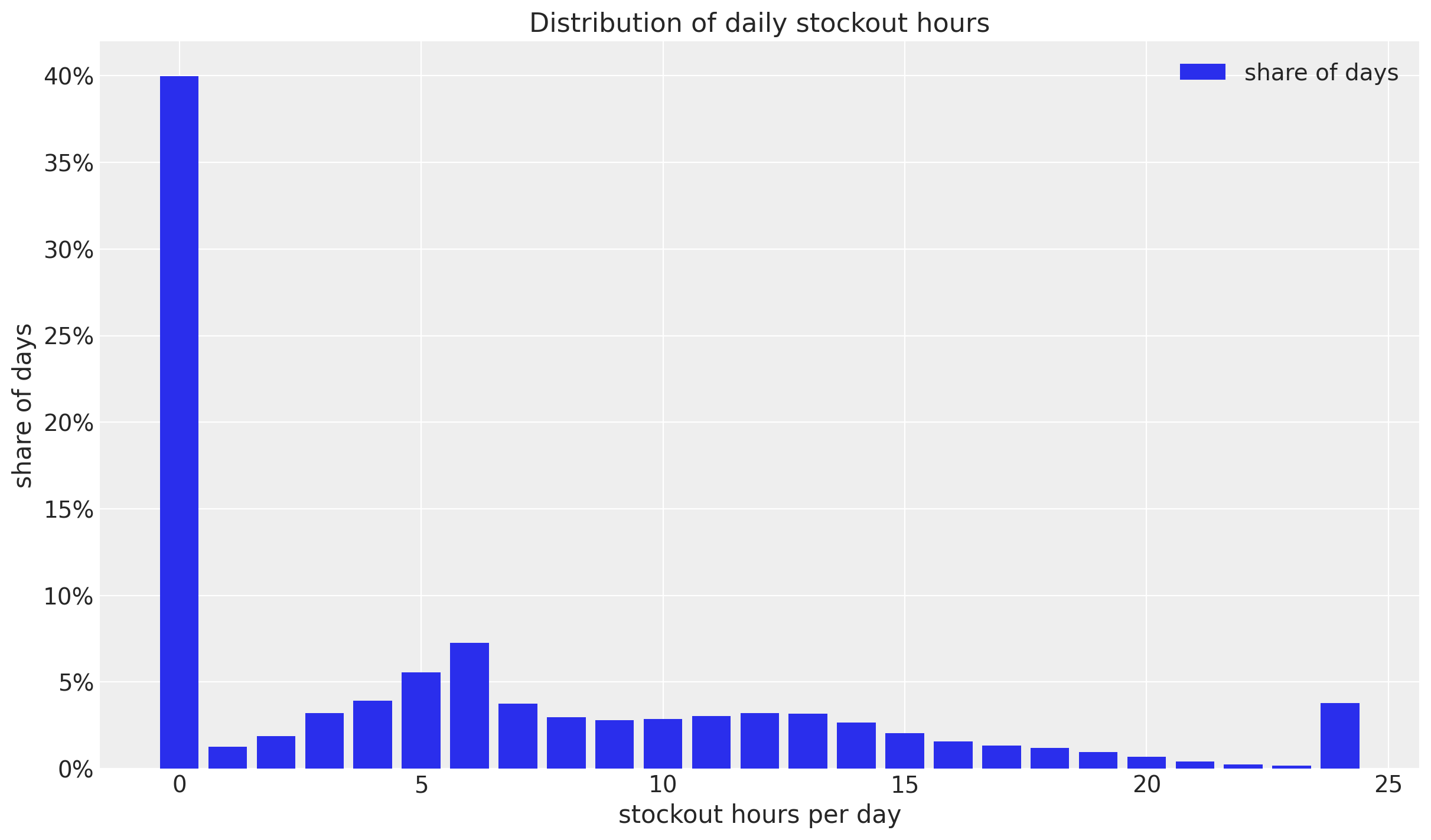

def stockout_hours() -> pl.Expr:

"""Count the hours of the day flagged out of stock."""

return pl.col("hours_stock_status").list.sum()

stockout_hours_df = (

data_lf.group_by(stockout_hours().alias("stockout_hours"))

.len()

.sort("stockout_hours")

.with_columns((pl.col("len") / pl.col("len").sum()).alias("share_of_days"))

.collect(engine="streaming")

)

fig, ax = plt.subplots()

ax.bar(

stockout_hours_df["stockout_hours"],

stockout_hours_df["share_of_days"],

color="C0",

label="share of days",

)

ax.legend(loc="upper right")

ax.yaxis.set_major_formatter(mtick.PercentFormatter(xmax=1, decimals=0))

ax.set(

xlabel="stockout hours per day",

ylabel="share of days",

title="Distribution of daily stockout hours",

);

The distribution is strongly bimodal: \(40\%\) of the days have no stockout at all, most of the rest lose a handful of hours, and a visible spike of about \(3.8\%\) of the days is flagged out of stock for all \(24\) hours.

The contradiction: sales on fully out-of-stock days

If the labels were exact, a day flagged out of stock for every hour could not sell anything. Let us check that under both stockout definitions (all \(24\) hours flagged, and all \(16\) daytime hours flagged).

max_daytime_hours = 16

def oos_all_day() -> pl.Expr:

"""Day flagged out of stock for all 24 hours."""

return stockout_hours() == 24

def oos_daytime() -> pl.Expr:

"""Day flagged out of stock for all 16 daytime (6:00 to 22:00) hours."""

return pl.col("stock_hour6_22_cnt") == max_daytime_hours

def scaled_sales() -> pl.Expr:

"""Daily sales scaled by the series' own mean, so 1 is an average day."""

return pl.col("sale_amount") / pl.col("sale_amount").mean().over("store_id", "product_id")

def share_positive_sales_when(flag: pl.Expr) -> pl.Expr:

"""Share of days with positive sales among the days where ``flag`` holds."""

return (pl.col("sale_amount") > 0).filter(flag).mean()

data_lf.select(

oos_all_day().mean().alias("share_days_oos_all_day"),

oos_daytime().mean().alias("share_days_oos_daytime"),

share_positive_sales_when(oos_all_day()).alias("p_sales_oos_all_day"),

share_positive_sales_when(oos_daytime()).alias("p_sales_oos_daytime"),

scaled_sales()

.filter(oos_all_day() & (pl.col("sale_amount") > 0))

.mean()

.alias("relative_sales_when_positive"),

).collect(engine="streaming")| share_days_oos_all_day | share_days_oos_daytime | p_sales_oos_all_day | p_sales_oos_daytime | relative_sales_when_positive |

|---|---|---|---|---|

| 0.037937 | 0.040398 | 0.147589 | 0.185631 | 0.248096 |

About \(15\%\) of the all-day stockout days (and \(19\%\) of the daytime ones) still record positive sales, and when they do the amount is not negligible: about a quarter of the series’ average daily sales. Plausible mechanisms are stockout labels reconstructed from inventory snapshots, a sell-out followed by a restock within the same hour, or back-room stock that never registered on the shelf system. Whatever the cause, the labels are noisy, and a model that pins the mean at zero whenever recorded availability is zero is misspecified.

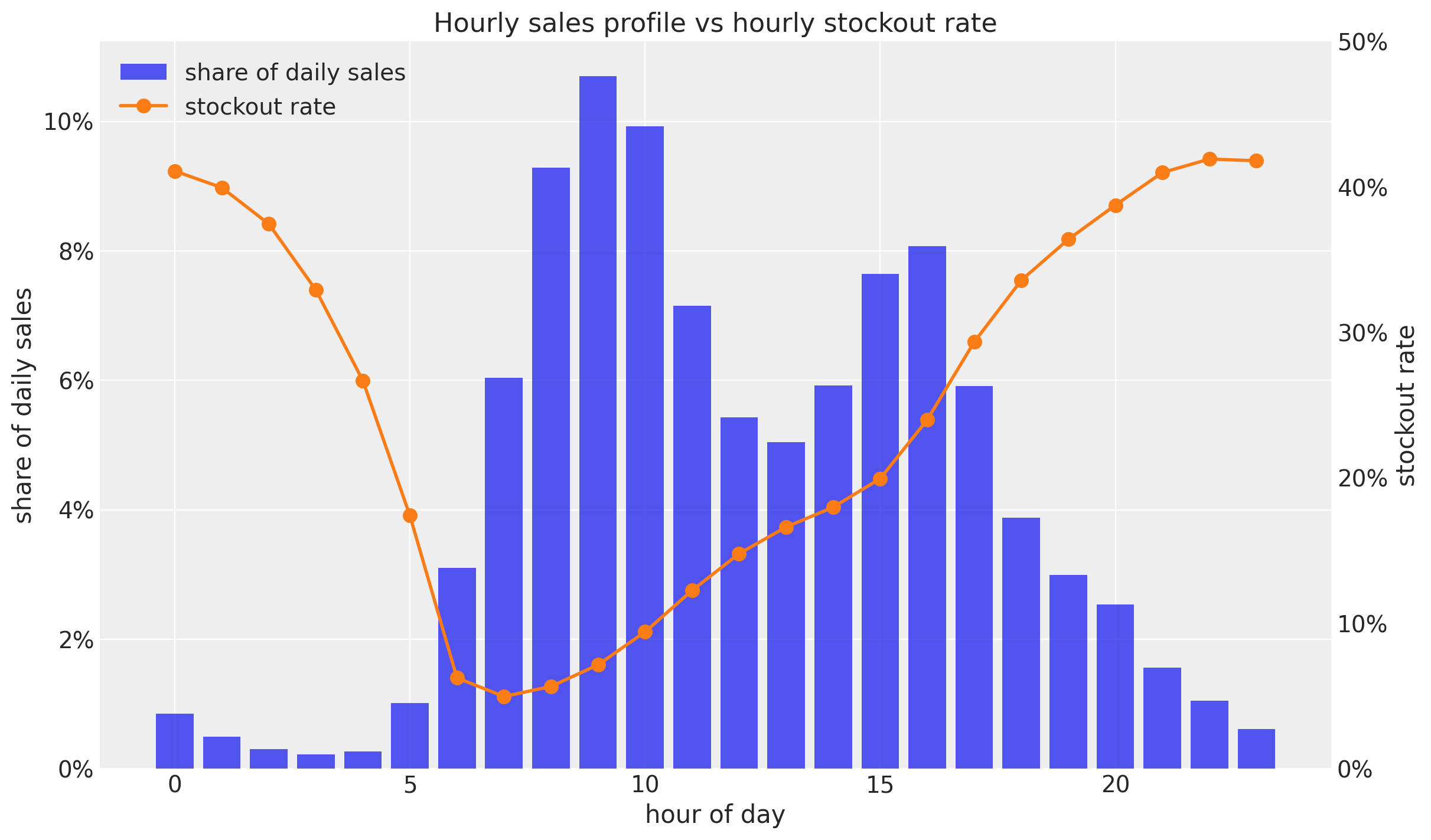

When do sales and stockouts happen within the day?

The hourly decomposition tells us how much each flagged hour actually matters for daily demand.

def total_sales_in_hour(hour: int) -> pl.Expr:

"""Total sales recorded in one hour of the day, over the full dataset."""

return pl.col("hours_sale").list.get(hour).sum()

def stockout_rate_in_hour(hour: int) -> pl.Expr:

"""Share of days flagged out of stock in one hour of the day."""

return pl.col("hours_stock_status").list.get(hour).mean()

hourly_row = (

data_lf.select(

*[total_sales_in_hour(h).alias(f"sales_{h}") for h in range(24)],

*[stockout_rate_in_hour(h).alias(f"oos_{h}") for h in range(24)],

)

.collect(engine="streaming")

.row(0)

)

sales_by_hour = np.asarray(hourly_row[:24], dtype=np.float64)

stockout_rate_by_hour = np.asarray(hourly_row[24:], dtype=np.float64)

hourly_weights = sales_by_hour / sales_by_hour.sum()

fig, ax = plt.subplots()

ax.bar(np.arange(24), hourly_weights, color="C0", alpha=0.8, label="share of daily sales")

ax_twin = ax.twinx()

ax_twin.plot(

np.arange(24),

stockout_rate_by_hour,

color="C1",

marker="o",

markersize=8,

linewidth=2,

label="stockout rate",

)

ax_twin.grid(False)

ax_twin.set(ylabel="stockout rate", ylim=(0, 0.5))

handles, bar_labels = ax.get_legend_handles_labels()

handles_twin, labels_twin = ax_twin.get_legend_handles_labels()

ax.legend(handles + handles_twin, bar_labels + labels_twin, loc="upper left")

ax.yaxis.set_major_formatter(mtick.PercentFormatter(xmax=1, decimals=0))

ax_twin.yaxis.set_major_formatter(mtick.PercentFormatter(xmax=1, decimals=0))

ax.set(

xlabel="hour of day",

ylabel="share of daily sales",

title="Hourly sales profile vs hourly stockout rate",

)

print(f"share of sales in the 6:00 to 22:00 window: {hourly_weights[6:22].sum():.1%}")

print(

f"peak hourly stockout rate: {stockout_rate_by_hour.max():.1%} "

f"(hour {int(stockout_rate_by_hour.argmax())})"

)share of sales in the 6:00 to 22:00 window: 95.2%

peak hourly stockout rate: 41.9% (hour 22)

The two curves are almost mirror images: sales concentrate between \(7{:}00\) and \(20{:}00\) (\(95\%\) of all sales fall in the \(6{:}00\) to \(22{:}00\) window), while the stockout rate peaks at \(42\%\) late at night, exactly when nobody is buying. A raw \(24\)-hour stockout count therefore heavily over-penalizes availability. We can also measure the label noise directly: how much of the total sales volume is recorded in hours that are flagged out of stock?

def sales_in_flagged_hours() -> pl.Expr:

"""Sales volume recorded in the hours whose own stockout flag is set."""

return pl.sum_horizontal(

[

(pl.col("hours_sale").list.get(h) * pl.col("hours_stock_status").list.get(h))

for h in range(24)

]

)

data_lf.select(

(sales_in_flagged_hours().sum() / pl.col("hours_sale").list.sum().sum()).alias(

"share_of_sales_in_flagged_stockout_hours"

)

).collect(engine="streaming")| share_of_sales_in_flagged_stockout_hours |

|---|

| 0.025131 |

\(2.5\%\) of all sales happen in hours the labels declare out of stock. This is direct, hour-level evidence that the stockout signal has noise that no availability feature can remove, and it is why the model below learns a floor instead of trusting availability zero to mean demand zero.

A sales-weighted availability feature

Instead of counting stockout hours uniformly, we weight each hour by its share of global sales, so that losing a night hour costs almost nothing and losing the morning peak costs a lot:

\[\begin{align*} a_{t,s} &= \sum_{h=0}^{23} w_h \left(1 - \text{stockout}_{t,s,h}\right), \\ w_h &= \frac{\text{total sales in hour } h}{\text{total sales}}. \end{align*}\]

One note on hygiene: the weights \(w_h\) are a global hour-of-day profile computed over the full dataset, test window included, whereas a deployed system would compute them on history only. We keep the dataset-wide profile for simplicity; the effect of \(14\) extra days on a fixed \(24\)-number profile is negligible, and the availability feature itself is treated as a known future input in the retrospective evaluation set up below anyway.

def sales_weighted_availability(weights: Float[np.ndarray, " hours"]) -> pl.Expr:

"""In-stock share of the day, weighting each hour by its share of global sales."""

return pl.sum_horizontal(

[(1 - pl.col("hours_stock_status").list.get(h)) * float(weights[h]) for h in range(24)]

).alias("availability")

def zero_availability_summary(

lf: pl.LazyFrame, zero_flag: pl.Expr, definition: str

) -> pl.LazyFrame:

"""Summarize the zero-availability days implied by one stockout definition."""

return lf.select(

pl.lit(definition).alias("definition"),

zero_flag.mean().alias("share_days_zero_availability"),

share_positive_sales_when(zero_flag).alias("p_positive_sales_given_zero"),

)

availability_expr: pl.Expr = sales_weighted_availability(hourly_weights)

pl.concat(

[

data_lf.pipe(zero_availability_summary, oos_daytime(), "daytime hours all flagged"),

data_lf.pipe(zero_availability_summary, oos_all_day(), "all 24 hours flagged"),

data_lf.pipe(

zero_availability_summary, availability_expr == 0, "sales-weighted availability = 0"

),

]

).collect(engine="streaming")| definition | share_days_zero_availability | p_positive_sales_given_zero |

|---|---|---|

| "daytime hours all flagged" | 0.040398 | 0.185631 |

| "all 24 hours flagged" | 0.037937 | 0.147589 |

| "sales-weighted availability = 0" | 0.037937 | 0.147589 |

Two remarks on this table. First, because every hour carries a positive share of global sales, the weighted availability is exactly zero only when all \(24\) hours are flagged: its zero set coincides with the all-day definition by construction, and it inherits that definition’s lower \(15\%\) contradiction rate. The daytime definition’s hard zero is both noisier (\(19\%\)) and cruder, since it also zeroes out days that were merely stocked overnight; under the weighted feature those days keep a tiny positive \(a_{t,s}\) instead. Second, the feature’s real contribution lies between the extremes: it grades partial days by how much selling time they lose, so a lost night hour costs almost nothing and a lost morning-peak hour costs a lot. The \(15\%\) that remains at exact zero is irreducible label noise, and the model handles it with a learned floor rather than a data transformation.

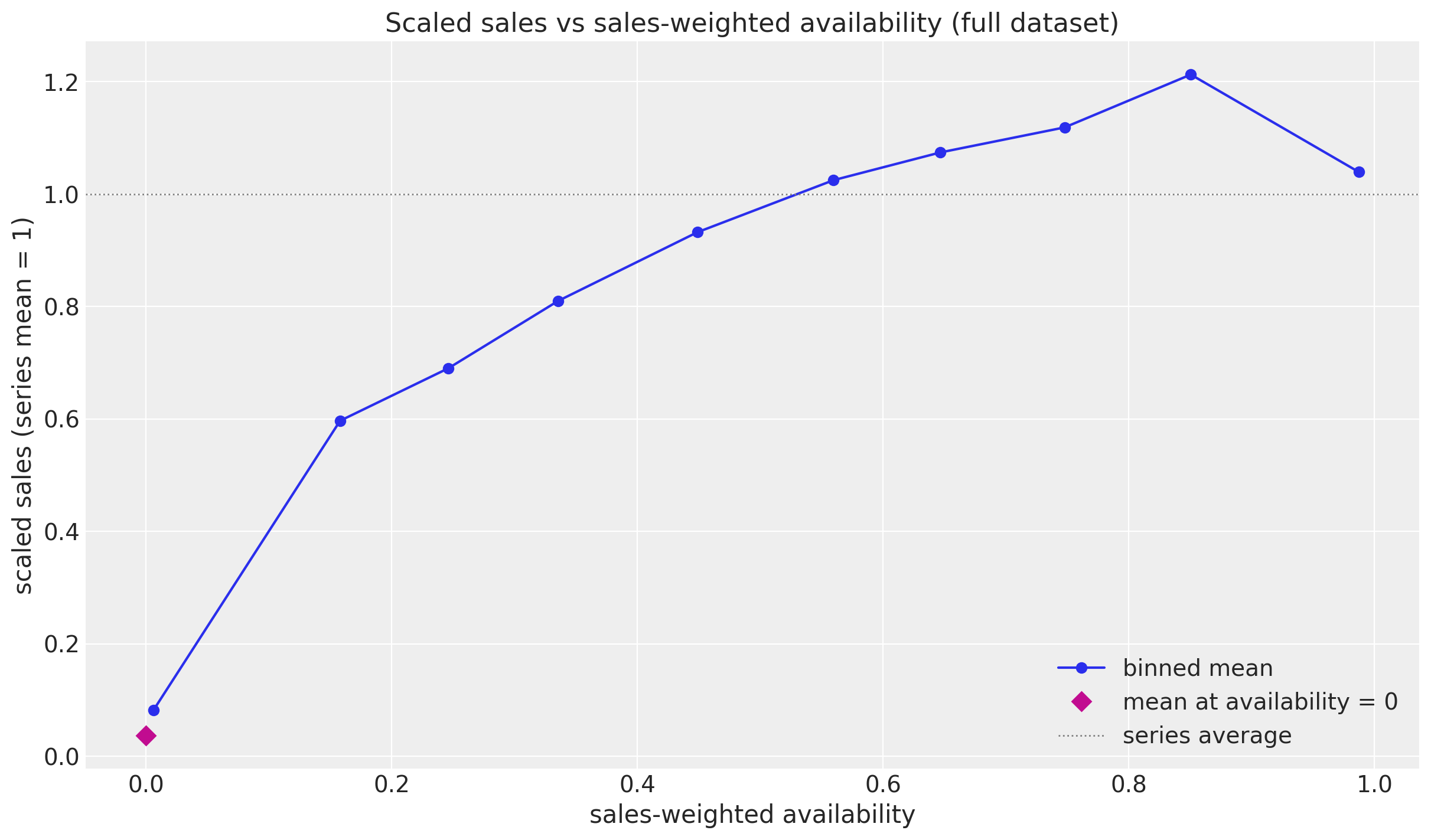

The empirical demand-availability curve

How do sales respond to partial availability? We scale each series by its own mean (so different volumes are comparable) and bin the scaled sales by weighted availability.

def availability_bin() -> pl.Expr:

"""Decile bin (0 to 9) of the sales-weighted availability."""

return (pl.col("availability") * 10).floor().clip(0, 9).alias("availability_bin")

def mean_scaled_sales_by_availability_bin(lf: pl.LazyFrame) -> pl.LazyFrame:

"""Bin the days by availability and average the scaled sales within each bin."""

return (

lf.group_by(availability_bin())

.agg(

pl.col("availability").mean().alias("mean_availability"),

pl.col("scaled_sales").mean().alias("mean_scaled_sales"),

pl.len().alias("days"),

)

.sort("availability_bin")

)

def mean_scaled_sales_at_zero_availability(lf: pl.LazyFrame) -> pl.LazyFrame:

"""Average the scaled sales over the days with zero sales-weighted availability."""

return lf.filter(pl.col("availability") == 0).select(

pl.col("scaled_sales").mean().alias("mean_scaled_sales"),

pl.len().alias("days"),

)

availability_sales_lf = data_lf.with_columns(

availability_expr, scaled_sales().alias("scaled_sales")

)

factor_curve_df = availability_sales_lf.pipe(mean_scaled_sales_by_availability_bin).collect(

engine="streaming"

)

empirical_floor_df = availability_sales_lf.pipe(mean_scaled_sales_at_zero_availability).collect(

engine="streaming"

)

empirical_floor = float(empirical_floor_df["mean_scaled_sales"][0])

fig, ax = plt.subplots()

ax.plot(

factor_curve_df["mean_availability"],

factor_curve_df["mean_scaled_sales"],

"o-",

color="C0",

label="binned mean",

)

ax.plot(0.0, empirical_floor, "D", color="C3", markersize=8, label="mean at availability = 0")

ax.axhline(1.0, color="gray", linestyle=":", linewidth=1, label="series average")

ax.legend(loc="lower right")

ax.set(

xlabel="sales-weighted availability",

ylabel="scaled sales (series mean = 1)",

title="Scaled sales vs sales-weighted availability (full dataset)",

)

print(f"empirical floor at zero availability: {empirical_floor:.3f}")empirical floor at zero availability: 0.037

The curve is saturating, exactly the shape a multiplicative factor should have: steep gains at low availability, flattening out near full availability. Two details matter for the model. First, the value at zero availability is positive (about \(0.04\)), which is the empirical floor the factor must reproduce. Second, the bins just below full availability sit slightly above the fully-available bin. That is endogeneity, not magic: stockouts happen disproportionately on high-demand days (a sell-out is itself evidence of demand), so a naive read of this curve overstates what availability alone does. The model mitigates this by attributing day-to-day variation to the trend, weekly seasonality, and promotion covariates jointly with the factor.

Promotion and calendar covariates

We encode the discount as discount_magnitude = 1 - discount, so zero means no discount and larger values mean deeper discounts (a positive coefficient then reads “more discount, more sales”).

def raw_discount_magnitude() -> pl.Expr:

"""Depth of the discount read literally from the raw column: 1 - discount."""

return 1 - pl.col("discount")

def mean_scaled_sales_when(flag: str, active: bool) -> pl.Expr:

"""Mean scaled sales over the days where a 0/1 flag column is (in)active."""

prefix = "scaled" if active else "scaled_no"

name = flag.removesuffix("_flag")

return scaled_sales().filter(pl.col(flag) == int(active)).mean().alias(f"{prefix}_{name}")

data_lf.select(

raw_discount_magnitude().mean().alias("mean_discount_magnitude"),

(raw_discount_magnitude() > 0).mean().alias("share_days_discounted"),

(pl.col("discount") == 0).mean().alias("share_days_discount_zero"),

pl.col("activity_flag").mean().alias("share_days_activity"),

pl.col("holiday_flag").mean().alias("share_days_holiday"),

mean_scaled_sales_when("activity_flag", active=True),

mean_scaled_sales_when("activity_flag", active=False),

mean_scaled_sales_when("holiday_flag", active=True),

mean_scaled_sales_when("holiday_flag", active=False),

).unpivot().collect(engine="streaming")| variable | value |

|---|---|

| "mean_discount_magnitude" | 0.088859 |

| "share_days_discounted" | 0.515299 |

| "share_days_discount_zero" | 0.003564 |

| "share_days_activity" | 0.378421 |

| "share_days_holiday" | 0.344444 |

| "scaled_activity" | 1.113655 |

| "scaled_no_activity" | 0.930806 |

| "scaled_holiday" | 1.147654 |

| "scaled_no_holiday" | 0.922419 |

Discounts are common (about half of all days, with a mean magnitude near \(9\%\)), promotion activity lifts scaled sales by roughly \(20\%\) on average, and holidays by roughly a quarter. All three are worth including as regression covariates, with effects pooled hierarchically by store. One anomaly to keep in mind: a small share of days (\(0.4\%\) dataset-wide) records discount = 0, which read literally would be a \(100\%\) discount and is far more plausibly an unpriced placeholder; it looks negligible in aggregate, but we will meet it again below, since it is concentrated in exactly the flagship launch product that dominates the series we plot.

Build the modeling panel

We model the full panel: with n_series_panel = 50_000 the top-\(n\) selection below keeps every series. The ranking machinery is retained from the \(1{,}000\)-series CPU variant of this notebook, and its fold discipline still matters whenever a subset is modeled: ranking on the full window would let test-period spikes decide which series get modeled and scored, the same class of leak the scaling discussion below is careful to keep out of the fold. The last \(14\) days are held out as a test set; the model trains on the first \(76\) days and receives the actual covariates (availability, discount, promotion, holiday, launch indicator) over the forecast window, which is the standard retrospective evaluation setup.

Getting from the long dataframe to model-ready arrays is worth doing carefully, because every shape convention we set here is relied on by the model and by the ArviZ export. We proceed in five steps: pivot the long panel into dense (time, series) arrays, scale each series by its own training mean, build the integer store index that drives the hierarchical pooling, add the panel-wide launch indicator, and stack all exogenous inputs into a single tensor with named axes.

One data decision happens right in the panel build: the placeholder discount = 0 days flagged in the EDA are encoded as no discount (and the handful of discount > 1 artifacts are clipped). The feature itself stays in the model; the encoding fix is what makes its coefficient read as a genuine discount effect rather than a data-gap indicator, and the promotion plot further below shows why that matters for this panel.

n_series_panel = 50_000

t_train = 76

horizon = 14

def top_series_by_total_sales(lf: pl.LazyFrame, n: int) -> pl.LazyFrame:

"""Rank the series by total sales over the window and keep the top ``n``."""

return (

lf.group_by("store_id", "product_id")

.agg(pl.col("sale_amount").sum().alias("total_sales"))

.sort("total_sales", descending=True)

.head(n)

)

def keep_top_series(lf: pl.LazyFrame, top_series: pl.DataFrame) -> pl.LazyFrame:

"""Keep only the rows belonging to the selected store-product series."""

return lf.join(

top_series.lazy().select("store_id", "product_id"), on=["store_id", "product_id"]

)

def series_unique_id() -> pl.Expr:

"""Store-product identifier ``store::product`` naming each series."""

return pl.concat_str(["store_id", "product_id"], separator="::").alias("unique_id")

def cleaned_discount_magnitude() -> pl.Expr:

"""Discount depth with the placeholder days encoded as no discount.

``discount == 0`` records are unpriced placeholders (not free giveaways), so

they map to zero magnitude; values above 1 are clipped artifacts.

"""

return (

pl.when(pl.col("discount") > 0)

.then(raw_discount_magnitude().clip(0.0, 1.0))

.otherwise(0.0)

.alias("discount_magnitude")

)

# Rank on the training window only: the modeled panel must be chosen before

# observing the test window, the same fold discipline the per-series scale

# gets in the scaling section below.

in_train_window = pl.col("dt").str.to_date() < (

pl.col("dt").str.to_date().min() + pl.duration(days=t_train)

)

top_series_df = (

data_lf.filter(in_train_window)

.pipe(top_series_by_total_sales, n_series_panel)

.collect(engine="streaming")

)

panel_df = (

data_lf.pipe(keep_top_series, top_series_df)

.with_columns(

pl.col("dt").str.to_date(),

series_unique_id(),

availability_expr,

cleaned_discount_magnitude(),

)

.select(

"dt",

"unique_id",

"store_id",

"sale_amount",

"availability",

"discount_magnitude",

pl.col("activity_flag").cast(pl.Float64),

pl.col("holiday_flag").cast(pl.Float64),

)

.collect(engine="streaming")

.sort("unique_id", "dt")

)

series_ids: list[str] = panel_df["unique_id"].unique().sort().to_list()

n_series = len(series_ids)

dates_series = panel_df["dt"].unique().sort()

dates = dates_series.to_numpy()

panel_df.head()| dt | unique_id | store_id | sale_amount | availability | discount_magnitude | activity_flag | holiday_flag |

|---|---|---|---|---|---|---|---|

| 2024-03-28 | "0::104" | 0 | 0.5 | 0.949572 | 0.0 | 0.0 | 0.0 |

| 2024-03-29 | "0::104" | 0 | 0.9 | 1.0 | 0.024 | 0.0 | 0.0 |

| 2024-03-30 | "0::104" | 0 | 0.7 | 0.917782 | 0.072 | 0.0 | 1.0 |

| 2024-03-31 | "0::104" | 0 | 0.9 | 0.709863 | 0.0 | 0.0 | 1.0 |

| 2024-04-01 | "0::104" | 0 | 0.8 | 0.760477 | 0.024 | 0.0 | 0.0 |

From long panel to a named dataset

The package convention places time at axis \(-2\) and the observation (series) axis last, so the data panel is a dense (time, n_series) matrix. make_pivot builds one such matrix per column, always selecting the columns in series_ids order: that single sorted list defines the series axis everywhere (data, covariates, store index, ArviZ coordinates), so column \(s\) refers to the same store-product pair in every array that follows. The function also validates the result, one row per date, one column per series, and no missing entries, so a silent join or pivot problem fails loudly here instead of corrupting the fit later.

The pivots themselves go straight into an xarray.Dataset with named time and series coordinates, and that dataset is the source of truth for everything downstream: selections read by label (panel_ds["sale_amount"].sel(series="22::267")) instead of positional index bookkeeping, reductions name their axis (.mean("time")), and the plain jax.numpy arrays the model consumes are extracted from it at the model boundary.

def make_pivot(value: str) -> Float[np.ndarray, " duration n_series"]:

"""Build the dense (date x series) matrix of one panel column.

Columns follow ``series_ids`` order so every pivot shares the same series axis.

"""

pivot_df = panel_df.pivot(index="dt", on="unique_id", values=value).sort("dt")

matrix = pivot_df.select(series_ids).to_numpy().astype(np.float64)

if matrix.shape != (len(dates), n_series) or np.isnan(matrix).any():

msg = f"Unexpected pivot for {value!r}: shape {matrix.shape}"

raise ValueError(msg)

return matrix

panel_ds: xr.Dataset = xr.Dataset(

{

name: (("time", "series"), make_pivot(name))

for name in [

"sale_amount",

"availability",

"discount_magnitude",

"activity_flag",

"holiday_flag",

]

},

coords={"time": dates, "series": series_ids},

)

panel_ds<xarray.Dataset> Size: 182MB

Dimensions: (time: 90, series: 50000)

Coordinates:

* time (time) datetime64[s] 720B 2024-03-28 ... 2024-06-25

* series (series) <U8 2MB '0::104' '0::117' ... '9::9' '9::93'

Data variables:

sale_amount (time, series) float64 36MB 0.5 0.3 2.2 ... 2.0 0.1 0.5

availability (time, series) float64 36MB 0.9496 0.0 ... 0.3227 0.7152

discount_magnitude (time, series) float64 36MB 0.0 0.0 0.258 ... 0.0 0.0

activity_flag (time, series) float64 36MB 0.0 0.0 1.0 ... 0.0 0.0 0.0

holiday_flag (time, series) float64 36MB 0.0 0.0 0.0 ... 0.0 0.0 0.0

Per-series scaling

The panel mixes products that sell a unit every ten days with products that sell dozens per day (the printout below spans scales from \(0.10\) to \(18\) sale units per scaled unit). A single set of priors cannot cover both on the raw scale: an initial-level prior like \(\text{Normal}(1, 0.5)\) would be far too tight for one series and far too wide for another. Dividing each series by its own mean daily sales puts every series on a common unit scale, where \(1\) means “an average day for this product”, and one prior vocabulary works across the whole panel (\(\text{Normal}(1, 0.5)\) is then exactly the prior the model places on the scaled initial level). Two details matter:

- The scale is computed on the training window only. Computing it on the full series would leak the held-out level into the model input; the effect is mild on this dataset but catastrophic whenever the test window carries a trend.

- The scale is also the inverse map for evaluation: the model’s draws live on the scaled axis, and we multiply them by

scaleto score and plot in original sale units.

scale: xr.DataArray = panel_ds["sale_amount"].isel(time=slice(None, t_train)).mean("time")

y_scaled: xr.DataArray = panel_ds["sale_amount"] / scale

y_train: Float[Array, " t_train n_series"] = jnp.asarray(

y_scaled.isel(time=slice(None, t_train)).to_numpy(), dtype=jnp.float32

)

y_train_original: Float[Array, " t_train n_series"] = jnp.asarray(

panel_ds["sale_amount"].isel(time=slice(None, t_train)).to_numpy(), dtype=jnp.float32

)

y_test_original: Float[Array, " horizon n_series"] = jnp.asarray(

panel_ds["sale_amount"].isel(time=slice(t_train, None)).to_numpy(), dtype=jnp.float32

)

scale_jax: Float[Array, " n_series"] = jnp.asarray(scale.to_numpy(), dtype=jnp.float32)

print(

f"sale units per scaled unit: min {float(scale.min()):.2f} | "

f"median {float(scale.median()):.2f} | max {float(scale.max()):.2f}"

)sale units per scaled unit: min 0.10 | median 0.65 | max 18.10The store index series_to_store

The covariate effects \(\beta_{c,s}\) are pooled by store: series from the same store share a store-level location and scale. To express that inside the model we need a lookup from the series axis to the store axis, and that is exactly what series_to_store is: an integer vector with one entry per series, series_to_store[s] = m(s), aligned with the same sorted series_ids order as every pivot (both come from sorting by unique_id). We build it with scikit-learn’s LabelEncoder, which consumes the polars column directly: fit_transform maps each store id to its position among the sorted unique ids, and the fitted classes_ are exactly those sorted ids, so the same encoder yields both the integer index the model gathers with and the store coordinate labels the ArviZ export uses below. Inside the model, the advanced indexing b_loc_store[:, series_to_store] gathers the (n_cov, n_stores) store-level parameters into an (n_cov, n_series) array of per-series prior locations, a vectorized dictionary lookup. The jaxtyping annotation records the contract in the code: one integer per series.

The printout below shows the hierarchy is well populated on the full panel: the \(50{,}000\) series spread over \(898\) stores with a median of \(50\) series per store (up to \(164\)), so genuine cross-series pooling is the norm. Singleton stores, where the store-level location is informed by a single series and the hierarchy acts as regularization toward the global hyperpriors rather than as pooling, still exist (the minimum is one series) but are the exception. We revisit this when inspecting the fitted hierarchy.

series_store_df = panel_df.select("unique_id", "store_id").unique().sort("unique_id")

store_encoder = LabelEncoder()

series_to_store: Int[Array, " n_series"] = jnp.asarray(

store_encoder.fit_transform(series_store_df["store_id"]), dtype=jnp.int32

)

store_ids: list[int] = store_encoder.classes_.tolist()

n_stores = len(store_ids)

# The store id of each series as a named lookup table, for label-based gathers on

# the store dimension of the posterior (used in the hierarchy plot below).

series_store_da = xr.DataArray(

series_store_df["store_id"].to_numpy(), dims=["series"], coords={"series": series_ids}

)

series_per_store = np.bincount(np.asarray(series_to_store), minlength=n_stores)

print(f"panel: {n_series} series map to {n_stores} stores")

print(

f"series per store: min {series_per_store.min()} | "

f"median {np.median(series_per_store):.0f} | max {series_per_store.max()}"

)

print(f"train: {t_train} days | test: {horizon} days")panel: 50000 series map to 898 stores

series per store: min 1 | median 50 | max 164

train: 76 days | test: 14 daysA launch indicator

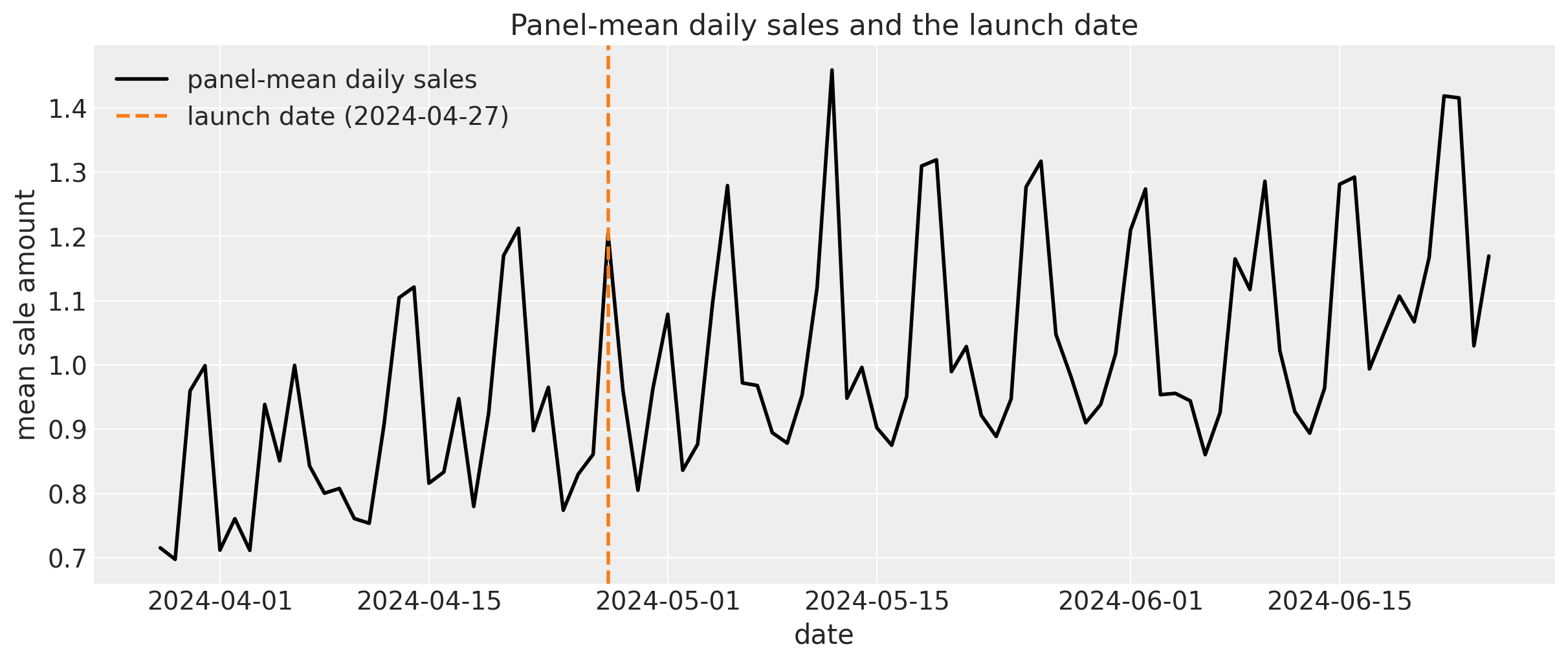

The sales plots below share a striking pattern: the top-volume series all jump to a new level in late April, when this panel’s flagship product ramps up across the assortment. Those series carry a large share of the panel’s volume, so the event matters even though most of the \(50{,}000\) series never see it. That jump is a one-off structural event, not demand dynamics, so we give the model an explicit launch indicator: without a dedicated regressor for the step, any feature that happens to flip around the launch can absorb it and come out with a nonsense coefficient, putting the promotion effects in a tug-of-war with the level. Alternatives that do not work here: relying on the cleaned discount encoding alone (it shrinks the launch-aligned placeholder step, but a shrunken step is still a step a coefficient can latch onto), and per-series change-point detection (fifty thousand extra change points for a one-off event whose date is known).

We therefore fix one shared launch date, \(2024\)-\(04\)-\(27\), inherited from the flagship product’s ramp, which is plainly visible in the top-volume facets below. On the full panel the date is much less prominent than on a top-sellers subset, and the printout below is honest about that: the panel-mean daily sales step up by \(1.40\)x day over day on that date, a move of the same size as the ordinary weekly swings around it, only \(9\%\) of the series place their largest week-over-week jump between \(2024\)-\(04\)-\(27\) and \(2024\)-\(05\)-\(01\), and the modal largest-jump date (\(2024\)-\(06\)-\(05\)) belongs to unrelated series. The indicator is \(0\) before the launch date and \(1\) from that day onward, so over the forecast window it is constantly \(1\): a known future covariate.

window = 7

# rolling labels each window by its last day, so the difference at day t compares

# the week ending at t with the week ending at t - 7; shifting the argmax back by

# window - 1 days labels each series' largest jump by the later week's first day.

rolling_mean = panel_ds["sale_amount"].isel(time=slice(None, t_train)).rolling(time=window).mean()

weekly_jump = rolling_mean - rolling_mean.shift(time=window)

jump_date = weekly_jump.idxmax("time") - np.timedelta64(window - 1, "D")

ramp_date = np.datetime64("2024-04-27")

ramp_x = float(mdates.date2num(ramp_date))

panel_ds["post_ramp"] = (

(panel_ds["time"] >= ramp_date).astype(np.float64).broadcast_like(panel_ds["sale_amount"])

)

panel_mean_sales = panel_ds["sale_amount"].mean("series")

fig, ax = plt.subplots(figsize=(12, 5))

ax.plot(dates, panel_mean_sales, color="black", linewidth=2, label="panel-mean daily sales")

ax.axvline(ramp_x, color="C1", linestyle="--", linewidth=2, label="launch date (2024-04-27)")

ax.legend(loc="upper left")

ax.set(

xlabel="date", ylabel="mean sale amount", title="Panel-mean daily sales and the launch date"

)

modal_dates, modal_counts = np.unique(jump_date.to_numpy(), return_counts=True)

share_modal = float((jump_date == ramp_date).mean())

share_cluster = float(

((jump_date >= ramp_date) & (jump_date <= np.datetime64("2024-05-01"))).mean()

)

step_ratio = float(

panel_mean_sales.sel(time=ramp_date)

/ panel_mean_sales.sel(time=ramp_date - np.timedelta64(1, "D"))

)

print(

f"modal largest-weekly-jump date: {modal_dates[modal_counts.argmax()].astype('datetime64[D]')}"

)

print(f"share of series with their largest weekly jump on 2024-04-27: {share_modal:.2f}")

print(f"share with it between 2024-04-27 and 2024-05-01: {share_cluster:.2f}")

print(f"panel-mean sales step on 2024-04-27: {step_ratio:.2f}x day over day")modal largest-weekly-jump date: 2024-06-05

share of series with their largest weekly jump on 2024-04-27: 0.01

share with it between 2024-04-27 and 2024-05-01: 0.09

panel-mean sales step on 2024-04-27: 1.40x day over day

The model inputs tensor

The model consumes five exogenous inputs per series and day: availability, the three promotion features, and the launch indicator. Rather than flattening them into a wide 2-D matrix (packing and unpacking by hand is exactly the kind of index bookkeeping that fails silently), we stack the five panel variables into a single 3-D DataArray with to_dataarray, whose leading input axis carries the variable names as coordinate labels. The jax.numpy tensor the model consumes is extracted at the boundary and keeps the same layout, with the stack order also named in the jaxtyping hint, availability_discount_activity_holiday_ramp, so it stays readable in every signature that touches the tensor. This layout is fully compatible with the package’s shape convention, which only requires time at axis \(-2\) with batch axes to the left. The train-forecast split stays a pure time slice, and the forecast horizon is still derived from shapes alone: training sees covariates[:, :t_train, :], forecasting the full tensor. The model unpacks the inputs by plain indexing instead of a reshape. to_datatree stores covariates in constant_data as (time, covariate_dim) by default, but accepts this tensor as-is through its covariate_dims argument, which we use in the export section below.

covariate_names = ["discount_magnitude", "activity_flag", "holiday_flag", "post_ramp"]

n_covariates = len(covariate_names)

input_names = ["availability", *covariate_names]

covariates_da: xr.DataArray = panel_ds[input_names].to_dataarray(dim="input")

covariates: Float[Array, " availability_discount_activity_holiday_ramp duration n_series"] = (

jnp.asarray(covariates_da.transpose("input", "time", "series").to_numpy(), dtype=jnp.float32)

)

covariates_train: Float[Array, " availability_discount_activity_holiday_ramp t_train n_series"] = (

covariates[:, :t_train, :]

)

print(f"model inputs: {covariates.shape} | train: {covariates_train.shape}")model inputs: (5, 90, 50000) | train: (5, 76, 50000)Before modeling, let us look at a few of the series we are about to fit: the ten largest by volume and the ten with the most zero-availability days, about twenty facets in all (the prior predictive check further below narrows to a six-series focus subset, three from each ranking).

series_to_plot = 10

n_focus = 3

def top_series(ranking: xr.DataArray, n: int) -> list[str]:

"""Labels of the ``n`` series with the largest value of a per-series ranking."""

return ranking["series"].to_numpy()[np.argsort(-ranking.to_numpy())[:n]].tolist()

total_sales_per_series = panel_ds["sale_amount"].sum("time")

zero_availability_days = (panel_ds["availability"] == 0.0).sum("time")

top_volume_labels = top_series(total_sales_per_series, series_to_plot)

top_stockout_labels = top_series(zero_availability_days, series_to_plot)

plot_labels = list(dict.fromkeys([*top_volume_labels, *top_stockout_labels]))

# The EDA facets and the forecast plot show the full ~20-series set; the prior

# predictive check below uses a 6-series focus set (3 largest by volume,

# 3 heaviest stockouts) to stay readable.

focus_labels = list(dict.fromkeys([*top_volume_labels[:n_focus], *top_stockout_labels[:n_focus]]))

split_x = float(mdates.date2num(dates[t_train]))

# plot_lm concatenates x with the float predictions internally, so the faceted

# plots below use matplotlib date numbers plus a date formatter on each axis.

dates_num = np.asarray(mdates.date2num(dates))

fig, axes = plt.subplots(

nrows=len(plot_labels),

figsize=(12, 2.2 * len(plot_labels)),

sharex=True,

layout="constrained",

)

for ax, label in zip(axes, plot_labels, strict=True):

(sales_line,) = ax.plot(

dates, panel_ds["sale_amount"].sel(series=label), color="black", linewidth=2, label="sales"

)

split_line = ax.axvline(

split_x, color="C3", linestyle="--", linewidth=1, label="train-test split"

)

ramp_line = ax.axvline(ramp_x, color="C1", linestyle=":", linewidth=1.5, label="launch date")

ax.set(title=label, ylabel="sale amount")

ax_twin = ax.twinx()

(availability_line,) = ax_twin.plot(

dates,

panel_ds["availability"].sel(series=label),

color="red",

linewidth=1.5,

label="availability",

)

ax_twin.grid(False)

ax_twin.yaxis.set_major_formatter(mtick.PercentFormatter(xmax=1, decimals=0))

ax_twin.set(ylabel="availability", ylim=(0, 1.05))

axes[0].legend(

handles=[sales_line, split_line, ramp_line, availability_line], loc="upper left", fontsize=10

)

fig.supxlabel("date")

fig.suptitle("Sales and sales-weighted availability", fontsize=18, fontweight="bold");

The stockout-heavy series make the modeling problem vivid: sales collapse toward zero when availability drops, but not exactly to zero, and they snap back as soon as stock returns. The two rankings select two different products. Every top-volume facet is the flagship product (267) in a different store, and the dotted launch line runs right through their shared jump: each of those series starts selling in earnest or doubles its level at \(2024\)-\(04\)-\(27\). The stockout ranking is instead dominated by a low-volume product (757), whose facets show long fully-out-of-stock stretches, and several of those series only start selling weeks after the launch date.

The same view for the promotion covariates completes the picture: the discount magnitude on the right axis, with promotion-activity and holiday days shaded in the background.

fig, axes = plt.subplots(

nrows=len(plot_labels),

figsize=(12, 2.2 * len(plot_labels)),

sharex=True,

layout="constrained",

)

discount_max = float(panel_ds["discount_magnitude"].max())

for ax, label in zip(axes, plot_labels, strict=True):

(sales_line,) = ax.plot(

dates, panel_ds["sale_amount"].sel(series=label), color="black", linewidth=2, label="sales"

)

split_line = ax.axvline(

split_x, color="C3", linestyle="--", linewidth=1, label="train-test split"

)

activity_span = ax.fill_between(

dates,

0,

1,

where=(panel_ds["activity_flag"].sel(series=label) > 0.5).to_numpy(),

transform=ax.get_xaxis_transform(),

color="C0",

alpha=0.25,

linewidth=0,

label="promotion activity day",

)

holiday_span = ax.fill_between(

dates,

0,

1,

where=(panel_ds["holiday_flag"].sel(series=label) > 0.5).to_numpy(),

transform=ax.get_xaxis_transform(),

color="C4",

alpha=0.35,

linewidth=0,

label="holiday",

)

ax.set(title=label, ylabel="sale amount")

ax_twin = ax.twinx()

(discount_line,) = ax_twin.plot(

dates,

panel_ds["discount_magnitude"].sel(series=label),

color="C1",

alpha=0.8,

linewidth=1,

label="discount magnitude",

)

ax_twin.grid(False)

ax_twin.yaxis.set_major_formatter(mtick.PercentFormatter(xmax=1, decimals=0))

ax_twin.set(ylabel="discount", ylim=(0, 1.1 * discount_max))

axes[0].legend(

handles=[sales_line, split_line, discount_line, activity_span, holiday_span],

loc="upper center",

bbox_to_anchor=(0.5, 1.45),

ncol=5,

fontsize=12,

)

fig.supxlabel("date")

fig.suptitle("Sales and promotion covariates", fontsize=18, fontweight="bold");

# The facet plot shows the top series only; these panel-wide shares back the

# feature-quality discussion below.

panel_covariate_shares = (

data_lf.pipe(keep_top_series, top_series_df)

.with_columns(cleaned_discount_magnitude())

.group_by("store_id", "product_id")

.agg(

(pl.col("activity_flag") > 0).any().alias("any_activity"),

(pl.col("discount_magnitude") > 0).any().alias("any_discount"),

(pl.col("discount") == 0).mean().alias("placeholder_share"),

)

.select(

pl.col("any_activity").mean(),

pl.col("any_discount").mean(),

pl.col("placeholder_share").mean(),

)

.collect(engine="streaming")

)

promo_share, discount_share, placeholder_share = panel_covariate_shares.row(0)

print(f"panel series with at least one active-promotion day: {promo_share:.1%}")

print(f"panel series with at least one real discount day: {discount_share:.1%}")

print(f"placeholder discount = 0 share of the panel's day-rows: {placeholder_share:.1%}")panel series with at least one active-promotion day: 83.8%

panel series with at least one real discount day: 96.7%

placeholder discount = 0 share of the panel's day-rows: 0.4%Two patterns jump out. The holiday flag repeats weekly (weekends plus a solid block around the May Day week), and several series show local sales spikes on those shaded days. Promotion activity and priced discounts split cleanly across the two rankings: the ten top-volume rows show neither (the flagship launch product is simply never promoted), while the stockout-heavy rows carry long promotion-activity spans and real discounts, in line with the panel at large, where \(84\%\) of the series have at least one active-promotion day and \(97\%\) at least one real discount day. The flat discount line on the flagship rows is also the placeholder cleanup at work: for those series the raw discount column is zero on most days (the placeholder flagged in the EDA at \(0.4\%\) of all day-rows is concentrated in exactly this product), so the cleaned magnitude sits at an honest zero instead of reading as a \(100\%\) discount. This heterogeneity in feature quality is one more argument for pooling the covariate effects by store rather than fitting one global discount effect: where the feature is quiet the coefficient is weakly identified and shrinks toward its store-level prior, and where the feature is informative it can act.

Model specification

The model is a panel state space model on the scaled sales, with five components per series \(s\):

- a random-walk local level for slow demand shifts,

- a damped AR(1) trend slope that carries the recent drift into the forecast window,

- a zero-sum weekly seasonal profile,

- promotion, calendar, and launch effects pooled hierarchically by store,

- a multiplicative availability factor with a learned floor, which also scales the observation noise.

\[ \begin{align*} y_{t,s} &\sim \text{Normal}\left(f_{t,s} \, \mu_{t,s},\; f_{t,s} \left(\sigma_s + \lambda_s \, \text{softplus}(\ell_{t,s})\right) + \sigma_0\right) \\ \mu_{t,s} &= \ell_{t,s} + \gamma_{d(t),s} + \sum_{c=1}^{4} \beta_{c,s} \, x_{c,t,s} \\ \ell_{t,s} &= \ell_{0,s} + \sum_{u \le t} \left(\varepsilon_{u,s} + \delta_{u,s}\right), \qquad \varepsilon_{u,s} \sim \text{Normal}(0, \tau_s) \\ \delta_{u,s} &= \phi^{\text{trend}}_s \, \delta_{u-1,s} + \eta_{u,s}, \qquad \eta_{u,s} \sim \text{Normal}\left(0, \tau^{\text{trend}}_s\right), \quad \delta_{0,s} = 0 \\ f_{t,s} &= \phi_s + (1 - \phi_s) \, \frac{1 - e^{-b_s a_{t,s}}}{1 - e^{-b_s}} \\ \beta_{c,s} &\sim \text{Normal}\left(\mu^{\text{store}}_{c,\,m(s)},\; \sigma^{\text{store}}_{c,\,m(s)}\right) \end{align*} \]

where \(d(t)\) is the day of week, \(m(s)\) the store of series \(s\), \(a_{t,s}\) the sales-weighted availability, \(x_{c,t,s}\) the four regression features (discount magnitude, promotion activity, holiday, and the launch indicator), \(\lambda_s\) the loading of the level-dependent noise component, and \(\sigma_0 = 0.02\) a small constant basal noise; the last two are discussed with the noise scale below. The remaining priors, all on the scaled axis where \(1\) is an average day for the series:

\[ \begin{align*} \ell_{0,s} &\sim \text{Normal}(1, 0.5), & \tau_s &\sim \text{LogNormal}(-3, 1) \\ \phi^{\text{trend}}_s &\sim \text{Beta}(8, 2), & \tau^{\text{trend}}_s &\sim \text{LogNormal}(-4, 1) \\ \gamma_{\cdot,s} &\sim \text{ZeroSumNormal}(\sigma_\gamma, 7), & \sigma_\gamma &\sim \text{HalfNormal}(0.2) \\ \mu^{\text{store}}_{c,m} &\sim \text{Normal}(0, 0.5), & \sigma^{\text{store}}_{c,m} &\sim \text{HalfNormal}(0.3) \\ \phi_s &\sim \text{Beta}(2, 18), & b_s &\sim \text{LogNormal}(1, 0.5) \\ \sigma_s &\sim \text{HalfNormal}(0.5), & \lambda_s &\sim \text{HalfNormal}(0.2) \end{align*} \]

The random-walk drift \(\varepsilon\) and the coefficients \(\beta\) use LocScaleReparam with learned centeredness parameters (each a global \(\text{Uniform}(0, 1)\) latent), as in the other hierarchical examples. The sections below motivate the trend, dynamics, and availability-factor priors in detail.

The damped trend

We give each series a damped AR(1) slope on top of the random-walk level because a \(14\)-day forecast needs momentum: this panel keeps drifting upward through the test window, and only a trend state can carry that drift past the last observed day. In the state-space scan the forecast is seeded by the final in-sample slope, which then decays geometrically at rate \(\phi^{\text{trend}}_s < 1\) while its uncertainty keeps growing, so the forecast inherits the current momentum without betting on it indefinitely. The interval-diagnostics section below quantifies what this buys on the holdout.

Alternatives that do not work here:

- A pure random-walk level with no slope, meaning the forecast freezes at the last fitted level. On a drifting panel like this one the interval misses then concentrate above the bands and grow with the horizon while the forecast fan barely widens, exactly the miscalibration signature the interval diagnostics below are built to detect.

- An undamped slope (an integrated random walk), meaning the last local trend is extrapolated as a straight line indefinitely. Fresh-retail momentum is short-lived (a promotion tail, a post-launch settling), so the straight line overshoots at precisely the long horizons where intervals are most fragile; the damping relaxes the trend toward zero within the horizon instead.

The availability factor

The factor \(f_{t,s}\) deserves a close look, because its three ingredients each fix a concrete failure mode:

- The floor \(\phi_s \in (0, 1)\). At zero recorded availability the factor equals \(\phi_s\), not zero, so the \(15\%\) of flagged stockout days with positive sales are explained by a small expected sale instead of blowing up the likelihood. The prior \(\phi_s \sim \text{Beta}(2, 18)\) (mean \(0.1\)) is informed by the empirical floor of about \(0.04\) measured above, while staying wide enough for series with sloppier labels.

- The saturating link \(1 - e^{-b_s a}\). This is the classic random-encounter (reach) curve: if purchase attempts arrive through the day as a Poisson process with intensity \(b_s\), and a share \(a\) of the (sales-weighted) selling time is in stock, the probability that at least one attempt lands while the product is on the shelf is exactly \(1 - e^{-b_s a}\). It matches the concave shape of the empirical curve, and compared to alternatives such as \(\tanh\) it is cheaper (one exponential), has a smooth monotone gradient in \(b_s\), and gives \(b_s\) a direct interpretation as purchase-opportunity intensity.

- The normalization by \(1 - e^{-b_s}\). Without it, the factor at full availability is \(1 - e^{-b_s} < 1\), and the model can trade the factor’s overall scale against the level \(\ell_{t,s}\) (multiply one, divide the other), leaving both non-identified. Anchoring \(f_{t,s} = 1\) at \(a = 1\) removes that degeneracy: the level is the demand at full availability, \(\phi_s\) is exactly the share of demand still sold on a fully flagged-out day, and \(b_s\) only controls the curvature. Numerically we compute the ratio with

expm1, which avoids the catastrophic cancellation in \(1 - e^{-b_s}\) for small \(b_s\), where the naive expression degrades toward \(0/0\).

fig, ax = plt.subplots()

pz.Beta(2, 18).plot_pdf(color="C0", ax=ax)

ax.axvline(

empirical_floor,

color="C3",

linestyle="--",

label=f"empirical floor ({empirical_floor:.2f})",

)

ax.legend(loc="upper right")

ax.set(xlabel=r"floor $\phi_s$", ylabel="density", title="Floor prior");

def availability_factor(

availability: Float[np.ndarray | Array, " ..."] | float,

b_avail: Float[np.ndarray | Array, " ..."] | float,

floor: Float[np.ndarray | Array, " ..."] | float,

) -> Float[np.ndarray | Array, " ..."]:

"""Floored, normalized saturating availability factor.

The model-specification curve

``floor + (1 - floor) * expm1(-b_avail * availability) / expm1(-b_avail)``:

``floor`` at zero availability, exactly ``1`` at full availability, with the

curvature set by ``b_avail``. Defined once, at first use, and shared by the

illustrative curves here, the model, and the prior/posterior diagnostic

cells below, so the plotted curves can never drift from what the model

computes. Inputs broadcast together per NumPy rules. NumPy and scalar

inputs are accepted (``xarray.apply_ufunc`` passes NumPy arrays in the

posterior diagnostic below) and computed with ``jax.numpy``.

Parameters

----------

availability

Sales-weighted availability in ``[0, 1]``.

b_avail

Saturation rate (the purchase-opportunity intensity).

floor

The factor at zero availability, in ``(0, 1)``.

Returns

-------

Array

The multiplicative availability factor.

"""

saturation = jnp.expm1(-b_avail * availability) / jnp.expm1(-b_avail)

return floor + (1.0 - floor) * saturation

a_grid = jnp.linspace(0, 1, 200) # availability from 0 to 1

b_vals = [0.5, 1.5, 5.0, 12.0] # some example b_s values

fig, ax = plt.subplots()

for b in b_vals:

f = availability_factor(a_grid, b, 0.0)

ax.plot(a_grid, f, label=f"$b_s={b}$")

fig.text(0.7, 0.42, r"$\frac{1 - e^{-b_s a_{t,s}}}{1 - e^{-b_s}}$", fontsize=36)

ax.legend(loc="lower right")

ax.set(

title="Saturating availability factor vs $a_{t,s}$",

xlabel="Availability $a_{t,s}$",

ylabel="Availability factor",

);

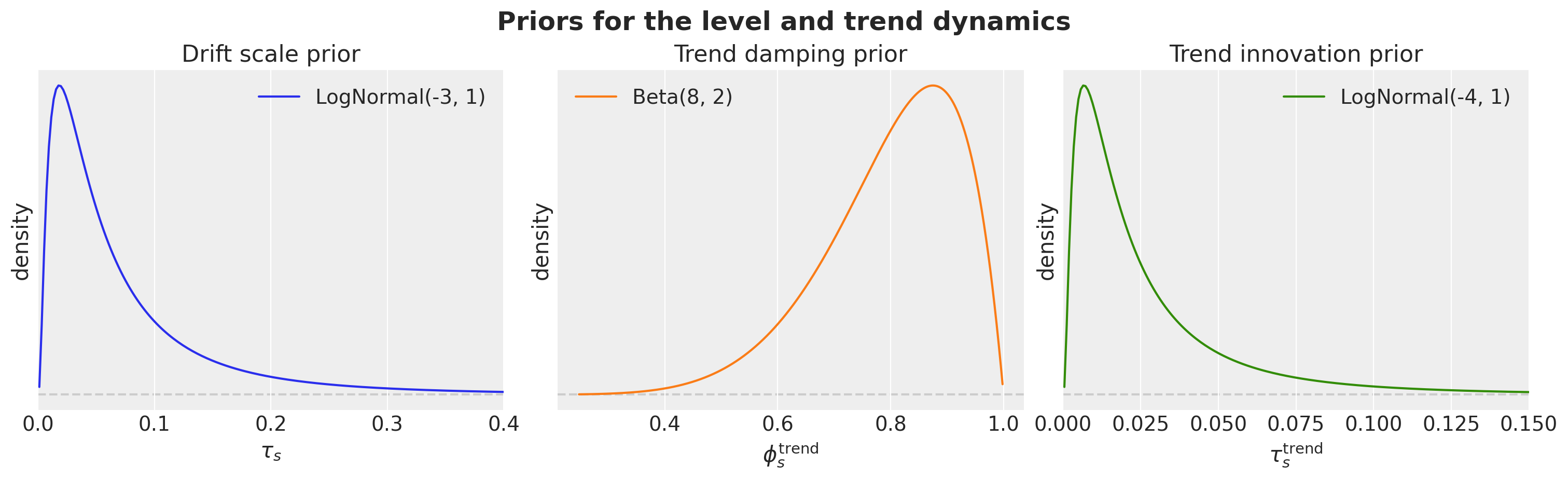

Priors for the level and trend dynamics

Three priors govern how much the level is allowed to move, and they are worth choosing deliberately. All live on the scaled axis, where \(1\) is an average day for the series:

- \(\tau_s \sim \text{LogNormal}(-3, 1)\), the random-walk drift scale: median \(\approx 0.05\), so a typical series may shift its level by around \(5\%\) of an average day per step, with the long right tail leaving room for jumpier series.

- \(\phi^{\text{trend}}_s \sim \text{Beta}(8, 2)\), the trend damping: mean \(0.8\), so a slope shock loses about half its size in three days (\(0.8^3 \approx 0.51\)) and the extrapolated trend flattens within the \(14\)-day horizon instead of running away.

- \(\tau^{\text{trend}}_s \sim \text{LogNormal}(-4, 1)\), the slope innovation scale: median \(\approx 0.018\), deliberately well below the drift and observation scales, so the slope only accumulates persistent day-over-day signals and cannot chase daily noise.

prior_panels = [

(pz.LogNormal(-3, 1), "C0", "LogNormal(-3, 1)", "Drift scale prior", r"$\tau_s$", (0.0, 0.4)),

(pz.Beta(8, 2), "C1", "Beta(8, 2)", "Trend damping prior", r"$\phi^{\mathrm{trend}}_s$", None),

(

pz.LogNormal(-4, 1),

"C2",

"LogNormal(-4, 1)",

"Trend innovation prior",

r"$\tau^{\mathrm{trend}}_s$",

(0.0, 0.15),

),

]

fig, axes = plt.subplots(ncols=3, figsize=(15, 4.5), layout="constrained")

for ax, (prior, color, name, title, xlabel, xlim) in zip(axes, prior_panels, strict=True):

prior.plot_pdf(color=color, legend=None, ax=ax)

pdf_line = next(line for line in ax.lines if line.get_color() == color)

pdf_line.set_label(name)

ax.legend()

ax.set(xlabel=xlabel, ylabel="density", title=title)

if xlim is not None:

ax.set_xlim(*xlim)

fig.suptitle("Priors for the level and trend dynamics", fontsize=18, fontweight="bold");

Finally, the noise scale is \(f_{t,s} \left(\sigma_s + \lambda_s \, \text{softplus}(\ell_{t,s})\right) + \sigma_0\). It has three parts: a per-series base scale \(\sigma_s\), a level-dependent component \(\lambda_s \, \text{softplus}(\ell_{t,s})\), sampled as noise_loading in the code (busier days are noisier in absolute terms, and its coverage payoff is quantified in the evaluation section), and the availability factor \(f_{t,s}\) shrinking the spread on stockout days, where sales are pinned near zero. The remaining piece is a small constant basal term \(\sigma_0 = 0.02\) on the scaled axis, which keeps the scale bounded away from zero. Three design questions hide in this one constant:

- Why not a learned basal term? Many series sell exactly zero on their stockout days, where the mean is also pinned near zero. A Normal density at a perfectly fit point grows without bound as its scale shrinks, so the ELBO rewards collapsing the total noise scale at those observations; with a learned basal term the collapse runs away and the optimization hits

NaNmid-run (on the \(1{,}000\)-series panel of the companion CPU notebook the first non-finite ELBO appears around step \(6{,}000\)). A constant cannot collapse. - Why not a tiny epsilon like \(10^{-6}\)? The constant is not there to avoid division by zero; it must remove the reward for collapse. With \(\sigma_0 = 10^{-6}\) the density at an exactly fit zero can still contribute \(\log\left(1 / (\sigma_0 \sqrt{2\pi})\right) \approx 12.9\) per observation, and on the \(1{,}000\)-series variant such a fit banks roughly a thousand nats of ELBO from these spikes while every predictive metric stays identical to the \(0.02\) fit: the “improvement” is purely the degenerate optimum being exploited, and stability is then at the mercy of the learning-rate schedule (the learned-term variant diverged through exactly this mechanism).

- Why \(0.02\) specifically? It sits at the data’s resolution: one physical sale unit is at least \(0.06\) on the per-series scaled axis (and up to \(10\) for the smallest series in this full panel), so a basal noise of \(0.02\) is below measurement granularity and cannot distort any interval the data could support. On the \(1{,}000\)-series companion notebook, fits with \(\sigma_0 \in \{0.01, 0.02, 0.05\}\) give the same CRPS and coverage to within noise.

class FreshRetailModel(ForecastingModel):

"""Damped-trend hierarchical panel model with a floored availability factor.

Parameters

----------

series_to_store

Integer index mapping each series to its store, shape ``(n_series,)``.

n_stores

Number of distinct stores in the panel.

n_series

Number of store-product series (the trailing observation axis).

n_cov

Number of regression features (excluding availability).

"""

def __init__(

self,

series_to_store: Int[Array, " n_series"],

n_stores: int,

n_series: int,

n_cov: int,

) -> None:

super().__init__()

self.series_to_store = series_to_store

self.n_stores = n_stores

self.n_series = n_series

self.n_cov = n_cov

def model(

self,

zero_data: Float[Array, " duration n_series"] | None,

covariates: Float[Array, " availability_discount_activity_holiday_ramp duration n_series"],

) -> None:

"""Sample the joint model (the package calls this for training and forecasting)."""

duration = covariates.shape[-2]

# The inputs tensor keeps time at axis -2 (the package-wide convention) with

# the stacked inputs as a leading batch axis, named explicitly in the

# signature: availability first, then the regression features, already

# shaped so that `features * b[:, None, :]` broadcasts against the

# (n_cov, n_series) coefficients. The `assert isinstance` lines are

# jaxtyping's runtime shape guards: they share the dimension memo with the

# signature (so `duration` and `n_series` are already bound by

# `covariates`); plain annotated assignments would NOT be checked at runtime.

availability = covariates[0]

assert isinstance(availability, Float[Array, " duration n_series"]) # ty: ignore[invalid-argument-type]

features = covariates[1:]

assert isinstance(features, Float[Array, " n_cov duration n_series"]) # ty: ignore[invalid-argument-type]

# Global hyperpriors. The seasonal scale must be a scalar because

# ZeroSumNormal cannot broadcast a per-series scale over the plate.

centered_drift = numpyro.sample("centered_drift", dist.Uniform(0.0, 1.0))

centered_b = numpyro.sample("centered_b", dist.Uniform(0.0, 1.0))

seasonal_scale = numpyro.sample("seasonal_scale", dist.HalfNormal(0.2))

with numpyro.plate("store", self.n_stores, dim=-1):

with numpyro.plate("covariate", self.n_cov, dim=-2):

b_loc_store = cast("Array", numpyro.sample("b_loc_store", dist.Normal(0.0, 0.5)))

b_scale_store = cast(

"Array", numpyro.sample("b_scale_store", dist.HalfNormal(0.3))

)

with numpyro.plate("series", self.n_series, dim=-1):

drift_scale = numpyro.sample("drift_scale", dist.LogNormal(-3.0, 1.0))

phi_trend = cast("Array", numpyro.sample("phi_trend", dist.Beta(8.0, 2.0)))

tau_trend = cast("Array", numpyro.sample("tau_trend", dist.LogNormal(-4.0, 1.0)))

init_level = cast("Array", numpyro.sample("init_level", dist.Normal(1.0, 0.5)))

b_avail = cast("Array", numpyro.sample("b_avail", dist.LogNormal(1.0, 0.5)))

floor = cast("Array", numpyro.sample("floor", dist.Beta(2.0, 18.0)))

sigma = cast("Array", numpyro.sample("sigma", dist.HalfNormal(0.5)))

noise_loading = cast("Array", numpyro.sample("noise_loading", dist.HalfNormal(0.2)))

seasonal = cast(

"Array",

numpyro.sample("seasonal", dist.ZeroSumNormal(seasonal_scale, event_shape=(7,))),

)

with numpyro.plate("covariate", self.n_cov, dim=-2):

with handlers.reparam(config={"b": LocScaleReparam(centered=centered_b)}):

b = cast(

"Array",

numpyro.sample(

"b",

dist.Normal(

b_loc_store[:, self.series_to_store],

b_scale_store[:, self.series_to_store],

),

),

)

# time_series opens its own time plate at dim=-2, so the covariate

# plate above must already be closed here.

drift = self.time_series(

"drift",

lambda: dist.Normal(0.0, drift_scale),

reparam=LocScaleReparam(centered=centered_drift),

)

# The damped AR(1) slope is a Markov latent: markov_time_series scans over

# time (and must be called outside the series plate; the per-series

# parameters enter through the closure), seeds the forecast scan with the

# final in-sample slope, and returns the latent in the package layout

# (duration, n_series).

def slope_transition(

carry: Array, _: Array | None

) -> tuple[dist.Distribution, Callable[[Array], Array]]:

return dist.Normal(phi_trend * carry, tau_trend), lambda value: value

slope = self.markov_time_series("slope", jnp.zeros(self.n_series), slope_transition)

level = init_level + jnp.cumsum(drift, axis=-2) + jnp.cumsum(slope, axis=-2)

seasonal_rep = periodic_repeat(seasonal.T, duration, axis=-2)

covariates_contribution = (features * b[:, None, :]).sum(axis=0)

factor = cast("Array", availability_factor(availability, b_avail, floor))

mu = factor * (level + seasonal_rep + covariates_contribution)

# The constant basal noise bounds the likelihood at exact-zero sales: a

# learned basal term collapses there and NaNs the optimization, and a tiny

# epsilon (e.g. 1e-6) leaves that degenerate optimum in play; 0.02 sits just

# below one physical sale unit on the scaled axis (see the markdown above).

sigma_t = factor * (sigma + noise_loading * jax.nn.softplus(level)) + 0.02

self.predict_glm(lambda m: dist.Normal(m, sigma_t), mu)

model = FreshRetailModel(

series_to_store=series_to_store,

n_stores=n_stores,

n_series=n_series,

n_cov=n_covariates,

)The model-structure rendering is commented out in this GPU run; see the companion CPU notebook for the numpyro.render_model graph.

numpyro.render_model(

model,

model_args=(covariates_train, y_train),

render_distributions=True,

)

Prior predictive checks

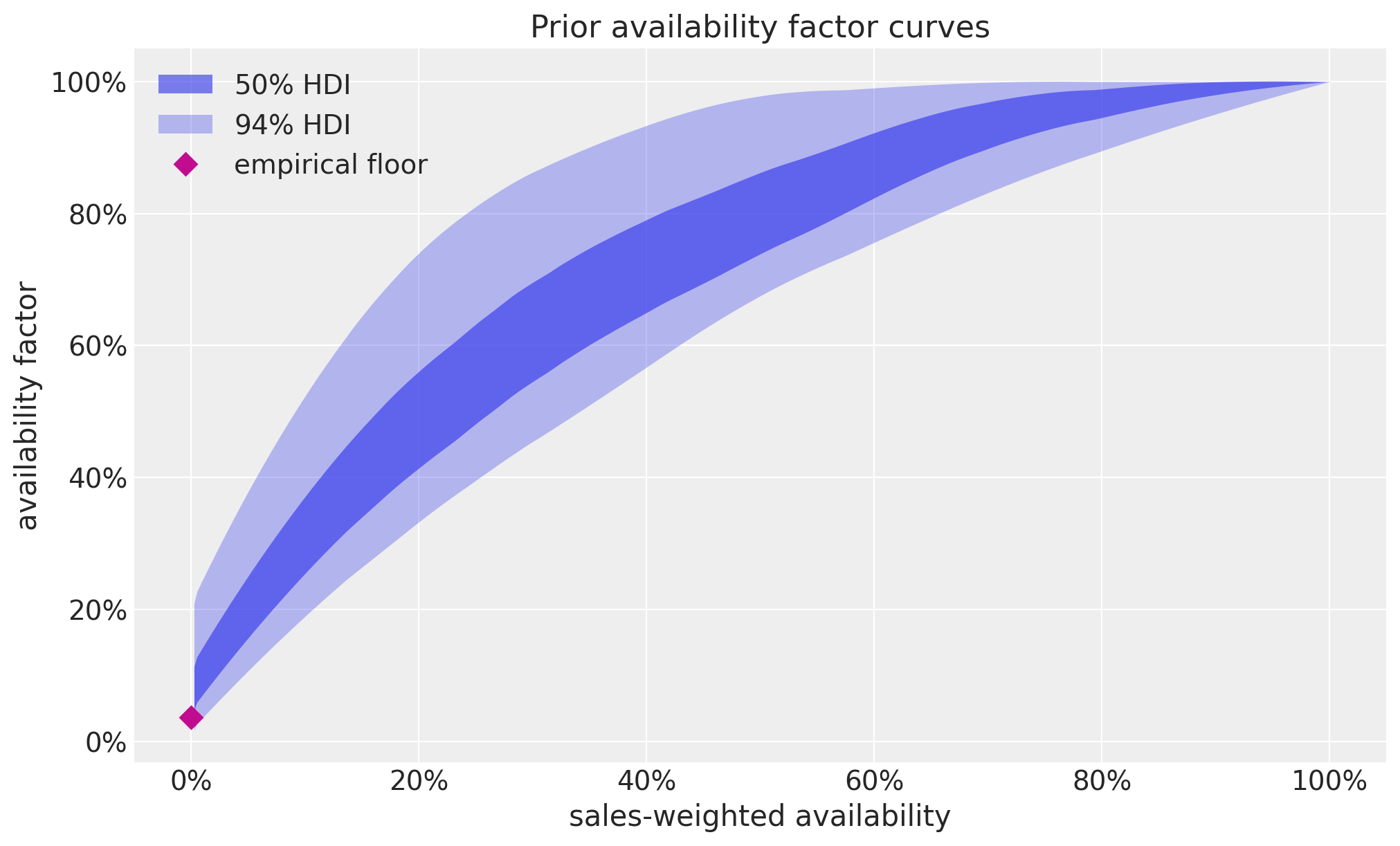

First the factor itself: the priors on \(\phi_s\) and \(b_s\) should cover both gentle and sharp saturation, with the floor concentrated near the empirical value but not glued to it.

The plots in this and the following sections lean on the package helper predictions_to_datatree: it packs raw prediction-draw arrays (possibly rescaled, clipped, or subset) into the DataTree layout that az.plot_lm needs for per-series faceting, with the independent variable broadcast per series in constant_data. It complements rather than duplicates to_datatree, which is fit-centric (it draws its own predictive from a fit and stores covariates, not a faceting grid). On our side of that boundary, every predictive ensemble gets wrapped in a DataArray with named time and series coordinates (the small draws_to_da helper below), so subsetting for a plot is a label-based .sel(series=...) rather than a positional index expression.

Every banded plot shares two styling conventions, set once here. The hdi_label helper formats the legend entries from the probability itself (the \% escape is what mathtext requires), and each az.plot_lm call maps the band transparency explicitly onto the prob dimension via aes={"alpha": ["prob"]} with the hdi_alphas values below, so the narrower \(50\%\) band sits more opaque on top of the lighter \(94\%\) band in every figure.

def hdi_label(prob: float, prefix: str = "") -> str:

r"""Legend label for an HDI band, e.g. ``$94\%$ HDI``."""

percent = f"{prob:.0%}".replace("%", r"\%")

return f"{prefix}${percent}$ HDI"

hdi_probs = (0.5, 0.94)

hdi_alphas = [0.6, 0.3]availability_grid = np.linspace(0.0, 1.0, 101)

rng_key, key_floor, key_b = random.split(rng_key, 3)

floor_prior = dist.Beta(2.0, 18.0).sample(key_floor, (500,))

b_prior = dist.LogNormal(1.0, 0.5).sample(key_b, (500,))

grid_jax = jnp.asarray(availability_grid, dtype=jnp.float32)

factor_prior = availability_factor(grid_jax, b_prior[:, None], floor_prior[:, None])

pc = az.plot_lm(

predictions_to_datatree(

np.asarray(factor_prior)[:, :, None],

availability_grid,

["prior factor"],

group="prior_predictive",

),

y="obs",

x="t",

plot_dim="time",

group="prior_predictive",

ci_kind="hdi",

ci_prob=hdi_probs,

smooth=True,

visuals={

"ci_band": {"color": "C0"},

"observed_scatter": False,

"pe_line": False,

"xlabel": False,

"ylabel": False,

},

aes={"alpha": ["prob"]},

alpha=hdi_alphas,

figure_kwargs={"figsize": (10, 6)},

)

ax = pc.get_target("t", {"series": "prior factor"})

ax.plot(0.0, empirical_floor, "D", color="C3", markersize=8, label="empirical floor")

bands = pc.viz["ci_band"]["t"].sel(series="prior factor")

for prob in (0.94, 0.5):

bands.sel(prob=prob).item().set_label(hdi_label(prob))

ax.legend(loc="upper left")

ax.xaxis.set_major_formatter(mtick.PercentFormatter(xmax=1, decimals=0))

ax.yaxis.set_major_formatter(mtick.PercentFormatter(xmax=1, decimals=0))

ax.set(

xlabel="sales-weighted availability",

ylabel="availability factor",

title="Prior availability factor curves",

);

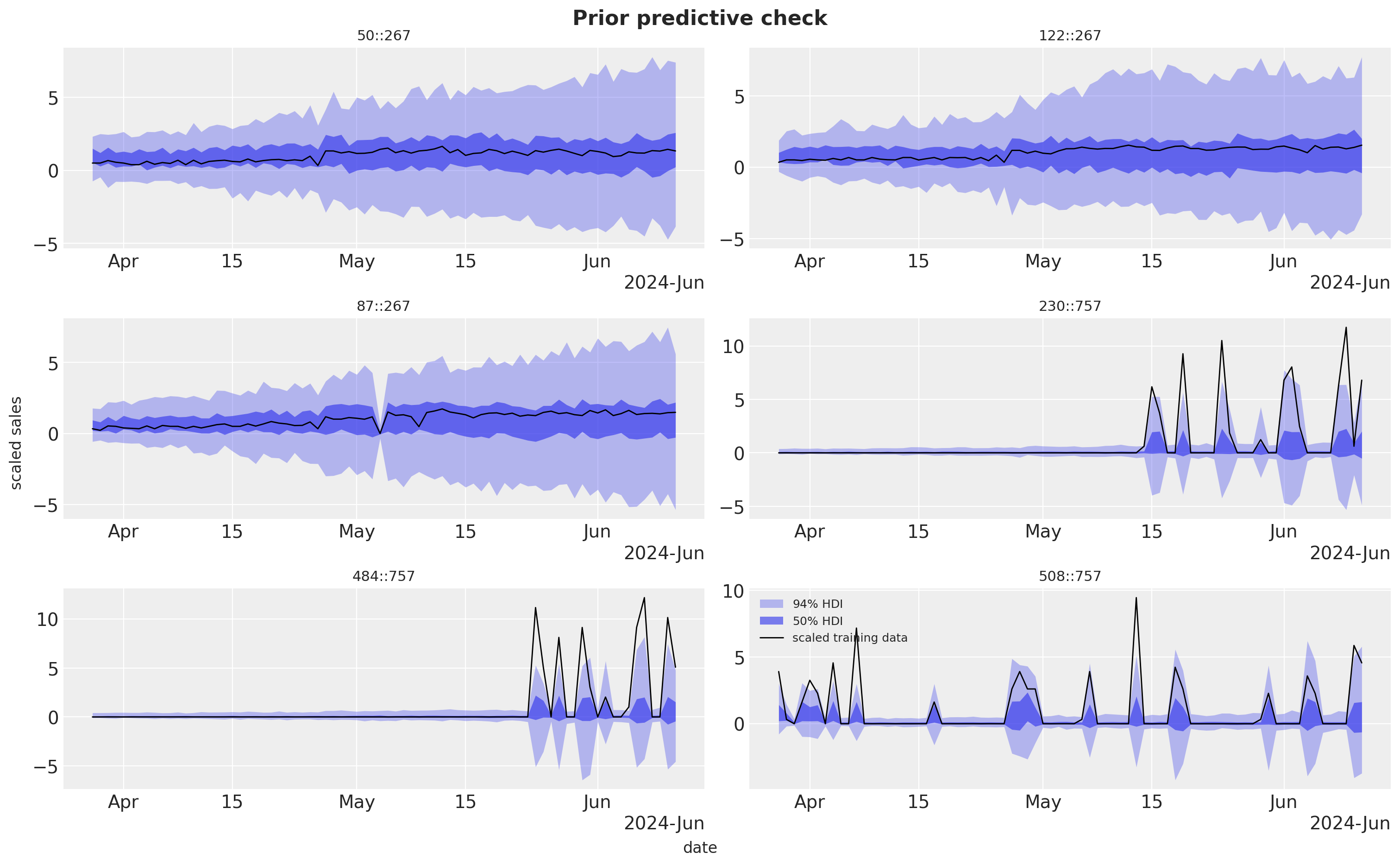

Next the full prior predictive on the training window for our six focus series, with the scaled observations overlaid. We want wide but sane bands on the unit scale of the normalized data. The bands also dip below zero: a Normal likelihood on the scaled axis pays for its simplicity with prior (and posterior) mass on negative sales, a compromise we accept here and revisit in the next steps with a strictly positive observation model.

def draws_to_da(

draws: Float[np.ndarray | Array, " sample time n_series"],

time_values: np.ndarray,

) -> xr.DataArray:

"""Wrap prediction draws in a DataArray with named time and series coordinates."""

return xr.DataArray(

np.asarray(draws),

dims=["sample", "time", "series"],

coords={"time": time_values, "series": series_ids},

)

rng_key, key_prior = random.split(rng_key)

prior_obs = Predictive(model, num_samples=500, return_sites=["obs"])(key_prior, covariates_train)[

"obs"

]

prior_obs_da = draws_to_da(prior_obs, dates[:t_train])

pc = az.plot_lm(

predictions_to_datatree(

prior_obs_da.sel(series=focus_labels).to_numpy(),

dates_num[:t_train],

focus_labels,

group="prior_predictive",

),

y="obs",

x="t",

plot_dim="time",

group="prior_predictive",

ci_kind="hdi",

ci_prob=hdi_probs,

smooth=False,

col_wrap=2,

visuals={

"ci_band": {"color": "C0"},

"observed_scatter": False,

"pe_line": False,

"xlabel": False,

"ylabel": False,

},

aes={"alpha": ["prob"]},

alpha=hdi_alphas,

figure_kwargs={"figsize": (15, 9)},

)

truth_da = (

y_scaled.isel(time=slice(None, t_train))

.sel(series=focus_labels)

.assign_coords(time=dates_num[:t_train])

.rename("t")

)

x_da = xr.DataArray(dates_num[:t_train], dims=["time"], coords={"time": dates_num[:t_train]})

pc.map(

az.visuals.line_xy,

"truth",

data=truth_da,

x=x_da,

ignore_aes=pc.aes_set,

color="black",

lw=1,

)

for label in focus_labels:

ax = pc.get_target("t", {"series": label})

ax.set_title(label, fontsize=11)

locator = mdates.AutoDateLocator()

ax.xaxis.set_major_locator(locator)

ax.xaxis.set_major_formatter(mdates.ConciseDateFormatter(locator))

ax0 = pc.get_target("t", {"series": focus_labels[-1]})

bands = pc.viz["ci_band"]["t"].sel(series=focus_labels[-1])

band_handles = []

for prob in (0.94, 0.5):

band = bands.sel(prob=prob).item()

band.set_label(hdi_label(prob))

band_handles.append(band)

truth_line = pc.viz["truth"]["t"].sel(series=focus_labels[-1]).item()

truth_line.set_label("scaled training data")

ax0.legend(handles=[*band_handles, truth_line], loc="upper left", fontsize=9)

fig = pc.viz["figure"].item()

fig.supxlabel("date")

fig.supylabel("scaled sales")

fig.suptitle("Prior predictive check", fontsize=16, fontweight="bold", y=1.02)

# The raw prior draws are a multi-GB device buffer at panel scale; the plot

# above holds a NumPy copy, so release the device memory here.

del prior_obs

Inference with SVI

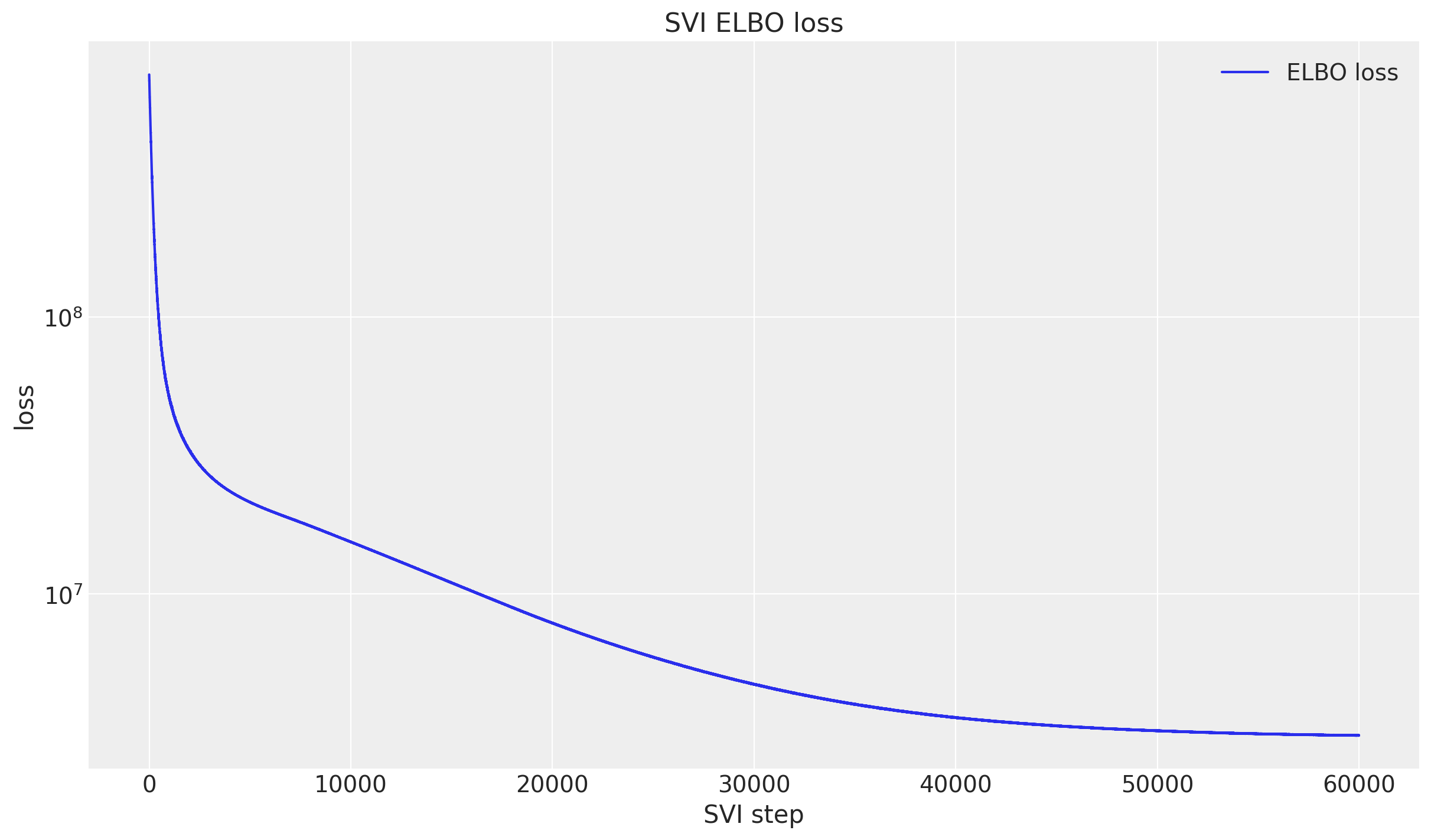

We fit with fit_svi and its default AutoNormal guide. Instead of a fixed learning rate we pass a custom optax optimizer, the one-cycle Adam schedule chained with reduce_on_plateau, which converges noticeably better on this panel (the same recipe as in the inference methods comparison example).

We set progress_bar=False, and not only because the scanned update loop compiles to a single lax.scan that runs all \(60{,}000\) steps on the full \(50{,}000\)-series panel in about five and a half minutes on the GPU (the timing below). The step-by-step execution path behind the progress bar compiles to slightly different floating-point arithmetic, and on the \(1{,}000\)-series variant of this panel that tiny perturbation is enough to steer the optimizer into a distinctly worse ELBO optimum (the evaluation section returns to this sensitivity). The scanned path is both the fast and the well-behaved one here.

%%time

num_steps = 60_000

scheduler = optax.linear_onecycle_schedule(

transition_steps=num_steps,

peak_value=0.001,

pct_start=0.3,

pct_final=0.85,

div_factor=2,

final_div_factor=3,

)

optimizer = optax.chain(

optax.adam(learning_rate=scheduler),

optax.contrib.reduce_on_plateau(

factor=0.8,

patience=20,

accumulation_size=100,

),

)

rng_key, key_fit = random.split(rng_key)

svi_fit = fit_svi(

key_fit,

model,

y_train,

covariates_train,

optim=optimizer,

num_steps=num_steps,

progress_bar=False,

)CPU times: user 4min 34s, sys: 1min 8s, total: 5min 43s

Wall time: 5min 28s%%time

fig, ax = plt.subplots()

ax.plot(svi_fit.losses, color="C0", label="ELBO loss")

ax.legend(loc="upper right")

ax.set(yscale="log", xlabel="SVI step", ylabel="loss", title="SVI ELBO loss");CPU times: user 10 ms, sys: 0 ns, total: 10 ms

Wall time: 11.7 ms

Export to an ArviZ DataTree