In this notebook we describe how to use blackjax’s pathfinder implementation to do inference with a numpyro model.

I am simply putting some pieces together from the following resources (strongly recommended to read):

References:

- Blackjax docs: Use with Numpyro models

- Blackjax Sampling Book: Pathfinder

- Numpyro Issue #1485

- PyMC Experimental - Pathfinder

- Pathfinder: Parallel quasi-Newton variational inference

What and Why Pathfinder?

From the paper’s abstract:

- What?

We propose Pathfinder, a variational method for approximately sampling from differentiable log densities. Starting from a random initialization, Pathfinder locates normal approximations to the target density along a quasi-Newton optimization path, with local covariance estimated using the inverse Hessian estimates produced by the optimizer. Pathfinder returns draws from the approximation with the lowest estimated Kullback-Leibler (KL) divergence to the true posterior.

- Why?

Compared to ADVI and short dynamic HMC runs, Pathfinder requires one to two orders of magnitude fewer log density and gradient evaluations, with greater reductions for more challenging posteriors.

Prepare Notebook

import arviz as az

import blackjax

import jax

import matplotlib.pyplot as plt

import numpy as np

import numpyro

import numpyro.distributions as dist

from jax import random

from numpyro.infer import SVI, Trace_ELBO

from numpyro.infer.autoguide import AutoMultivariateNormal

from numpyro.infer.util import initialize_model, Predictive

az.style.use("arviz-darkgrid")

plt.rcParams["figure.figsize"] = [12, 7]

plt.rcParams["figure.dpi"] = 100

plt.rcParams["figure.facecolor"] = "white"

numpyro.set_host_device_count(n=4)

rng_key = random.PRNGKey(seed=42)

%load_ext autoreload

%autoreload 2

%config InlineBackend.figure_format = "retina"Generate Data

We generate some data from a simple linear regression model.

def generate_data(rng_key, a, b, sigma, n):

x = random.normal(rng_key, (n,))

rng_key, rng_subkey = random.split(rng_key)

epsilon = sigma * random.normal(rng_subkey, (n,))

y = a + b * x + epsilon

return x, y

# true parameters

a = 1.0

b = 2.0

sigma = 0.5

n = 100

# generate data

rng_key, rng_subkey = random.split(rng_key)

x, y = generate_data(rng_key, a, b, sigma, n)

# plot data

fig, ax = plt.subplots(figsize=(8, 7))

ax.plot(x, y, "o", c="C0", label="data")

ax.axline((0, a), slope=b, color="C1", label="true mean")

ax.legend(loc="upper left")

ax.set(xlabel="x", ylabel="y", title="Raw Data")

Model Specification

We define a simple linear regression model in numpyro.

def model(x, y=None):

a = numpyro.sample("a", dist.Normal(0.0, 2.0))

b = numpyro.sample("b", dist.HalfNormal(2.0))

sigma = numpyro.sample("sigma", dist.Exponential(1.0))

mean = numpyro.deterministic("mu", a + b * x)

with numpyro.plate("data", len(x)):

numpyro.sample("likelihood", dist.Normal(mean, sigma), obs=y)

numpyro.render_model(

model=model,

model_args=(x, y),

render_distributions=True,

render_params=True,

)

Pathfinder Sampler

The key function is initialize_model from numpyro. This allow us to compute the log-density, which is required by blackjax’s pathfinder implementation. In addition, we get a way to transform the unconstrained space (where the optimization happens) to the constrained space.

rng_key, rng_subkey = random.split(rng_key)

param_info, potential_fn, postprocess_fn, *_ = initialize_model(

rng_subkey,

model,

model_args=(x, y),

dynamic_args=True, # <- this is important!

)

# get log-density from the potential function

def logdensity_fn(position):

func = potential_fn(x, y)

return -func(position)

# get initial position

initial_position = param_info.zWe can now use blackjax.vi.pathfinder.approximate to run the variational inference algorithm.

# run pathfinder

rng_key, rng_subkey = random.split(rng_key)

pathfinder_state, _ = blackjax.vi.pathfinder.approximate(

rng_key=rng_subkey,

logdensity_fn=logdensity_fn,

initial_position=initial_position,

num_samples=10_000,

ftol=1e-4,

)

# sample from the posterior

rng_key, rng_subkey = random.split(rng_key)

posterior_samples, _ = blackjax.vi.pathfinder.sample(

rng_key=rng_subkey,

state=pathfinder_state,

num_samples=5_000,

)

# convert to arviz

idata_pathfinder = az.from_dict(

posterior={

k: np.expand_dims(a=np.asarray(v), axis=0) for k, v in posterior_samples.items()

},

)Visualize Results

az.summary(data=idata_pathfinder, round_to=3)| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| a | 1.043 | 0.051 | 0.951 | 1.139 | 0.001 | 0.001 | 5047.694 | 4780.373 | NaN |

| b | 0.730 | 0.028 | 0.679 | 0.785 | 0.000 | 0.000 | 4998.218 | 4873.062 | NaN |

| sigma | -0.657 | 0.069 | -0.785 | -0.527 | 0.001 | 0.001 | 5056.785 | 5101.670 | NaN |

axes = az.plot_trace(

data=idata_pathfinder,

compact=True,

backend_kwargs={"layout": "constrained"},

)

plt.gcf().suptitle(

t="Pathfinder Trace - Transformed Space", fontsize=18, fontweight="bold"

)

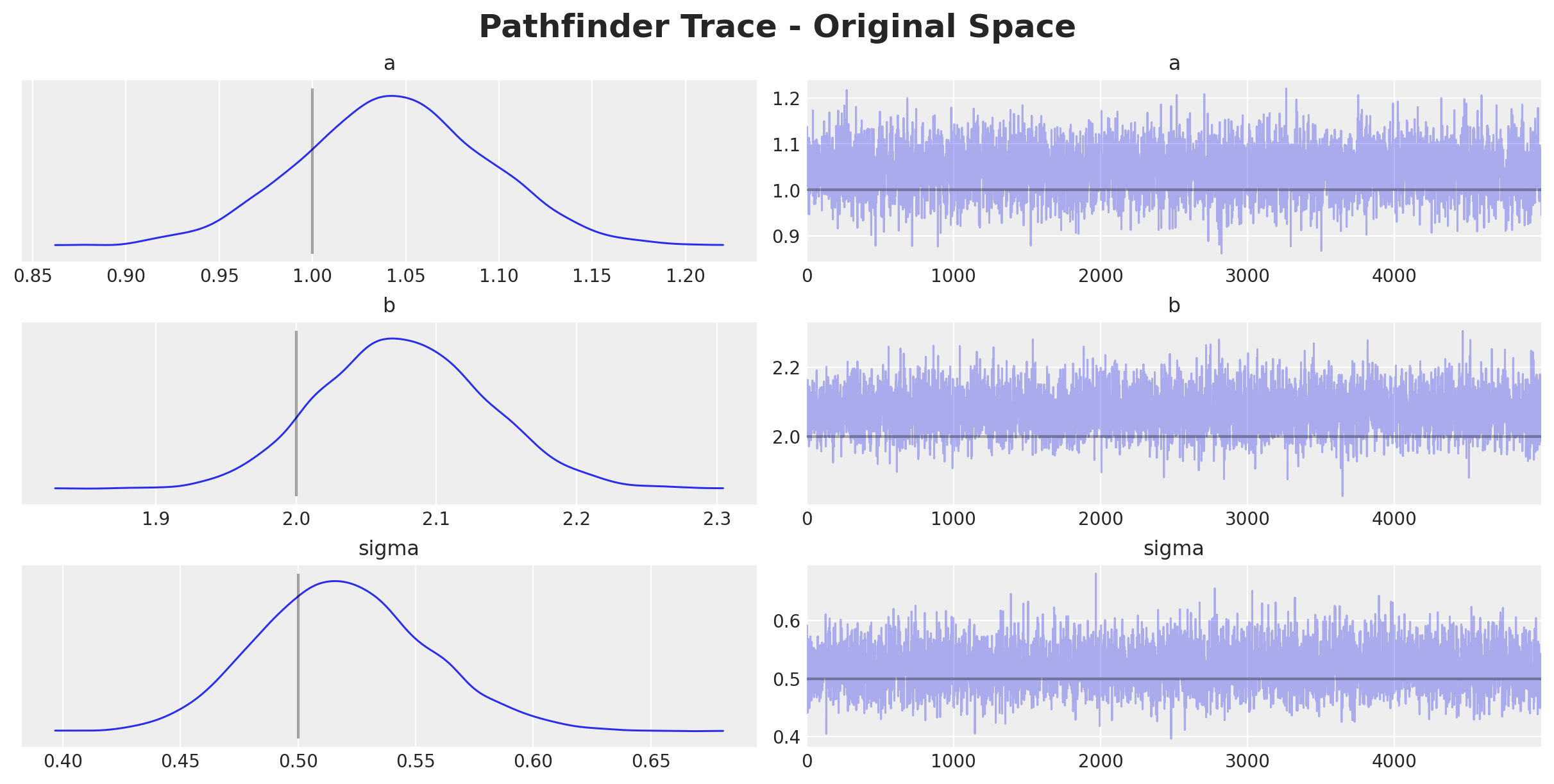

Note that the value for a is close to the true value of \(1.0\). However, the values for b and sigma are do not match the true values of \(2.0\) and \(0.5\) respectively. The reason is that we use a dist.HalfNormal and dist.Exponential prior these parameters respectively so the samples are taken from the unconstrained space.

Transform Samples

We can use the postprocess_fn function returned by initialize_model to transform the samples from the unconstrained space to the constrained space:

posterior_samples_transformed = jax.vmap(postprocess_fn(x, y))(posterior_samples)

rng_key, rng_subkey = random.split(rng_key)

posterior_predictive_samples_transformed = Predictive(

model=model, posterior_samples=posterior_samples_transformed

)(rng_subkey, x)

idata_pathfinder_transformed = az.from_dict(

posterior={

k: np.expand_dims(a=np.asarray(v), axis=0)

for k, v in posterior_samples_transformed.items()

},

posterior_predictive={

k: np.expand_dims(a=np.asarray(v), axis=0)

for k, v in posterior_predictive_samples_transformed.items()

},

)

axes = az.plot_trace(

data=idata_pathfinder_transformed,

var_names=["~mu"],

compact=True,

lines=[

("a", {}, a),

("b", {}, b),

("sigma", {}, sigma),

],

backend_kwargs={"layout": "constrained"},

)

plt.gcf().suptitle(

t="Pathfinder Trace - Original Space", fontsize=18, fontweight="bold"

)

fig, ax = plt.subplots(figsize=(8, 7))

ax.plot(x, y, "o", c="C0", label="data")

ax.axline((0, a), slope=b, color="C1", label="true mean")

az.plot_hdi(

x=x,

y=idata_pathfinder_transformed["posterior_predictive"]["mu"],

color="C2",

fill_kwargs={"alpha": 0.5, "label": "mu posterior ($94\%$ HDI)"},

ax=ax,

)

az.plot_hdi(

x=x,

y=idata_pathfinder_transformed["posterior_predictive"]["likelihood"],

color="C2",

fill_kwargs={"alpha": 0.3, "label": "posterior predictive ($94\%$ HDI)"},

ax=ax,

)

ax.legend(loc="upper left")

ax.set(xlabel="x", ylabel="y", title="Pathfinder Posterior Predictive")

Appendix: SVI

Here we compare against the stochastic variational inference (SVI) algorithm implemented in numpyro.

guide = AutoMultivariateNormal(model=model)

optimizer = numpyro.optim.Adam(step_size=0.01)

svi = SVI(model, guide, optimizer, loss=Trace_ELBO())

rng_key, rng_subkey = random.split(key=rng_key)

n_samples = 1_000

svi_result = svi.run(rng_subkey, n_samples, x, y)

fig, ax = plt.subplots(figsize=(9, 6))

ax.plot(svi_result.losses)

ax.set_title("ELBO loss", fontsize=18, fontweight="bold")

params = svi_result.params

# get posterior samples (parameters)

predictive = Predictive(model=guide, params=params, num_samples=4_000)

rng_key, rng_subkey = random.split(key=rng_key)

posterior_samples = predictive(rng_subkey, x, y)

# get posterior predictive (deterministics and likelihood)

predictive = Predictive(model=model, guide=guide, params=params, num_samples=4_000)

rng_key, rng_subkey = random.split(key=rng_key)

samples = predictive(rng_subkey, x, y)idata_svi = az.from_dict(

posterior={

k: np.expand_dims(a=np.asarray(v), axis=0) for k, v in posterior_samples.items()

},

)az.summary(data=idata_svi, var_names=["a", "b", "sigma"], round_to=3)| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| a | 1.034 | 0.052 | 0.935 | 1.132 | 0.001 | 0.001 | 3158.147 | 3521.286 | NaN |

| b | 2.062 | 0.063 | 1.940 | 2.178 | 0.001 | 0.001 | 4074.610 | 3881.514 | NaN |

| sigma | 0.516 | 0.035 | 0.455 | 0.583 | 0.001 | 0.000 | 3630.886 | 3446.498 | NaN |

axes = az.plot_trace(

data=idata_svi,

var_names=["a", "b", "sigma"],

compact=True,

lines=[

("a", {}, a),

("b", {}, b),

("sigma", {}, sigma),

],

backend_kwargs={"layout": "constrained"},

)

plt.gcf().suptitle(t="SVI Trace", fontsize=18, fontweight="bold")

axes = az.plot_forest(

data=[idata_pathfinder_transformed, idata_svi],

model_names=["Pathfinder", "SVI"],

var_names=["a", "b", "sigma"],

combined=True,

figsize=(9, 6),

)